18/2/26 Prices

International cash wheat markets were generally flat to -AUD$2.00/t compared to yesterday. US and Canadian wheat values out of the Pacific Northwest were generally the weaker, down AUD$1.50 to AUD$2.50 / tonne for mid grade milling wheat, compared to yesterdays conversion. White wheat out of the PNW was down about half a dollar, the fall having more to do with currency than grain. White wheat out of the PNW has been flat for a week or more now.

Nearby Chicago soft red winter wheat futures fell hard. Volume on the March contract was 99,376 contracts, 13.5mt, so pretty high given the closeness to the end of February. Open interest is 83,448, so possibly more volatility tonight as those not wanting to carry an open position into first notice day liquidate.

The May contract at Chicago was less volatile, still softer, but only by -6c/bu (-AUD$5.70/t).

The USA continues to compete very well into the Asian markets with HRWW. Now some US$14 cheaper than Aussie H2 wheat and US$2.00 under the Argie product. The Argie product is competing into all the major consumer markets at present, and setting the pace against US HRWW, for many buyers.

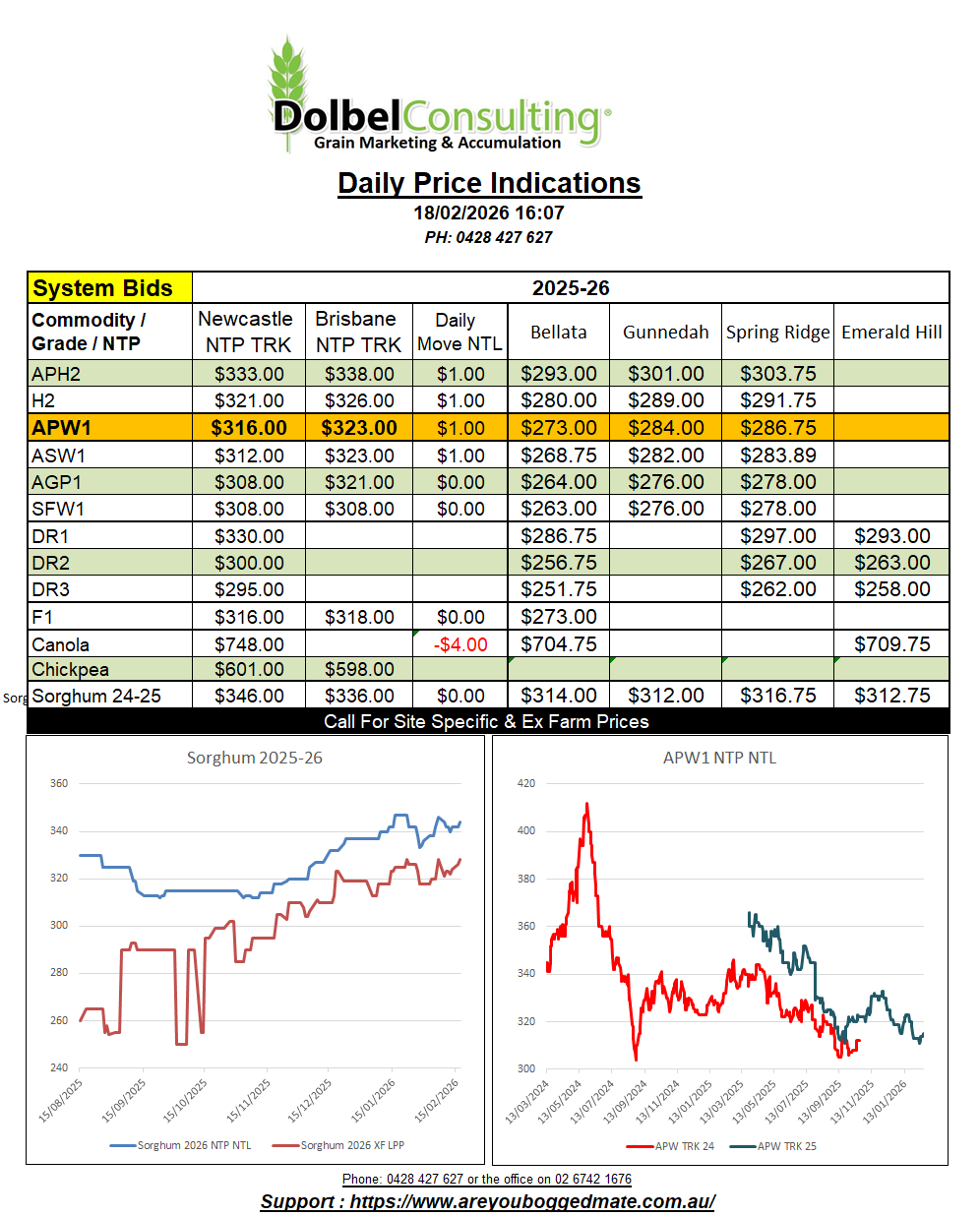

The rain in Argentina was viewed as generally favourable for their sorghum crop. FOB US and Argentine sorghum values were a little softer. This weighed on C&F China vales, which also softened a little overnight.

Comparing US, Argentine and Aussie sorghum values at a C&F China level, including tariffs for both the US and Argie products, shows we are level pegging with US values now, and still a few USD under the Argie product.

One might assume with both Argentina and Australia about to start sorghum harvest in earnest that values may come under pressure in the short to mid term. US weekly sorghum sales were still strong for the week ending Feb 5th at 261.3kt, down 24% from the previous week. China buying 139kt, demand is good.