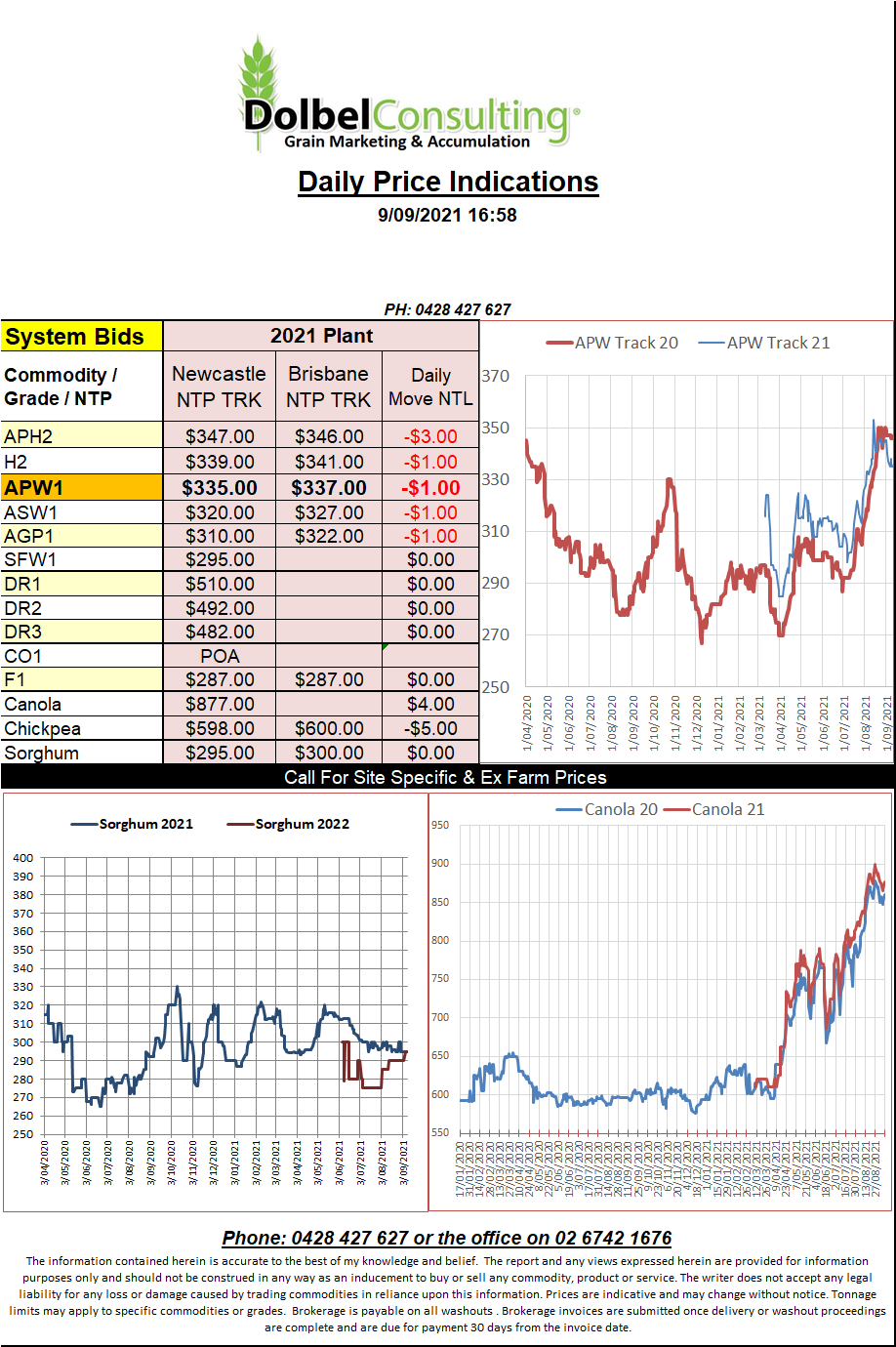

09/09/21 Prices

The US futures market continue to “square up” somewhat as we move towards the September USDA WASDE report due out on Friday, US time. The report is not expected to have too many surprises. The Canadian wheat stocks report did scare the market though, much higher than the punters had anticipated. Pegged at 6.1mt vs trade guestimates of 4.8mt. An early harvest does lengthen the marketing year.

US futures also found technical pressure from the speculative market. Commodity longs in both the US and Paris markets continue to be eroded this week.

Egypt picked up 300kt of Black Sea wheat overnight. Ukraine picked up the lions share placing 240kt against the order while Russia scored 60kt of the parcel. Prices were somewhat higher than their previous tender on Aug 30th. The lowest priced wheat was US$310.25 + freight at US$32.90, US$343.15 C&F. Freight rates varied a little but across the board are sharply higher than this time last year.

For the sake of the exercise this value would equate to milling wheat ex farm LPP of something close to AUD$310 ex farm. Currently the Asian market is offering much better value to Australian product. It does indicate a feasible floor to the market though.

Nearby Paris rapeseed futures continued to climb, up E4.75 for a November slot to close at E581.50. Winnipeg futures also closed higher but suffered some headwind from a generally weaker US market, Chicago soybeans just managing to close in the black.

Cash price analysis platform PDQ noted declines in Canadian spring wheat and durum, durum falling C$16.12 per tonne for December lift.