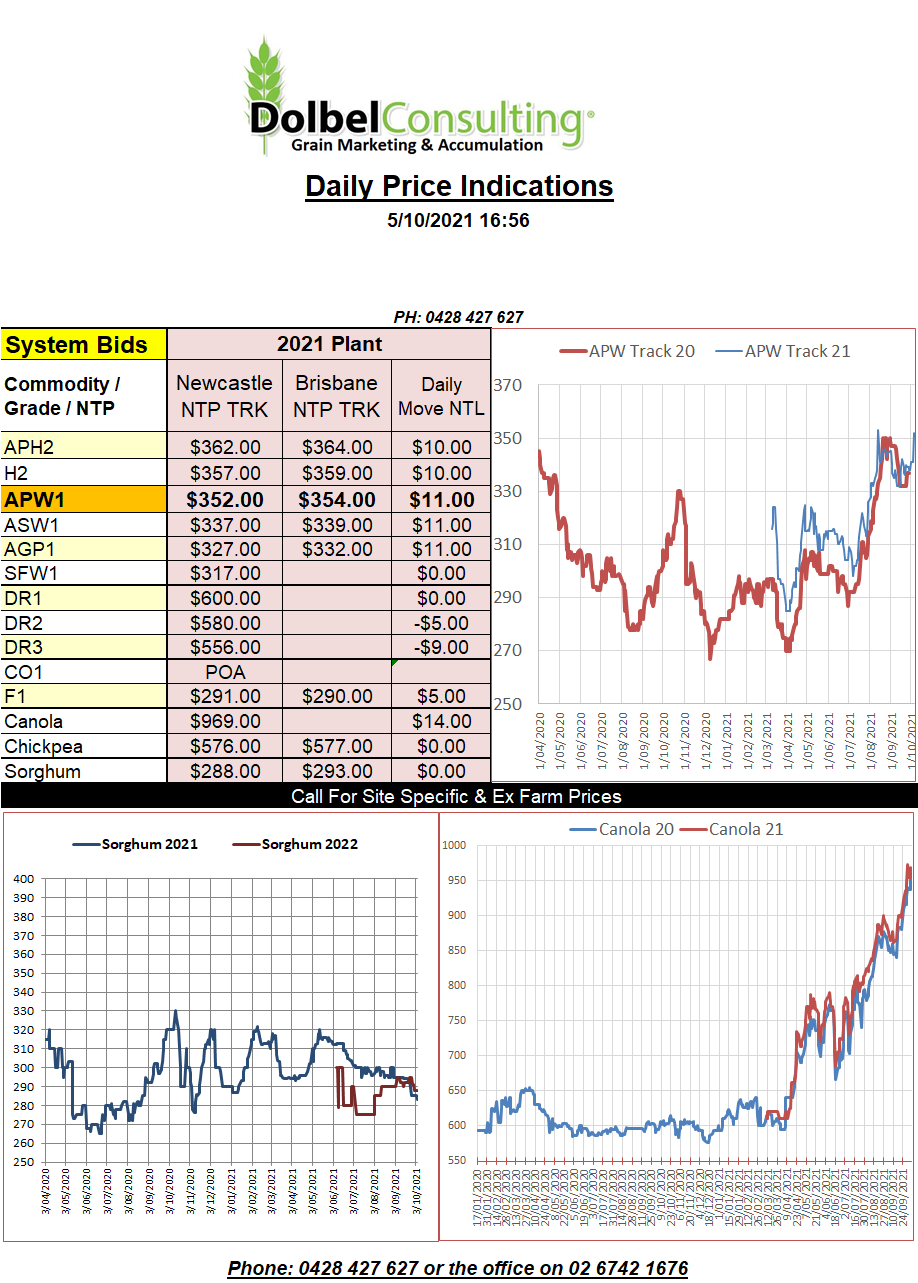

5/10/21

The lowest US wheat stocks in more than 13 years continues to be the major supporting factor to US futures at present. Wheat at Chicago and Minneapolis managed healthy gains overnight which should materialise as better new crop bids here on Monday / Tuesday.

We need to keep one major thing in our mind when we see reports about how low US wheat stocks are. From 2002 – 03 to 2008-09 world wheat stocks were low. In 2002-03 the Stocks to Use ratio was 27.80%. This ratio fell for much of the next few years to as low as 20.47% in 2007-08. During this time any production issues in any of the major exporters had a huge impact on not just their domestic values but also world values.

Currently we have a global wheat stocks to use ratio somewhere around 38%, this is still the 3rd highest global S:U ratio seen in the last 20 years. Yes it is worth keeping an eye on and the ratio may go lower but it is not sitting on a powder keg from an international perspective.

It was good to see both ICE canola futures and Paris rapeseed break away from the Chicago soybean market and move higher. Paris rapeseed futures put on E5.50 per tonne. Black Sea prices were also sharply higher, Ukraine rapeseed moving by an equivalent AUD amount of almost AUD$18 per tonne. I wonder if Ukraine growers are completing their ISCC documents, they may accept it a little better, you know, they were under communist rule for a fair time weren’t they.

US corn and SRWW wheat futures broke away from the bearish influence of soybeans at Chicago last night. Nearby HRWW futures were a little lower while Minneapolis spring wheat managed to close in the green.

Good to see both Paris rapeseed and ICE canola futures closed higher, also breaking away from a softer soybean market. Interesting to note the increase in outer month ICE canola futures. Nearby prices closed about C$4.00 higher while canola for Nov 2022 was actually up C$8.30 per tonne. The price difference between old and new crop is still very wide though. Dec 2021 ex farm SE Saskatchewan is priced at C$878.85 per tonne while the Sept 2022 price is C$664.07. The latter being roughly equivalent to an XF LPP value of about $750, so not exactly a poor price.

While we are looking at cash bids in Canada, durum prices were again higher. According to PDQ 1CWAD13 durum was bid at an average ex farm price out of SE Sask at C$721.93, up C$10.43 / tonne. On the back of an envelope using Italy as a consumer this would be roughly equivalent to an ex farm LPP price of somewhere around AUD$800+. As a counter price comparison, French 12% durum out of La Nouvelle was priced at about US$529 – US$539 FOB. This would roughly point to a comparable price of AUD$600+ ex farm LPP for a DR2-1 type product with less than perfect vitreous. There has been talk of parcels of better quality moving at some US$50 above these French values.

US corn 29% harvested, G/E rating unchanged at 59%. Soybeans 34% harvested G/E 58% unchanged. Winter wheat sown, 47%.