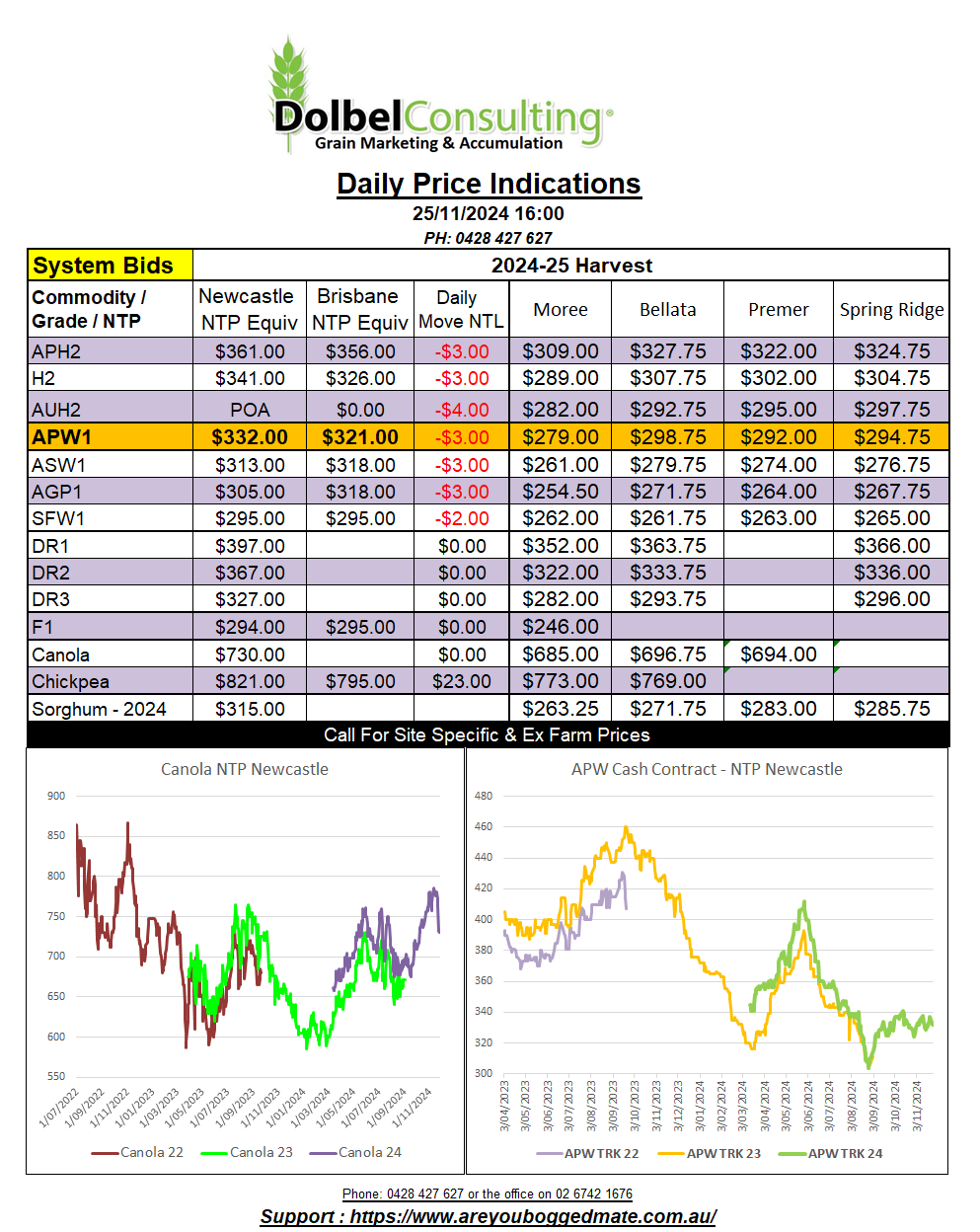

25/11/24 Prices

International Commentary

A higher close for Chicago soybean futures couldn’t put the brakes on the decline in both Winnipeg canola and Paris rapeseed futures. Paris did fare a little better than Winnipeg though. Paris slipped in the Feb / May slots but managed to close higher in the Aug / Nov / Feb 26 slots for the new crop.

The weaker AUD will help buffer the fall a little, but the trend in local prices could continue to be downwards for canola unless we see basis improvements.

The spill over weakness from palm oil futures should not be ignored. The Feb 25 slot for palm oil fell 130MYR / tonne, roughly AUD$44.80 / tonne.

Wheat futures in the US and Paris trended lower, the higher grades not slipping as much in the USA. Paris milling wheat shed €1.25 / tonne nearby. Cash values out of the Black Sea were AUD$2.00 to AUD$4.00 higher, the weaker AUD helping a lot. The softer AUD also helped turn small losses in USD/tonne out of the Pacific Northwest into slight increases in AUD/tonne compared to yesterday’s conversion. Not so for Canadian spring wheat though, even with the softer AUD the conversion shed a couple of dollars.

According to the International Grains Council world barley trade is expected to contract year on year. Smaller imports from the EU and China will counter a slight increase in imports from N.Africa and the Middle East. Currently Australian barley doesn’t compete well against Russian feed barley into the Middle East. Russia appears to have roughly a US$30 advantage to Australian feed barley there. Into the Asian market Australian feed barley is still very competitive. Russian barley into China is priced well, as it Argentine barley. Argentina, Russia and Australia are all very close in value to the Asian importer. This would in theory mean that anything that has an impact on Argentine or Russian values will in turn have an impact on Australian values. With Western Australia set to harvest around 4.52mt of barley this year the Australian market will need to continue to be very responsive to competitor pricing.

Domestic Commentary

Track wheat values were generally $2.00 lower yesterday. The trade had little interest in negotiating or buying at anything above their bid. The delivered market followed track values lower, at a public level SFW1 and ASW were both lower, but at least the feed grain guys were up for some negotiating and prices remained flat against firm offers to sell. ASW bid at $320 delivered Tamworth and SFW1 at $315 delivered prompt local consumer. I have buying interest in SFW1 for Dec / Jan at $320 delivered LPP end user.

The question of what to treat milling wheat with for weevil protection when stored on farm came up a few times yesterday. There’s a good chance that H2 being stored on farm will find its way onto a boat in Jan / Feb / March next year. The safest course of action is the keep grain destined for export, milled or unmilled, as PRF, pesticide residue free. This means that gas knockdowns can be used but nothing with a residual.

The feed grain market is generally less fussy, and as long as the spray is applied at label rates and doesn’t fall inside the withholding period, it’s generally not a problem for most feed grain consumers, but check before selling.

Canola took the biggest daily hit it has seen since August 6th this year when it fell $27.00. Canola is prone to some big moves, up and down. Back on the 9th and 10th of July it saw two consecutive moves of -$20, shedding $49 in 72 hours. Two weeks later it had rallied $30.00.