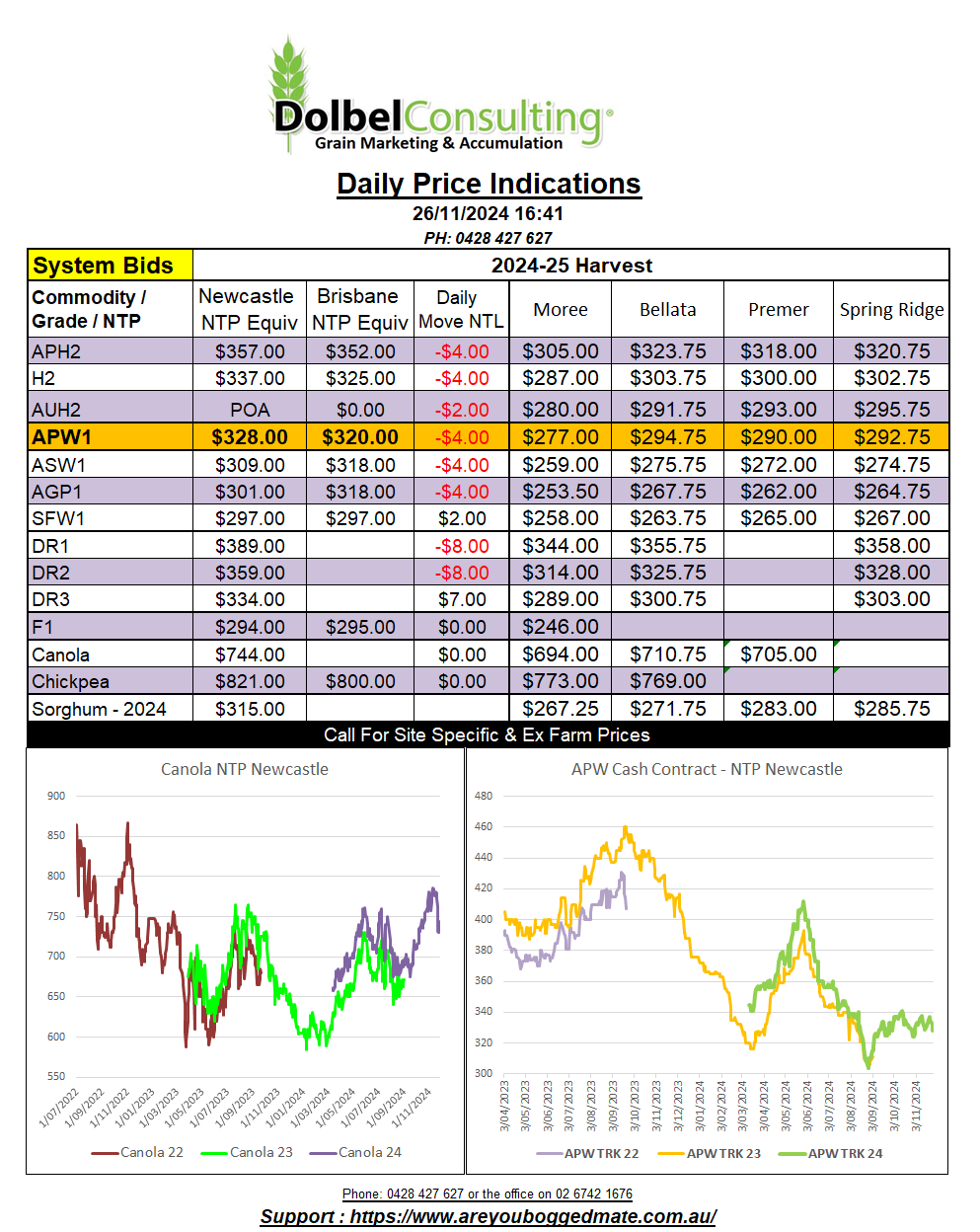

26/11/24 Prices

International Commentary

US and Paris wheat futures all closed in the red last night. Lower US futures were reflected in cash values out of the Pacific Northwest, apart from spring wheat. Minneapolis futures fell away 5c/bu, the least of the US wheat’s, but spring wheat out of the PNW increased a smidge in AUD/tonne when compared to Friday’s conversion. Paris milling wheat futures were hit hard though, back €4.75 in the December slot and €5.75 in the March slot.

Cash values out of the Black Sea were mixed, Russian offers AUD$3.00 lower while Ukraine offers were AUD$3.00 higher compared to Friday’s conversion. Local APW basis to Chicago SRWW was 2c/bu lower, not ideal, possibly reflecting the trades reluctance to take ownership in the last week of the month.

The winner from last night was oilseeds. Chicago soybeans closed in the green, just, as did Winnipeg canola futures. Paris rapeseed was the clear winner, clawing back an impressive €5.50 in the Feb slot after some big falls last week. Comparing Friday’s conversion to AUD/tonne to last night’s close, represents an increase of roughly AUD$13.94 / tonne. If reflected in local bids it should tempt many who missed selling before last weeks fall.

Private analyst SovEcon has again reduced their projection for Russian wheat exports. You might be able to bundle this into the list of reason why one would punt milling wheat on the track instead of selling today. The punters are basically expecting to see the reduction in Black Sea wheat hitting the market as an indication that demand will increase for US hard red winter wheat in Q1-2 2025. If you were of this view you would also have to think that this would encourage demand for Aussie H2 wheat.

Rainfall over the past 14 days has been exceptional across most of the US wheat belt and the Canadian Prairies. Some parts of western Oklahoma, Kansas and Texas turning from drought to flood, with over 600% of normal 14 days rainfall being recorded. In Russia, the Volga valley has seen some light showers.

Domestic Commentary

Growers refrained from marketing large volumes of track wheat yesterday. Recent price declines and harvest operations have taken producers time away from the market. Some have elected to wait for a bounce before going back to trade. This is a punt, but what isn’t in agriculture, we just need to determine if it’s a logical punt or a pig headed punt, sometimes either pay off.

At present the world wheat supply and demand is suggesting that everything is honky dory in the wheat world. Carry in stocks are good, winter sowing is winding up or complete, recent rain in both Russia and the US should help both locations recover from a dry start to sowing. Fundamentally the world wheat situation is good. Demand is steady, the market now indicating future direction is more sideways or rangebound. This isn’t pushing consumers to buy more than they need. So why would you punt track wheat.

There’s two things to consider. The bottle neck on the eastern ports due to the urgency of shipping chickpeas is one. Chickpeas need to be moved and at their destination in January, or February at the latest. Failure to meet this time slot could see boats on the water unloading as Indian harvest starts, not ideal considering the counterparties history for honouring contracts. This operational requirement is basically rolling exports of wheat out a little, the trade may be simply delaying their purchases until closer to execution. This strategy could lead to a volatile market as we move through December and January.

The second reason why one might want to punt is political. The Black Sea conflict is ramping up again. As yet this hasn’t had much of an impact on supply from the Black Sea but it potentially could. Without having an option against this scenario the only other way to participate in possible upside is with physical grain.