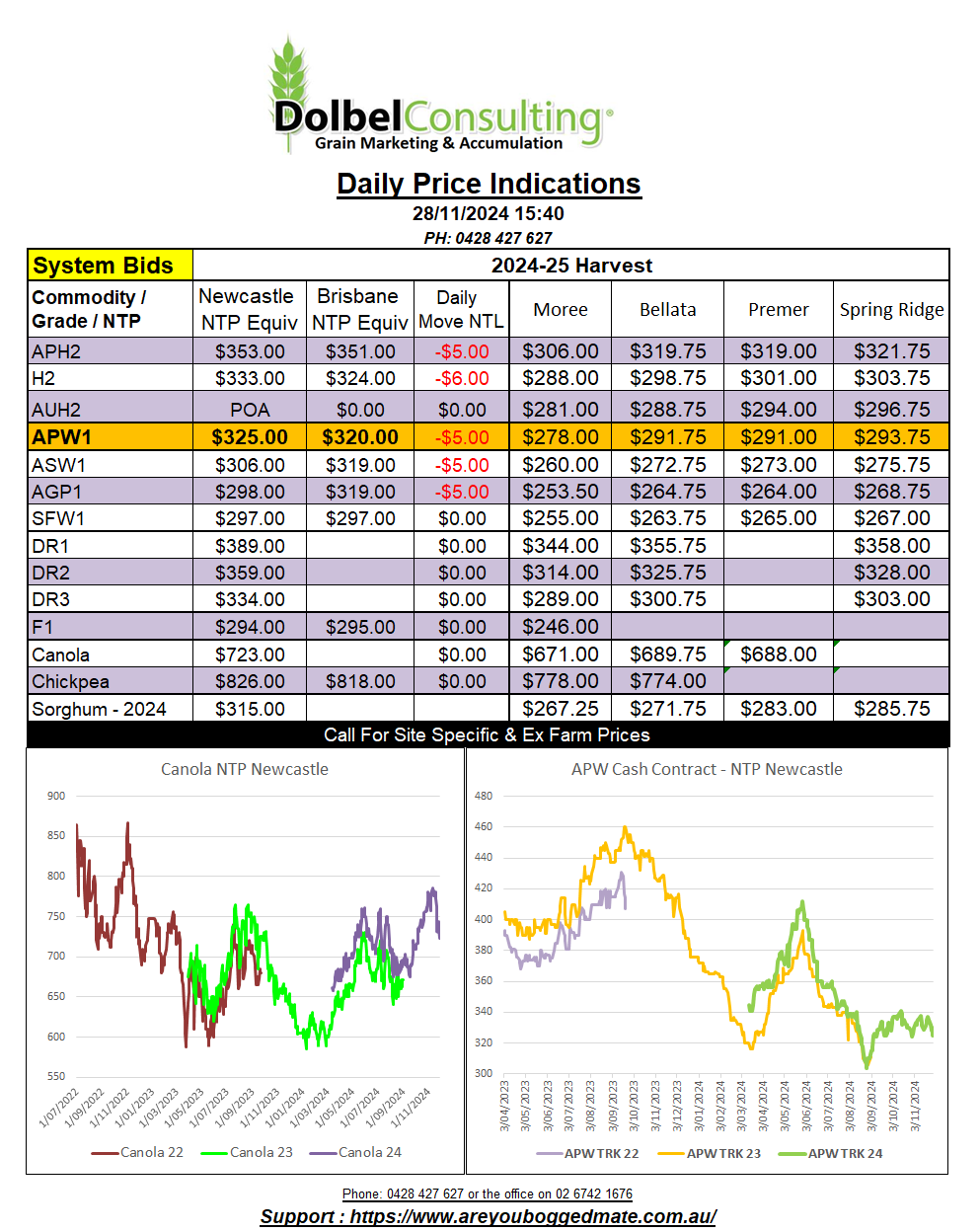

28/11/24 Prices

International Commentary

Nearby Kansas wheat futures were hit pretty hard last night, shedding 24.25c/bu (AUD$13.71/t) in the Dec slot. The December contract will move to first notice next week as it nears expiry. The move is probably more of a quick position adjustment prior to the end of November more than an indication that world HRWW values are falling apart, they aren’t. It may have the impact of stagnating that cash market for a week or so though.

Cash values for HRWW out of the US Pacific Northwest were lower. The day to day conversion comparison indicating a reduction of roughly AUD$11.21 / tonne. Not reflecting the full move in the futures market. The day to day comparison is also made worse by the improvement in the AUD against the USD. The AUD is still just under 65USc this morning.

Canola and rapeseed futures were the big losers in last nights session. Again moving against the trend in both Chicago soybeans and Malaysian palm oil, both those contract closed a smidge higher. This was not the case with Paris rapeseed, the day to day comparison shows a reduction in the conversion compared to yesterday of AUD$18.62. Winnipeg is worse, the conversion comparison there back AUD$19.12 / tonne. This will weigh heavily on local canola bids today.

Cash bids across SE Saskatchewan were lower, canola shedding C$15.39 / tonne for a Dec lift. Spring wheat was back C$4.55 / tonne (AUD$5.00) on average, Canadian wheat not reflecting the sharp move lower in HRWW but more closely reflecting the move lower in US spring wheat out of the PNW.

With the US taking a Thanksgiving holiday tonight and the majority of the punters probably making a long weekend of it, the market may lack influential news until next week. Who knows, maybe the punters will see last night’s panic in HRWW as a buying opportunity on Monday.

Tunisia durum tender numbers are in, lowest offer is US$346.70. On the back of an envelope that makes Aussie DR1 look just a smidge expensive.

Domestic Commentary

Offer volume on the track was low yesterday. Some producers continuing to cash product, taking advantage of the $1.00 to $2.00 jump in values, the majority that are holding appear happy to hold and wait out the softer sellers. The track market is seeing volume flow to the trade on a daily basis. This isn’t helping to negotiate a better price than the public bid. Sick of CropConnect, I’ll manage your transfers for a small fee.

With a sharp decline in some US wheat values overnight, I can’t see negotiations getting any easier today. For those holding stock waiting for a better price, today might be a good day to walk away from the screen and put down the phone. Not a lot of what happened in the overnight market makes a bunch of sense this morning. US wheat futures were a little overbought last week. With the December contract about to go to first notice day prior to expiry there was the risk of some “adjustments” prior to the end of November. It appears those adjustments were, or are being made. This doesn’t send a bullish signal to those holding grain, and the fundamentals in the US and Russia continue to improve for the 2025 crop. The biggest influence going forward, that’s moderately predictable remains the reduction in Russian exports. This is yet to play out and may have more of an impact on values during Dec / Jan / Feb than one would imagine.

Values into the domestic market were flat to softer. ASW to the Newcastle port was bid at $337 on a multigrade basis, APW @ $352 and H2 @ $362 for Dec / Jan / Feb delivery. DR1 direct to port was unchanged at $424 delivered Jan / Feb. Local ASW to Tangaratta was bid at $320 for a Feb slot, $310 Dec. The SFW1 market into the local feed lots was back $5.00 from last week at $310, offers from the producer steady at $320. H2 bid $310 XF Purlewaugh.