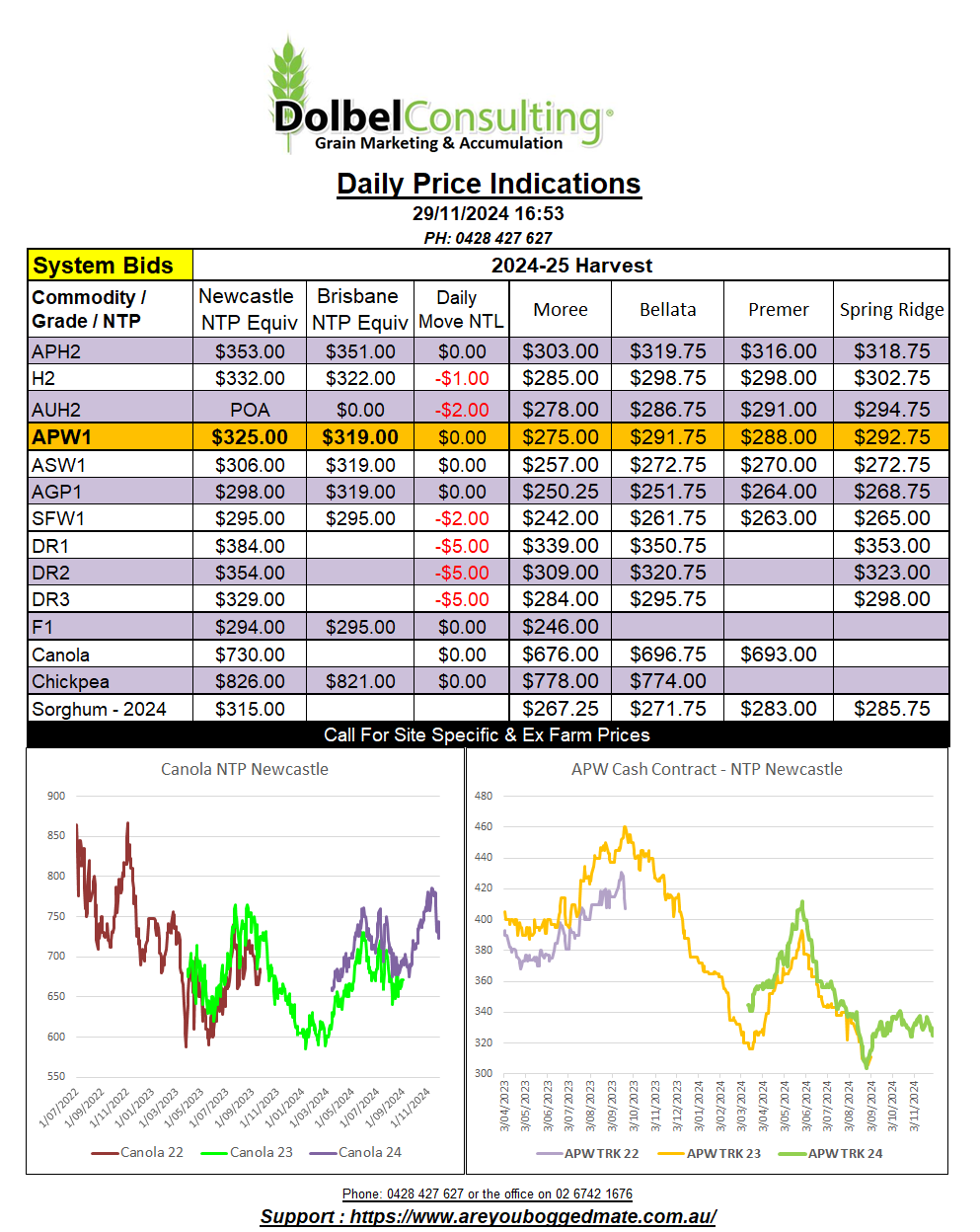

29/11/24 Prices

International Commentary

The US had a day off last night leaving the rest of the world to play without supervision. Russia didn’t pick on anyone else, Ukraine continued to play with the big kids toys. The skirmish over who runs the sandpit continued, those that own the sandpit not terribly concerned. While the rich kids continued to pretend to know how to use a futures market.

Both Paris rapeseed futures and Winnipeg canola futures closed higher. This market continues to show a large level of volatility but has trended lower for much of November. Paris rapeseed futures have fallen the least, just over AUD$20.00 compared to converted values on the 1st of November. With the EU being the export location for many sellers this is understandable. During the same time Canadian values have fallen about AUD$65.00 and Ukraine values more than AUD$80.00, much of that in one day. With no direction from Chicago soybeans last night the oilseed market moved higher, rapeseed, canola and palm oil all up by the close.

International wheat values were mixed. Paris milling wheat futures closed lower, the March 2025 slot shedding €0.50 / tonne. FOB values out of the Pacific northwest had no US offers but Canadian values for spring wheat edge higher. The average cash price ex farm SE Saskatchewan moving C$2.70 higher for a December lift. Compared to the 1st of November HRWW values out of the PNW, once converted to AUD per tonne end user and then converted back to an equivalent AUD / tonne port price using spot FX, has moved just AUD$1.00 higher. The month saw the HRWW conversion trade a range of AUD$15.21. Locally during the same time frame local H2 on the track has traded a range of AUD$15.00 per tonne.

Support for wheat going forward is sideways, movement will depend on political changes more than weather or harvest data for the next 2 or 3 months. Attached is a simple graphic that will explain what will influence the future direction of wheat prices more than anything else.

Domestic Commentary

There was a level of grower capitulation yesterday. Wheat ex farm LPP changed hands with the trade as prices generally trended lower. Track wheat volume was minimal, the fall on the track more significant than the delivered or ex farm market. Track basis to Chicago Dec SRWW futures slipped away, falling from +41c/bu to +37c/bu, or roughly AUD$2.26/t of additional downside from futures.

The delivered Newcastle market for milling grades wasn’t so bad. H2 trading at $360 delivered D/J/F or $321 ex farm C-LPP throughout the day. The trade wasn’t interested in higher offers but some APH was done later in the day, above the bid, at $376 delivered Newcastle.

Feed barley was steady at $280 delivered local feed lot. Border feed lots are bid at $320 delivered for Q1 – 2025. Prompt homes for barley and wheat for the feed market continue to be bid at about a $10 discount to the outer months, if you can find a home to take prompt.

Chickpeas moved $10.00 higher in the SQld market. The trade continue to lift the price in order to draw the last of the crop to market. The spread between the Indian price converted to AUD/t at the local packer, and the bid to buy at the local packer, indicated that the trade still have plenty of margin in this transaction. The question is how much margin does the trade require to feel comfortable in the January delivery period. There’s some enquiry about off grade chickpeas, price indication will vary greatly on the level and type of weather damage. The downgraded chickpea market often takes a week or two to sort itself out. This will also greatly depend on the volume of grain being presented for sale. Smaller volume maybe forced to find a domestic feed consumer.