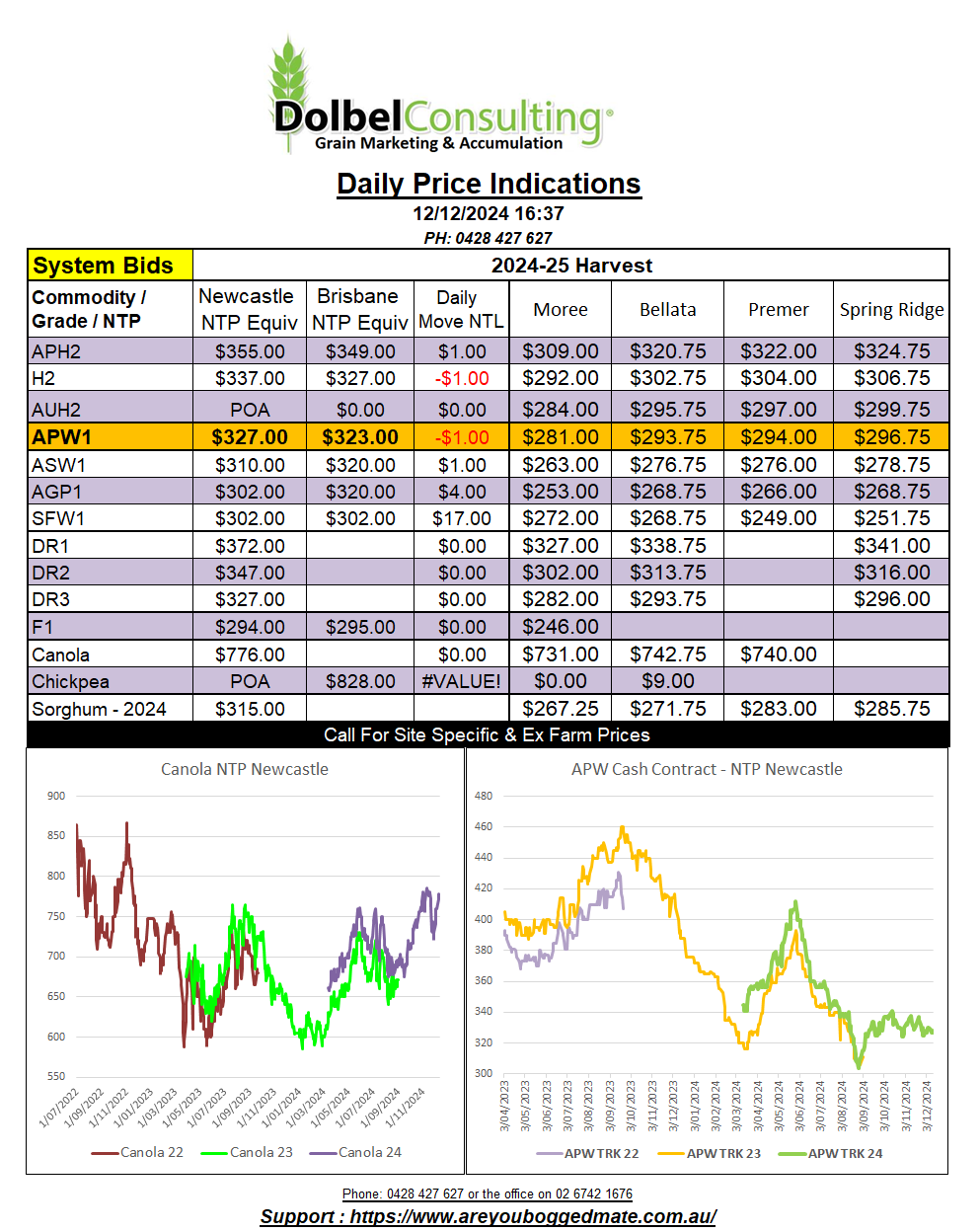

12/12/24 Prices

International Commentary

World wheat futures were generally a little firmer to flat overnight. London feed wheat gained £1.05/t in the March slot, Paris milling wheat was up €1.75 in the March slot and Chicago HRWW saw gains of just 3c/bu in the March slot. Paris rapeseed futures closed lower, back €2.00 in the Feb slot while Winnipeg canola futures found some strength from lower production estimates in the WASDE report.

International cash markets were mixed. Cash wheat out of the Pacific Northwest was higher, both Canadian and US offers creeping up by a couple of dollars. This mornings wires show Russian cash offers FOB are sharply lower for 11.5% wheat while Ukraine FOB offers appear to be as much as A$9.90 higher compared to yesterdays conversion. In AUD per tonne, French and Argentine cash wheat offers are up A$2.00 to A$4.00 compared to yesterday’s conversion.

Thailand picked up 66kt of feed wheat overnight at US$256.30 CFR. Wires report the origin to be S.American through Cargill. On the back of an envelope the number equates to a value of something close to AUD$310 ex farm LPP. This tends to back up the current market we are seeing here.

Sorghum values FOB US Gulf were higher overnight. This rolled across to slightly better values C&F China. In AUD terms US values increased roughly AUD$5.00 to AUD$6.00 per tonne when compared to yesterday’s conversion.

With US / China tariffs on the table it will be interesting to see what happens to sorghum values if this trade war picks up. As a rule the producers end up paying tariffs on grain with lower prices domestically. This could make the sorghum market very volatile in 2025 if the US tariff program kicks off early.

While on tariffs the Indian import tariff on chickpeas will return back to 66% after March 31st. With current 80 day shipping times, slow, being experienced this could make traders loading boats in January a tad nervous.

Domestic Commentary

Harvest is winding up on the Liverpool Plains. The quality of the last of the crop is poor. Wheat is generally making SFW1 grade due to falling numbers, in some cases as low as 60 seconds. Barley has been badly damaged too, F3 or worse and trading at $200 ex farm into the local feed market for those looking to harvest what is left. BAR1 bids were steady at $280 delivered LPP or $260XF.

SFW1 was bid at $330 delivered Newcastle market zone yesterday. ASW remained bid at $320 delivered Tangaratta through the trade for delivery during January > March, buyers call. The question now is do you hold stock on farm in hope of better feed prices down the line or do you sell into the closest nearby slot you can find. In the case of ASW the price hasn’t changed much since prior to harvest, selling into a flat market is better than selling into a falling market but the numbers do tend to suggest given the level of system stocks of ASW this year that this market could stay rangebound for some time. If it were to rally, it wouldn’t be unless there was an international issue during the N.Hemisphere spring in April / May.

The US futures market shows roughly 20c/bu carry between now and March. At today’s exchange rate that’s about A$11.50, we are not seeing any of this carry here. In fact we have seen nothing but eroding basis to US futures over the last couple of weeks, chart attached. This does tend to point towards prompt sales, or a futures hedge, or storing grain on the hope that basis improves without the deterioration of price, or in other words US futures fall and local prices don’t fall as far, thus improving basis. There is a lot of options for buyers this year, and until we see a significant volume of wheat consumed by feed or export the chance of improving basis, while we have sub 65c currency, is probably remote. Stem reports are failing sellers, not showing the volume of current export sales.