16/12/24 Prices

US wheat, corn and soybean futures all closed lower. London feed wheat was firmer, gaining £1.30/t, Paris milling wheat was mixed, nearby contracts a smidge higher while outer month contracts were a smidge lower. Paris corn followed the lead from Chicago, closing down €1.25 on the nearby while Paris rapeseed saw a €9.00/t gain on the nearby Feb 25 slot and lesser gains further out, May 25 +€1.75 and the new crop August 25 crop up €1.50, Nov 25 +€0.25 / tonne. Winnipeg canola joined the trend in Chicago beans, slipping C$6.10 in the nearby Jan 25 contract.

Over the last 12 hours the AUD generally traded lower after an early rally to 63.82 before closing just off the session low. Was it Paul Keating that said that the Australian dream of owning your own home was stupid, that Australians should be happy to rent. Nice call back in the 90’s, move forward to 2024 and the renters are the ones that have suffered the biggest decline in living standard. The RBA chose to keep official rates at 4.35% this week, basically thumbing their nose at retailers, mortgage holders, renters and anyone looking for a weaker AUD. I guess the living standard for many new arrivals is probably still better than it was where they arrived from. I digress, again, the AUD looks likely to be rangebound. The next RBA meeting isn’t until February 5th / 6th next year.

US wheat values out of the Pacific Northwest were a little lower overnight once the weaker AUD is taken into account. FOB values for Russian, French and Argentine wheat were up a little, less that A$2.00. While Ukraine values were less than a dollar lower. In AUD terms the day to day conversion for French durum was a little higher, in Euro we see the Port La Nouvelle value at €317.50, a Euro higher than the weekly low and just above the 12 month low set back in May this year during a sudden drop in prices.

Sorghum values FOB Gulf were back a little in USD. The weaker AUD is helping a little, but there’s still potential losses of around A$1.50 / tonne in that conversion. Weekly US export sales for sorghum were terrible, US Gulf prices are responding accordingly.

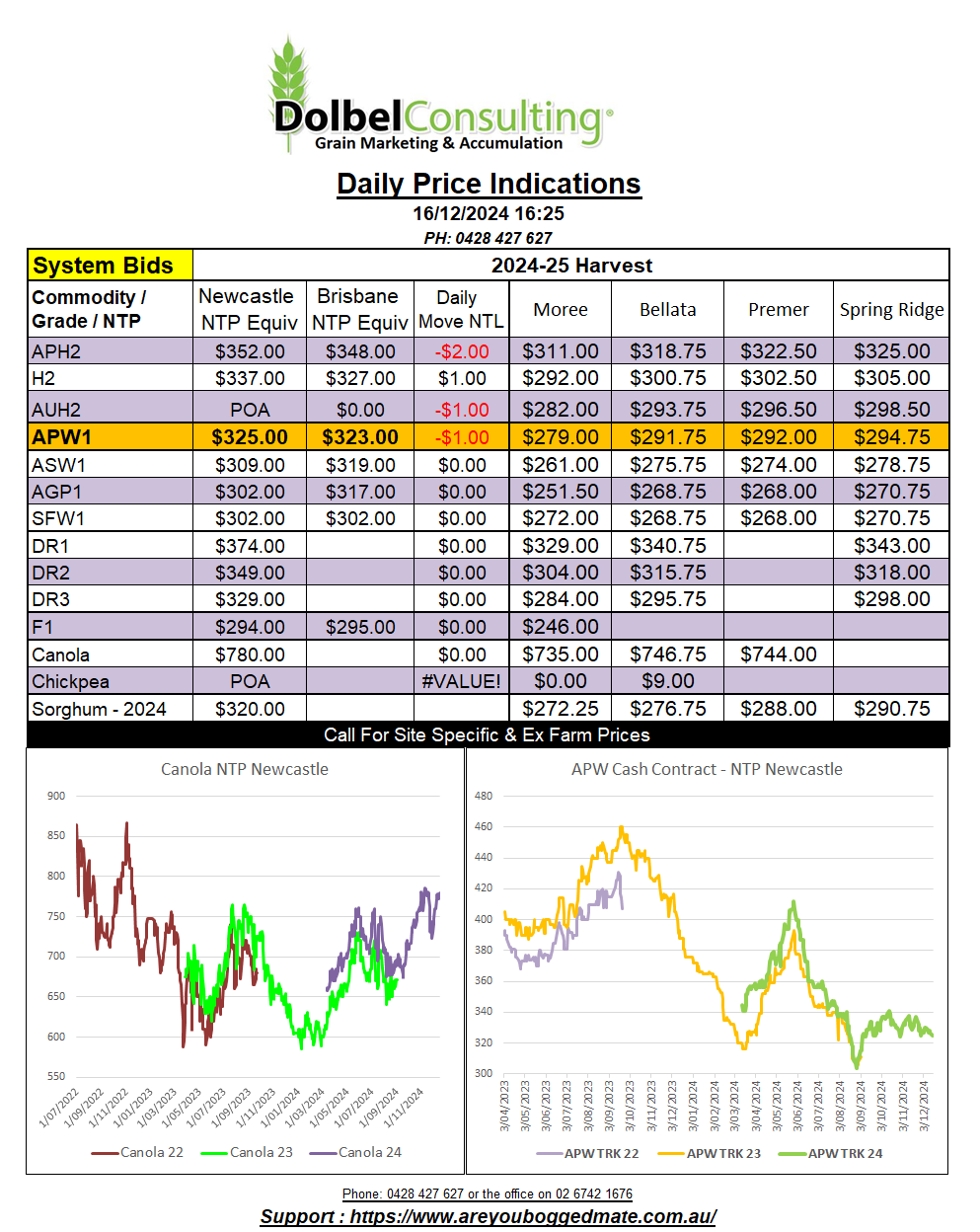

Local markets were flat to softer. Track wheat values generally not slipping more than a dollar. With the local market not falling dollar for dollar with the US market we did see a slight up tick in APW basis to Chicago SRWW futures, but +6c/bu isn’t exactly something a seller should get excited about.

From a trade hedge perspective, considering AUD/USD exposure is hedged, the current relationship between US futures and local cash prices may be presenting a good opportunity to buy local and sell US futures for the trade.

This close to the Christmas break, and with so much money tied up in chickpeas, the ability of the trade to buy volume at these levels may be somewhat tied.

The delivered feed wheat market, or should I now call it the ASW / SFW1 market, was mixed. Generally flat but some merchants did reduce bids or roll demand out another month. Business went through at $315 delivered Tangaratta for ASW in the January / February slot, buyers call. The SFW1 market was softer at Newcastle, bid $330 delivered Jan / Feb. Local bids were as low as $290 delivered, but there was a limited volume of public buyers yesterday. Most SFW1 positions are now covered out to Feb / March. If you are looking to clear silo’s prior to sorghum harvest you may need to consider selling prior to the break.

ASW on the track at Walgett was bid at $256, executed by road to Tamworth this would cost a buyer roughly $325 delivered. ASW at the Gunnedah silo was bid at $276, execution by road to Tamworth would cost the buyer roughly $321.

New crop sorghum was $5.00 lower on the bid sheets delivered Newcastle port by road, an offer to sell did see the bid to $350, $355 offers were rejected.