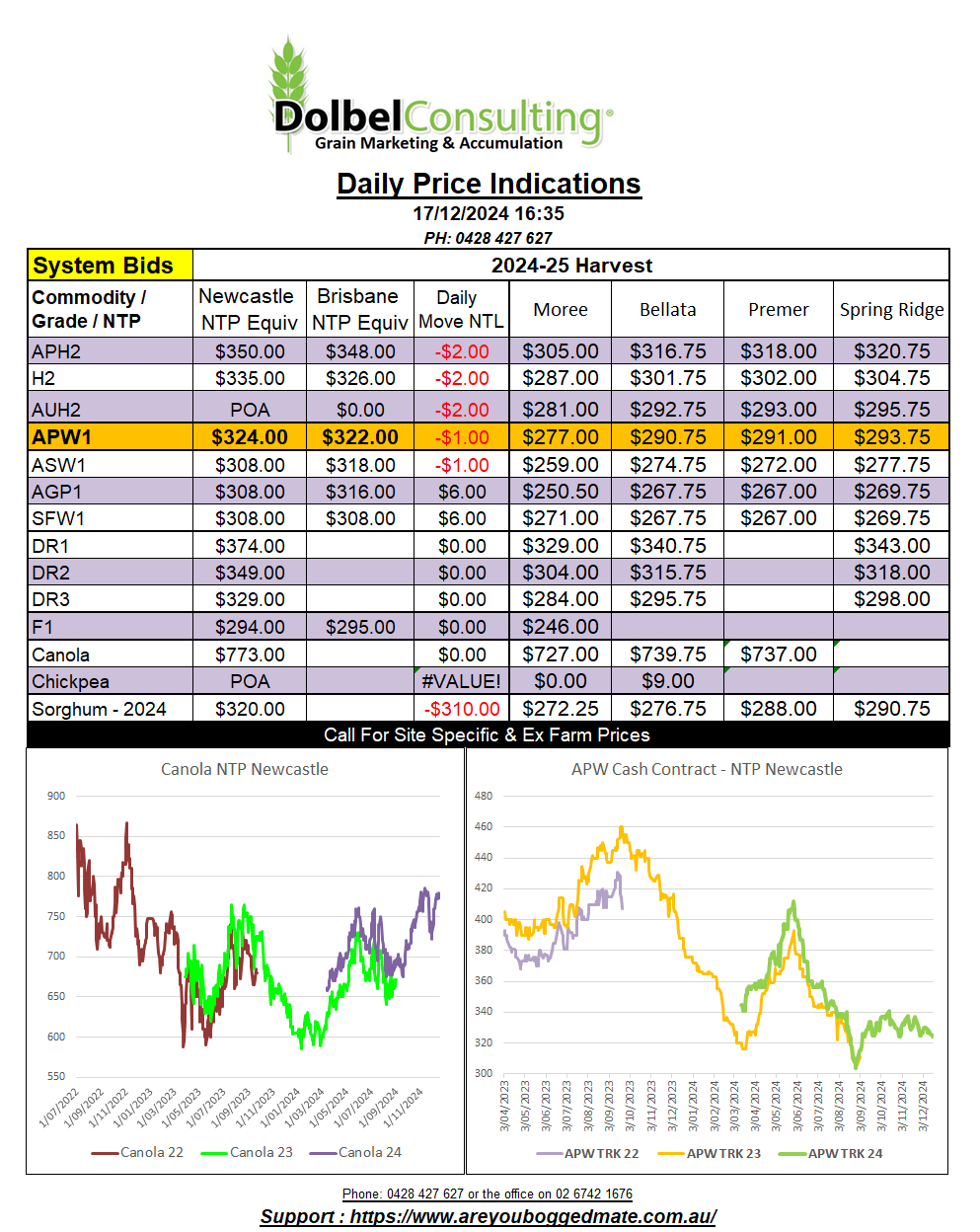

17/12/24 Prices

At least there’s some green on the screen this morning. London feed wheat futures were up £3.20/t out to the May slot, Paris milling wheat saw good gains in the March slot +€4.00/t, the May slot not far behind at +€3.50 / tonne. Both Chicago and Paris corn was higher. while Dalian corn in the May 25 slot was a smidge lower. The shining light of the last week was hit the hardest, both Paris rapeseed futures and Winnipeg canola futures shed a bunch of value nearby and in the outer months. A weaker Chicago soybean market didn’t help, neither did a weaker palm oil market which shed roughly AUD$7.40/t in the March slot.

World cash wheat values were mixed. Canadian 1CWRS 13.5 was lower ex farm SE Saskatchewan as well as out of the Pacific Northwest. US offers out of the PNW were also mixed, HRWW was up about AUD$1.25 / t compared to yesterdays conversion versus a decline of roughly AUD$1.10 / tonne for spring wheat. US white wheat values out of the PNW were unchanged day to day, the slightly firmer AUD reducing the day to day conversion by less than a dollar.

Black Sea, French and Argentine offers were generally firmer. Black Sea values flat to AUD$3.00 higher compared to yesterday while French values for 11.5% wheat were up by as much as AUD$4.90 / tonne compared to yesterday. Argie and Aussie values were up about a dollar.

Saudi Arabia picked up a massive 804kt of wheat by tender, taking many in the trade by surprise, not expecting to see this volume for this tender. The tender helped support both US and Paris milling wheat futures. The tender for 12.5% wheat was for delivery to multiple ports. The average price was just under US$269 C&F. On the back of an envelope this is close to something like AUD$320-$330 port Newcastle equivalent, a far cry from current bids of AUD$360 for H2 wheat delivered Newcastle.

The chance of east coast Aussie grain featuring in the supply program is probably remote at best. Most likely Black Sea, Russian wheat.

I mixed day yesterday, the number of different grains on my desk is testament to the diversity of the area. The day saw faba beans, chickpeas, feed barley, sorghum, wheat and canola priced. Looking at the Paris and Winnipeg canola markets this morning, those that sold yesterday should be happy.

Chickpeas found prompt buying interest at $800 delivered Narrabri packer or $818 delivered Werris Creek packer. Bids were also available on an ex farm LPP basis at $803 for prompt movement.

Feed barley was flat to softer, down a couple from some buyers while unchanged from some. The LPP consumer trade bid was public at $278 delivered Q1 buyers call. While there was some ex farm interest at $262 Spring Ridge or $258 Premer for January pickup, prices were too low for most producers.

The SFW1 bid saw the most variation, from $290 January pickup XF LPP to as low as $277 XF C-LPP for Feb / March pickup. Track wheat saw a little improvement in basis as local bids moved a dollar higher. Port by road bids were steady, H2 bid $360 delivered against the offer to sell of $365, neither counter party willing to meet the other.

Faba beans saw limited interest in feed grade, bid at $415 XF LPP. The number one grade failed to attract a firm bid, but saw indication from the packer at Narrabri of $540.

Durum by road to Newcastle port continued to slip away, buyers were limited with the best bid for a January slot coming in at $410 for DR1. There is little to no interest in off grade durum as yet. With the huge supplies of good low grade wheat this year those with bad off grade grain may struggle to sell in Q1-2 2025.