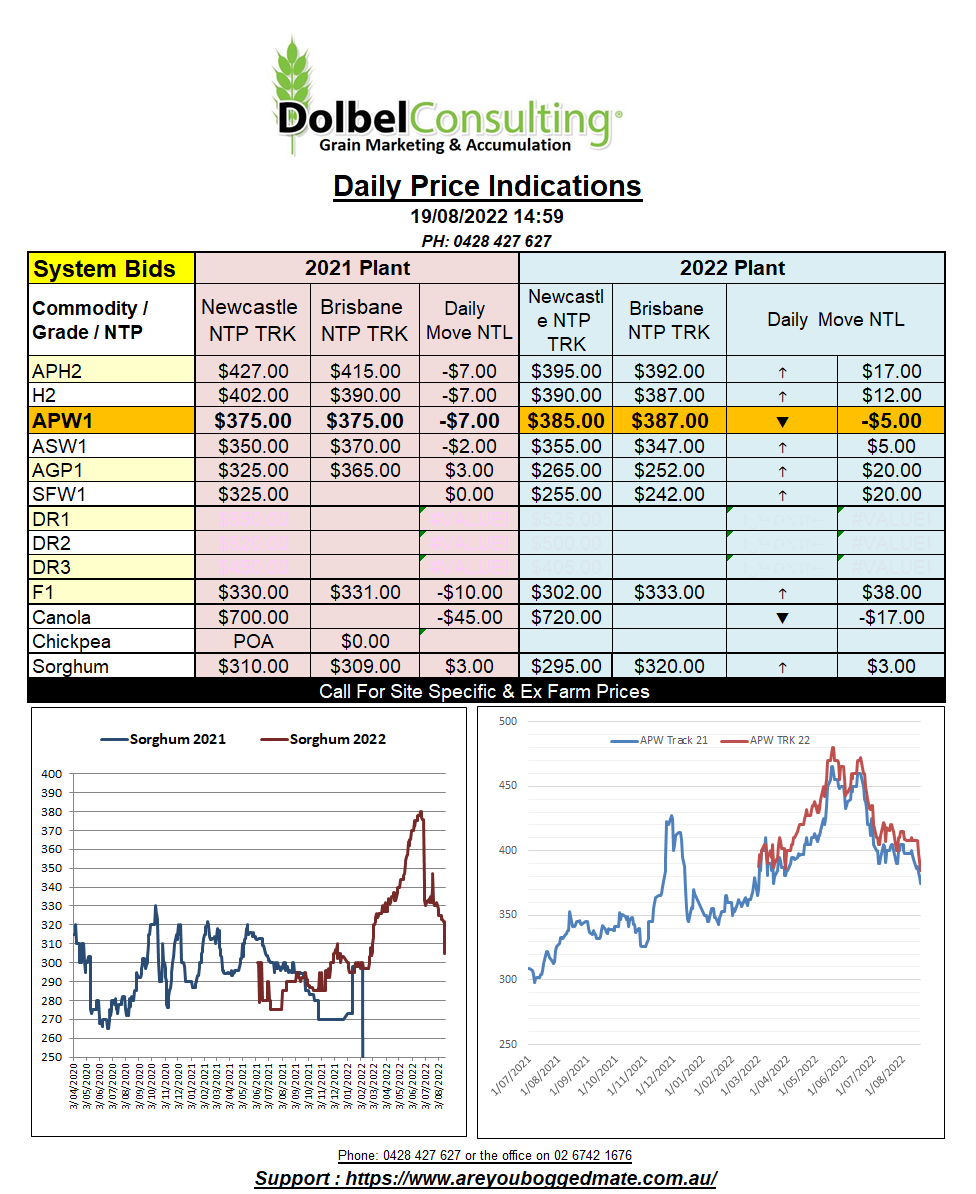

19/8/22 Prices

US wheat futures continued to fall away. The Chicago SRWW contract shedding another 31.5c/bu (AUD$16.73/t) overnight. Spring wheat and HRWW futures were also lower. Increased competition from the Black Sea and poor weekly US export sales the key. The basis traders offering new season wheat contracts here are likely to follow the US market lower […]