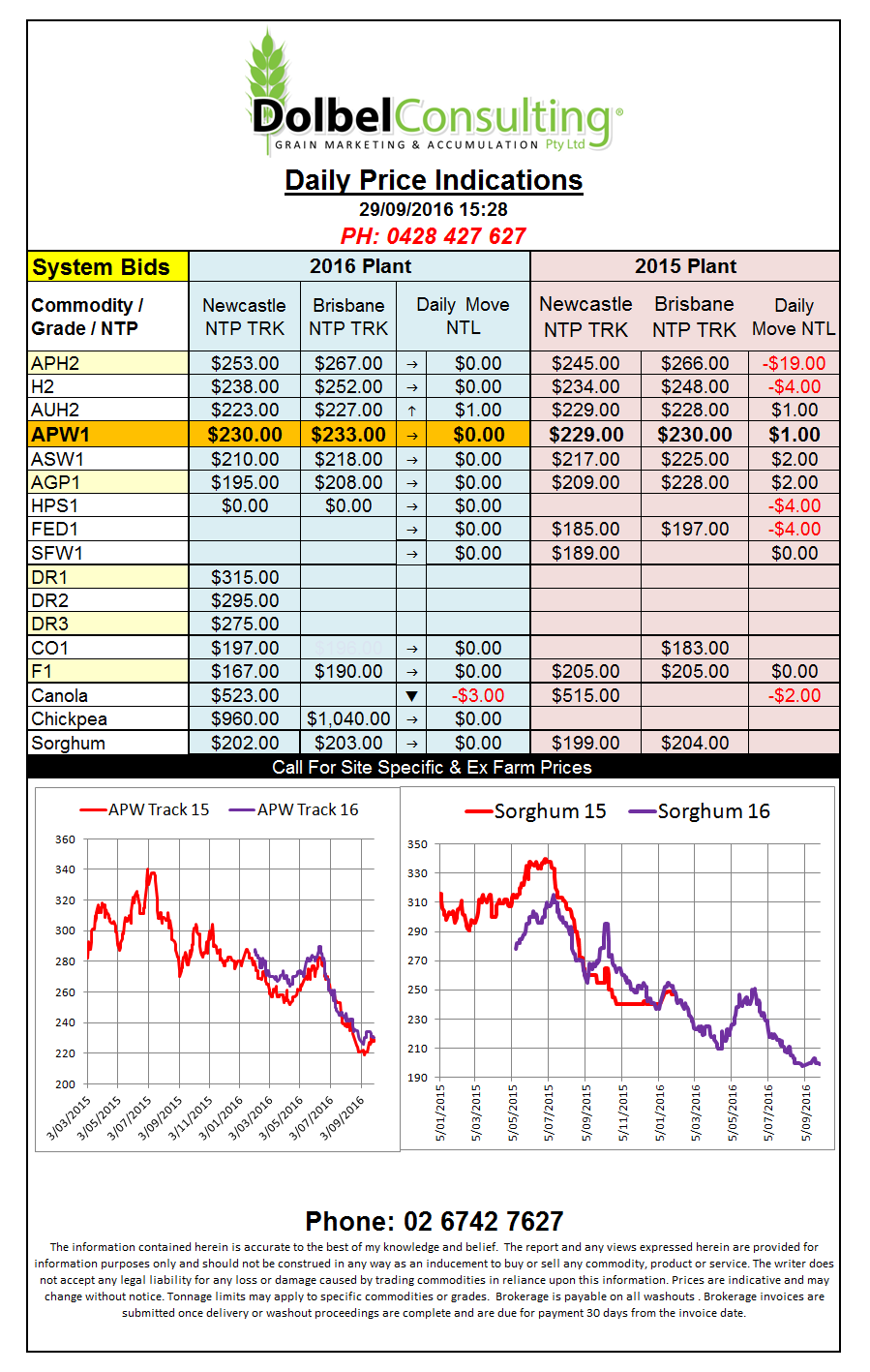

Prices 29/9/16

US corn futures closed lower in spite of the USDA reporting a 1.577mt sale to Mexico. The sale was spread over this year and next year but with over 1mt still pencilled in for the current season in any other year it would have been a serious market mover. It does bring up the question why such a big purchase though, are they bottom picking, is this an indication the low prices are in for the longer term, only time will tell.

Wheat futures in the US found support for HRW and DNS wheat while the SRW contract drifted lower in line with the row crops. There’s a lot of talk about spreads to the higher grades improving. So I ran the numbers, converted US futures to AUD per tonne, compared APH, APW and the three US grades. It appears it’s just hype at present, the spread between DNS and SRW in the states as of the 1st of September was about $60, it’s $50 today. Granted is has rallied from $42 set a couple of weeks ago but long term it has a long way to go to be termed a “premium spread”. The APH/APW spread over the same time is up $3.00, whoopee. So with this in mind you may well come to the conclusion that the higher grades should have a long way to go.

EU oilseed demand could increase greater than previously expected too. Lower sunflower yields will compound with lower canola production this year. New crop rape is emerging patchy too. Russian wheat harvest at 73.9mt with around 10% left to come.