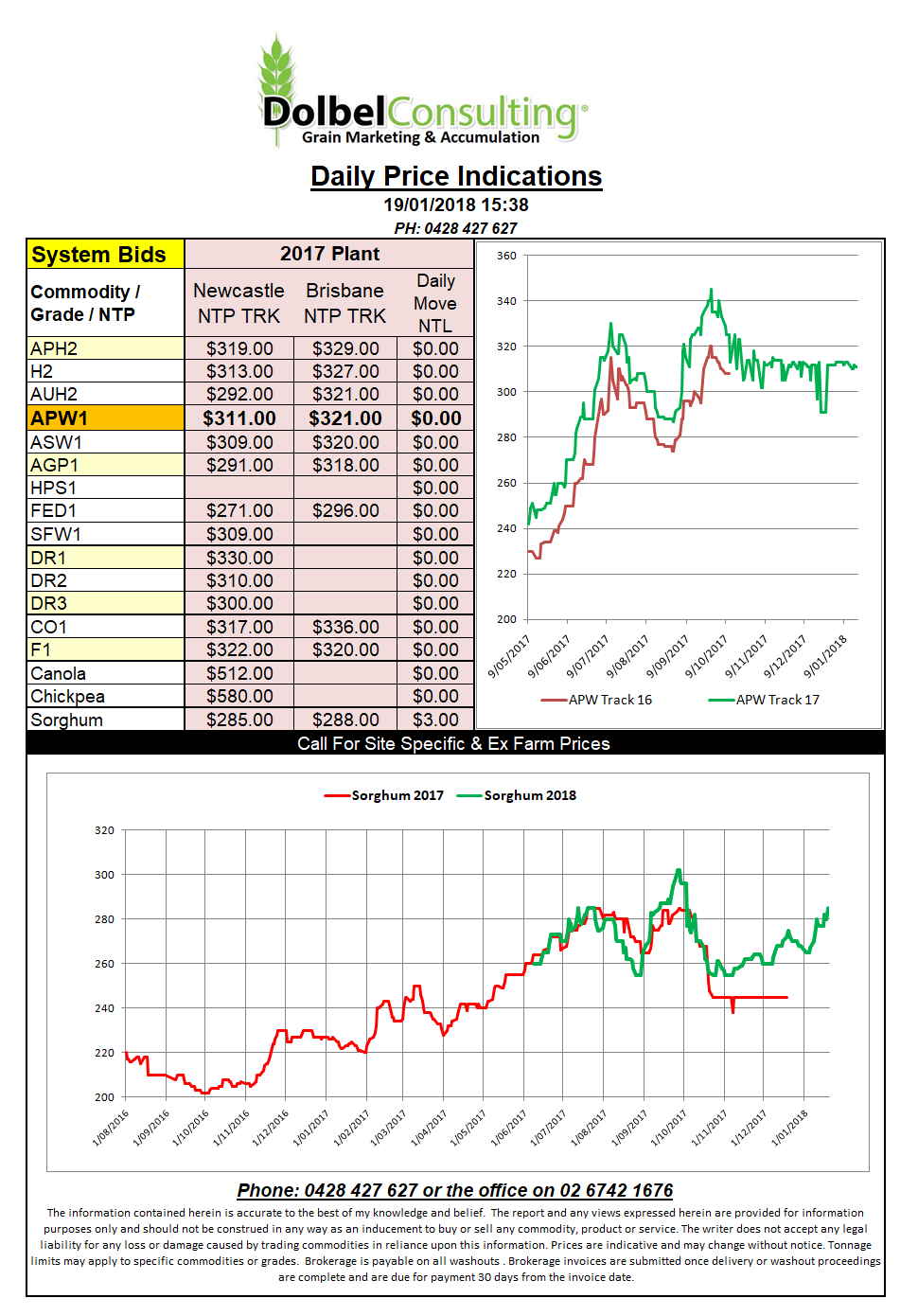

Prices 19/01/18

The trend in international markets at the moment is building wheat stocks. Last night Strategie Grains reduced EU exports for this season by 750kt, to a five year low. StratGrain is one of the lowest estimates at present at 21.6mt for EU exports, the IGC are still dreaming at 24.6mt and the European Commission must still be in the Riviera as they are up around 26mt of EU exports.

Who’s to blame, yes as always it’s the Russians, fixing elections, fixing wheat markets, those pesky Russians can break everyone’s hard work it appears. The pace of Russian wheat exports have surprised even the Russians. In December they forecast wheat exports at 35.5mt for the entire season but have already moved 20.7mt so may well smash the old record to pieces.

The other side countering much of the ever bearish news about 2017-18 wheat is the constant downgrading of production estimates for the 2018-19 wheat crop. StratGrain overnight pulled their EU estimate back 700kt to 141.6mt. Even the IGC see’s world wheat production falling in the coming season by a massive 35mt to 742mt. That’s only a little higher than the 2014-15 crop, which was a record that year. The numbers aren’t all smoke and mirrors either, we are starting to see more fundamental justification. Take the USA, the lowest winter wheat acres in over 90 years, Black Sea winter wheat area is also lower and things need to turn around across much of Australia to see anything close to a normal plant here. Could it be true, low prices actually fix low prices, I was starting to have my doubts. It was looking like low prices hurt those with expensive currency and allows others to capitalise on their inability to support their farming exports. Or am I just getting a little more bitter and twisted in this heat……..does anyone want to buy some carpet…or a mattress.