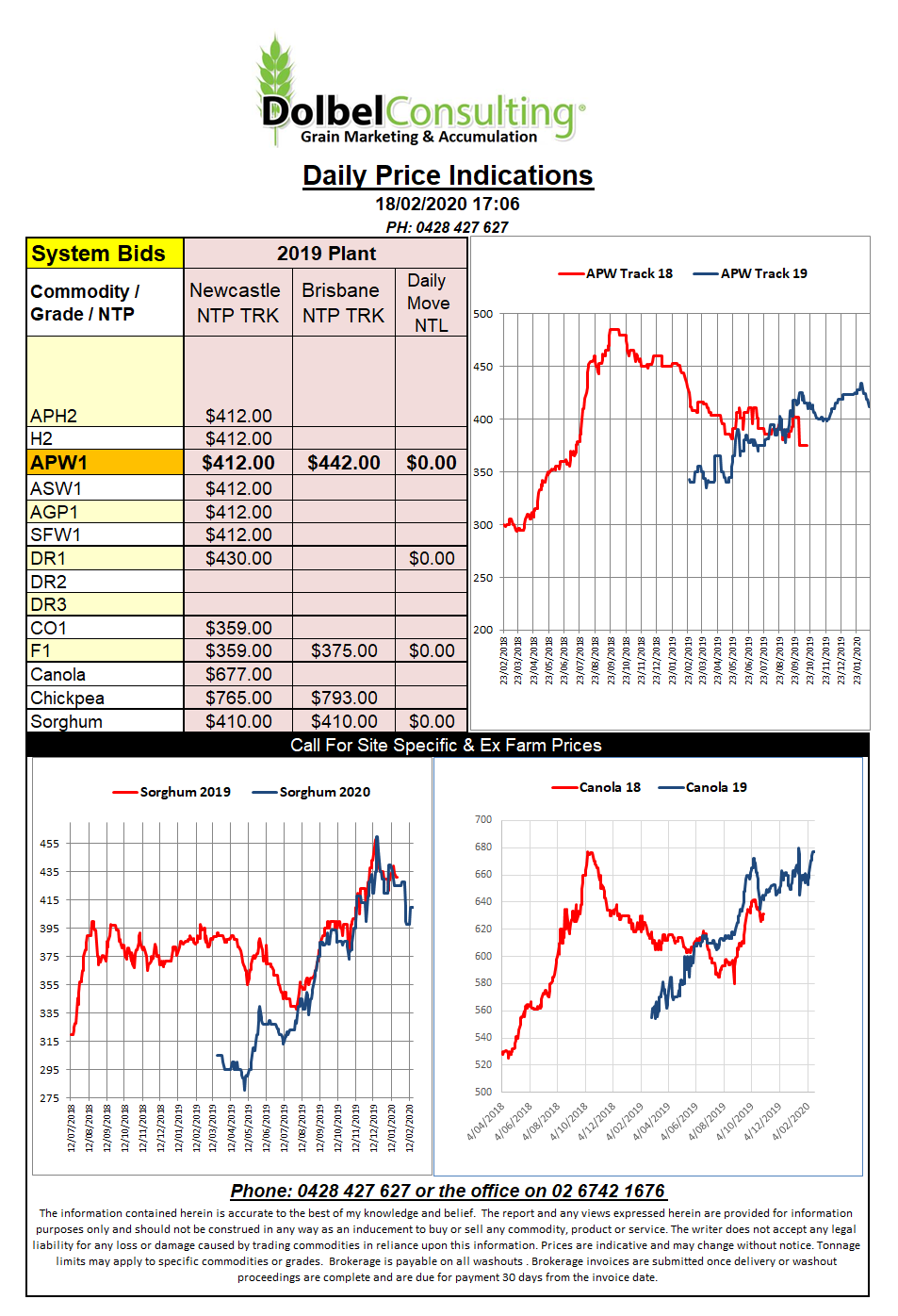

18/2/20 Prices

China continue to confirm it will meet US / China phase one trade deals arrangements regardless of the shock the coronavirus has had on importers. The lack of staff at some ports is becoming a major issue with many ships destined to China being diverted or ships leaving China failing to load. The oilseed sector is probably the hardest hit ag product at present. We have the US & S.America trying to place soybeans while the delays are also seeing issues with orders for palm oil out of Indonesia. We may see CPI increases as the cost of alternative imports from China increase in value. The Gov must love the way the GST revenue increases as import values increase. EU wheat exports remain strong at 18mt, that’s 70% better than last years reduced crop. ABARES have had another stab at the Australian production estimates for the 2019-20 winter / summer crops. NSW Sorghum is pegged at 120,000t, I think that might even be a little ambitious. In Friday afternoons report from Riverina Stock Feeds the NSW sorghum crop was estimated at just 59.5kt. I’m not being cynical but if anyone had a vested interest in talking the size of the crop up it’d have to be a consumer. The ABARES old crop wheat number is only 15.165mt, that’s over 2mt less than the previous season which itself was pretty diabolical on the east coast. The wheat number is 683kt bigger than the Riverina number which is pegged at 14.48mt, a decline of 17% on 2017-18.