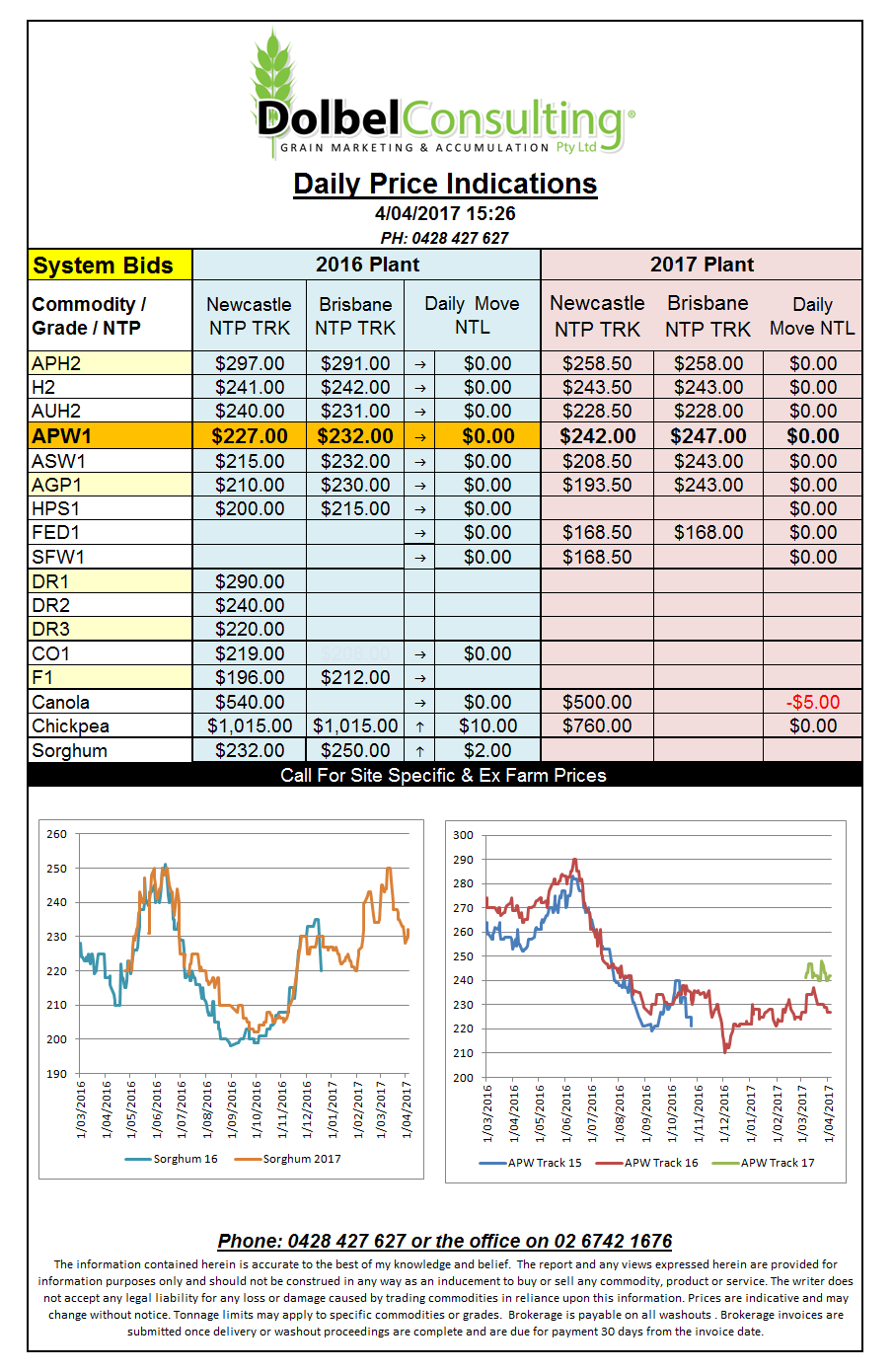

Prices 4/4/17

The US markets were still mulling over the USDA report from Friday night that showed a big jump in US soybean acres for 2017. This saw bean values continue to slip away but it appears that canola and Paris rapeseed futures have fallen enough for now with both markets managing to hold at current values, or in the case of the Paris contract actually put a couple of dollars on by the close.

The funds had spread soy / corn and are now reversing that spread adding some upside potential to the corn market on the buy back. At these values the US farmer still seeing better prospects in soybeans over corn though.

Rain across the HRW and SW belt in the USA continued to add pressure to wheat prices at Chicago and MGEX. Corn may see some more upside potential due to rain delays but USDA crop insurance guidelines suggest a planting window starting from late this week to early next week so at this stage of the game talk of planting delays driving markets are probably a little premature.

The end of March has come and gone and still no news on the Libya durum tender. 1CWAD values in SW Saskatchewan were higher by around C$3.50 / tonne yesterday and closed out around C$258 ex farm up country or roughly C$266 at the elevator, around $5 -$10 better than our own local values.

India confirmed a 10% import levy on pigeon peas last week, no news on what they might do with chickpeas as yet.