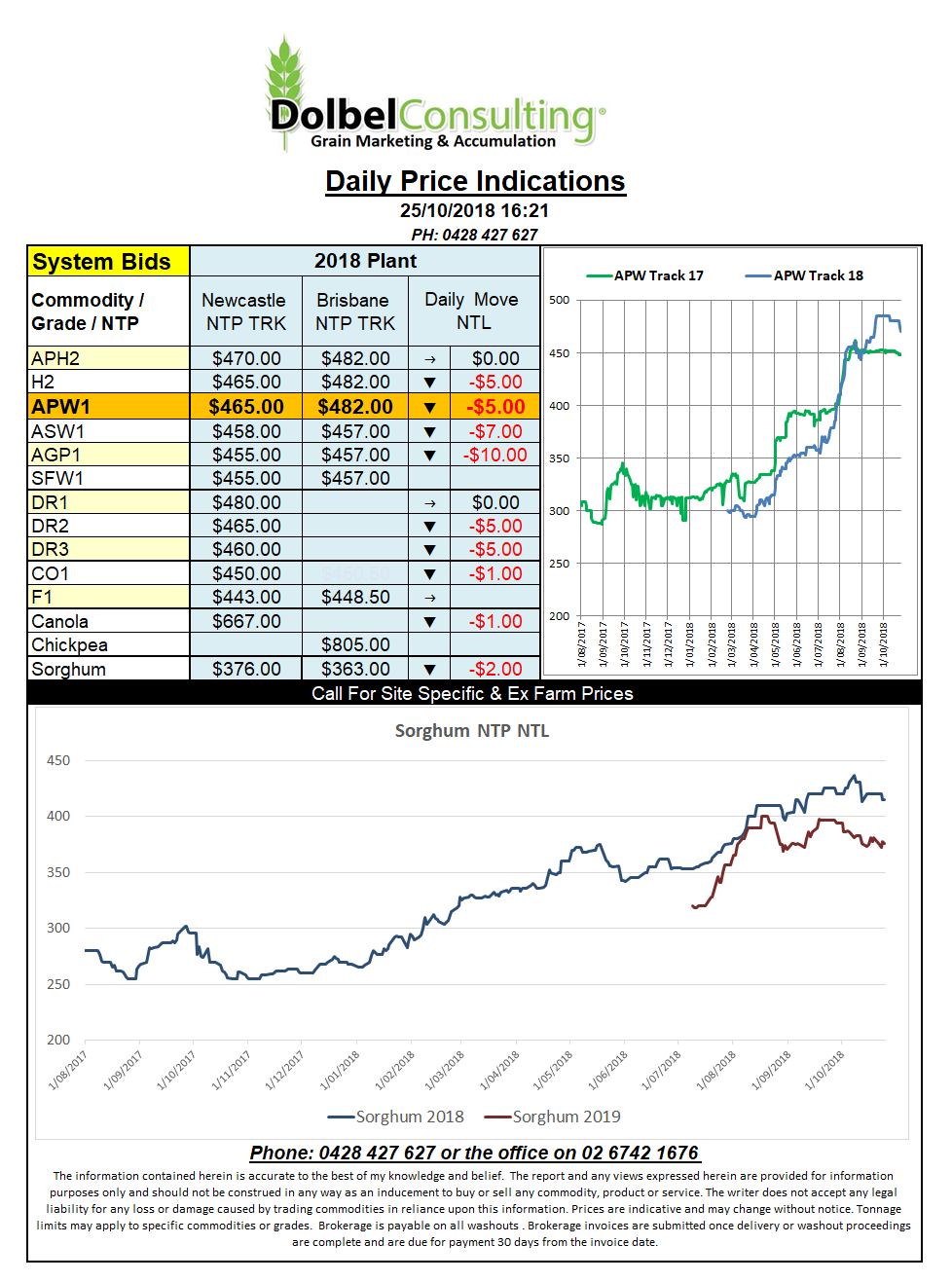

Prices 25/10/18

US wheat futures were lower again in overnight trade. A quick look at the charts and the stochastic indicates that the December CME soft wheat contract is now very much oversold. There is no law stating that it can’t remain this way for a little while but fundamentally at some stage these positions need to be reversed and we should see at least technical support begin to creep into this market in the short term.

Slow US exports are the thorn in this markets side at present. The question needs to be asked is it simply a matter of price or is there other reasons US exports are suffering. It’s not quality, so it must be a bit of column A and a bit of column B. Prices into the Asian market are roughly US$290 for Aussie wheat, usually around a $20 premium over red wheat. White wheat out of the PNW will work into Asian market for roughly US$275, so potentially it’s not price when aimed at the right market either.

The demand side is simply choosing to buy Black Sea wheat as it is closer and thus cheaper than the US product. For instance Russian milling wheat can move into N.Africa for US$235 the same wheat from the US would cost the buyer closer to US$270. Basically Russia is keeping US wheat out of the largest wheat market in the world and until we see the USA appear on import orders for N.Africa and the middle east, in volume, than US wheat exports will stumble. Don’t mention China.

Tunisia picked up 50kt of durum @ US$274.69 CFR, this is $2.00 more than their previous tender price.