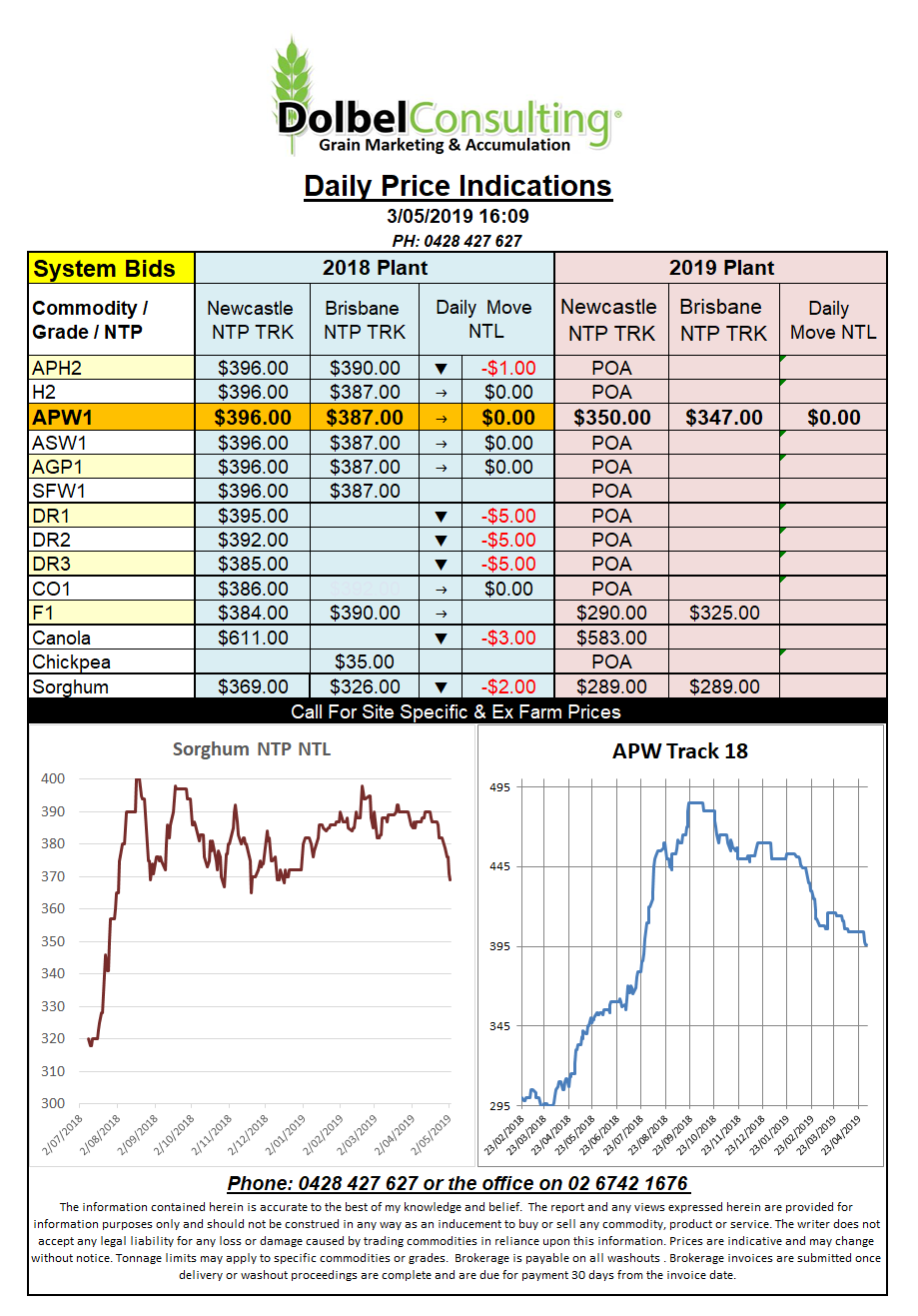

Prices 3/5/19

US wheat futures were torn between planting delays in the spring wheat, pretty meh weekly sales and export data and the thoughts that old crop wheat carry over may creep in higher than USDA projections thanks to lagging export sale execution.

On Monday the 10th the USDA will have their first official punt on 2019-20 wheat S&D numbers. The punters are calling lower acres but with better yields resulting in a similar ending stocks to what we are currently seeing. The net result is likely to be more of the same. There’s plenty of wheat to go around and prices could simply flat line, only spiking at domestic levels to draw grain onto the markets when needed. There is the prospect of grade spread variation but with Canada pulling out of canola and into wheat it’s unlikely we’ll become rich enough to retire at Byron Bay growing Prime Hard this year.

It’s often funny looking at the synergies between markets and what political influences are at play. I’m a cynical person at best and often conspiracy theories entertain me. For instance the issues between Canada and China which is reducing canola imports to China. The flip side to reduced imports is less meal to feed. Let’s consider ASF has seen the departure of around 140 million pigs. That’s a lot of feed they are not eating. Let’s also consider that China don’t have any issues with importing pork from Canada from the suppliers they like. For instance Canadian pork exports to China jumped 23% year on year in Jan / Feb.