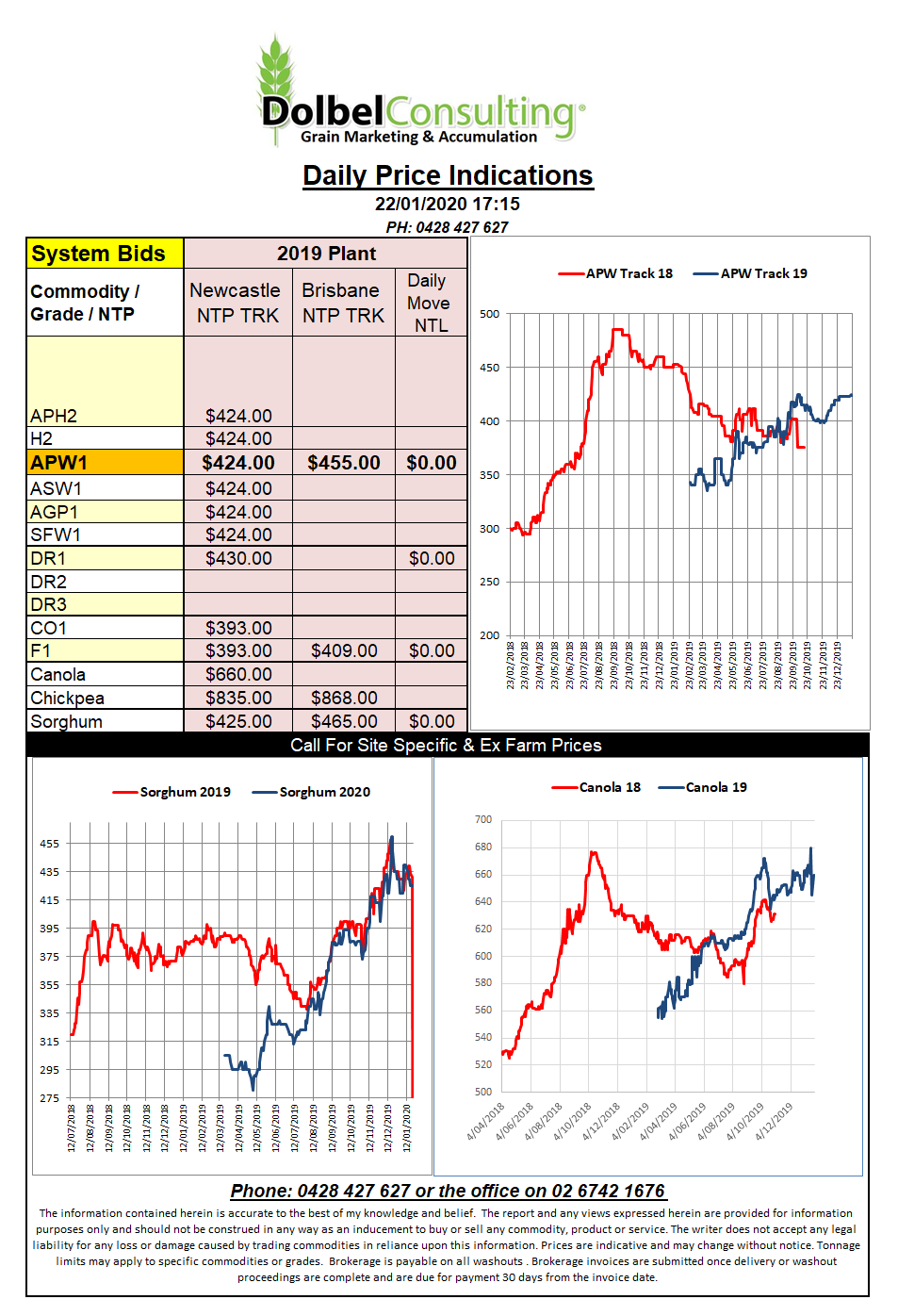

Prices 22/1/20

In the US corn and soybeans futures were lower while wheat futures in all three grades climbed higher.

Soft red winter wheat at Chicago saw impressive gains against the trend in the row crops. Fundamental support for wheat at these levels is a little questionable, especially with weekly export inspections out of the US falling 22% week on week to 435kt. Yet versus 2018-19 efforts the US export pace is still about 14% ahead. Asian markets remain the key to this pace at present. HRWW made up 199kt of US sales followed by HRS wheat at 124kt and then just 71kt of soft wheat.

Soybean futures at Chicago slipped away dragging corn lower. You can hear the punters saying it now “there’s been no caffeine fuelled mega buys from China yet and its already been a week”, patience grasshopper, patience, let the ink dry. The numbers do tend to suggest that if China is to buy the value of US agricultural products the trade agreement suggests than a robust buying program needs to come to life relatively quickly.

In Argentina producers have voted to suspend grain sales until the government reduces the newly introduced export tariffs. With the summer crops currently growing wheat appears to be the only major grain that will be impacted at present. Soybeans and corn exports tend to spike at harvest around April / May while wheat export volume peaks around the summer and early autumn months. Argentina failed to meet the record wheat crop many had expected to see earlier in 2019 after planting acres increased. Current USDA estimate show Argentine exports of wheat for 2019-20 are estimated at 13mt.