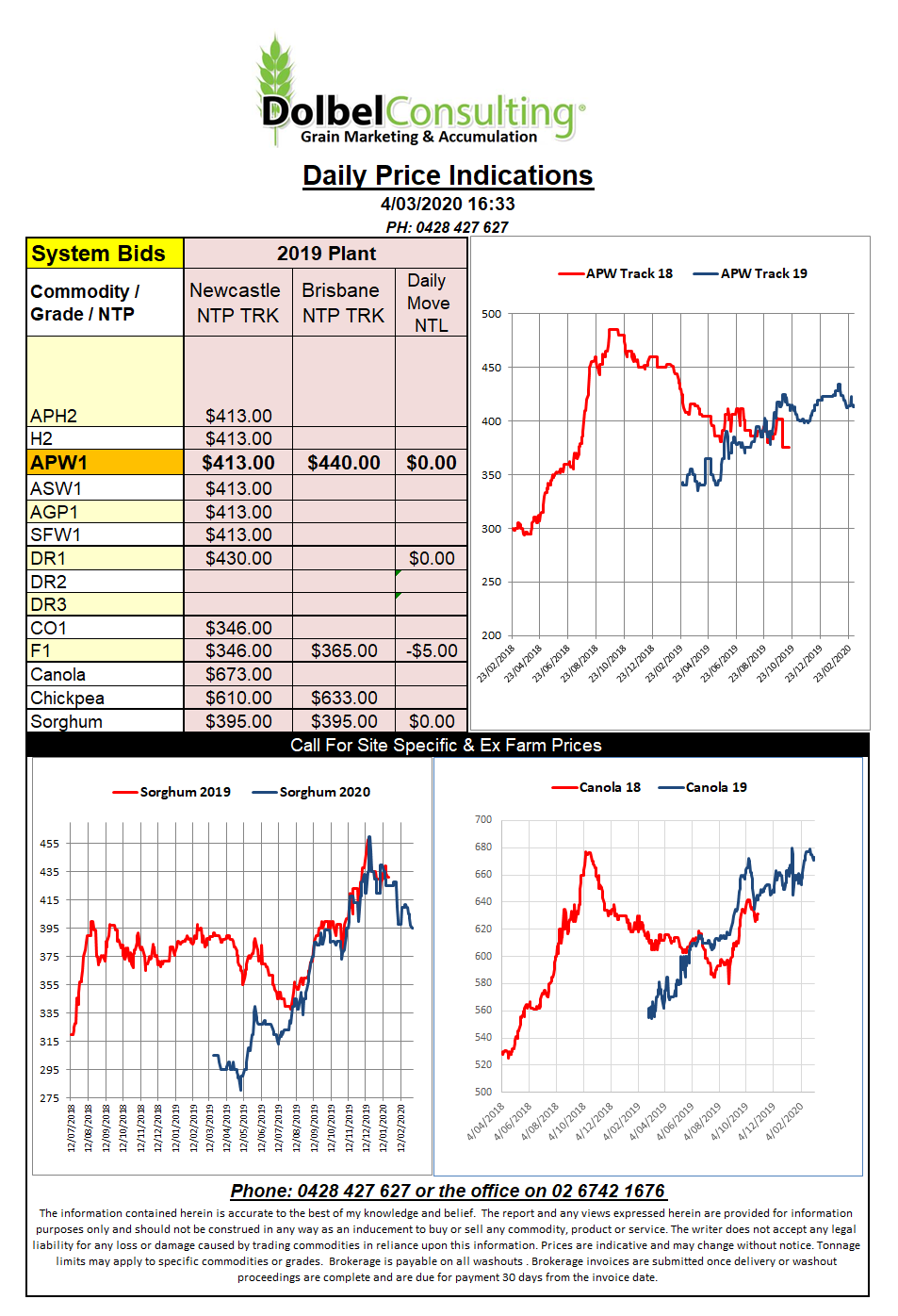

4/3/20 Prices

ABARES has pegged the 2020-21 Aussie wheat crop at 21.352mt, that’s a fairly rubbery number considering that there wouldn’t be too many seeds in the ground for another month or two. Domestic consumption is expected to slip back from 8.6mt to 8.45mt while exports increase resulting in a net reduction to carry over of 292kt, to just 3.071mt nationally. Export parity price is expected to come in somewhere around $255 ex farm LPP equivalent but we usually trade at a premium to that in NNSW unless it is a low grade crop. Increasing world and domestic demand is expected to put pressure on local stocks through to 2022. Nice crystal balling from ABARES, long way to go.

In the US grain futures were higher across the board with corn appearing to lead the way. Corn futures continue to recover at Chicago and are within reach of numbers prior to the coronavirus fall. Internal basis was generally flat to higher in the US but major buyers are picking and choosing at these levels which may create some resistance to US values going forward. A quick look at the May chart does show corn is now fairly neutral.

Chicago wheat was given a hand up by corn and a slightly lower US dollar. Improvements in wheat condition in Kansas capped the gains somewhat. Rated at 43% G/E Kansas is up 8% week on week. These ratings generally mean little until April though. Soil moisture across Kansas is ideal if not excessive in some of western Kansas. Oklahoma is a little dry in the SE while Texas is a little dry across the Panhandle but generally pretty good elsewhere.