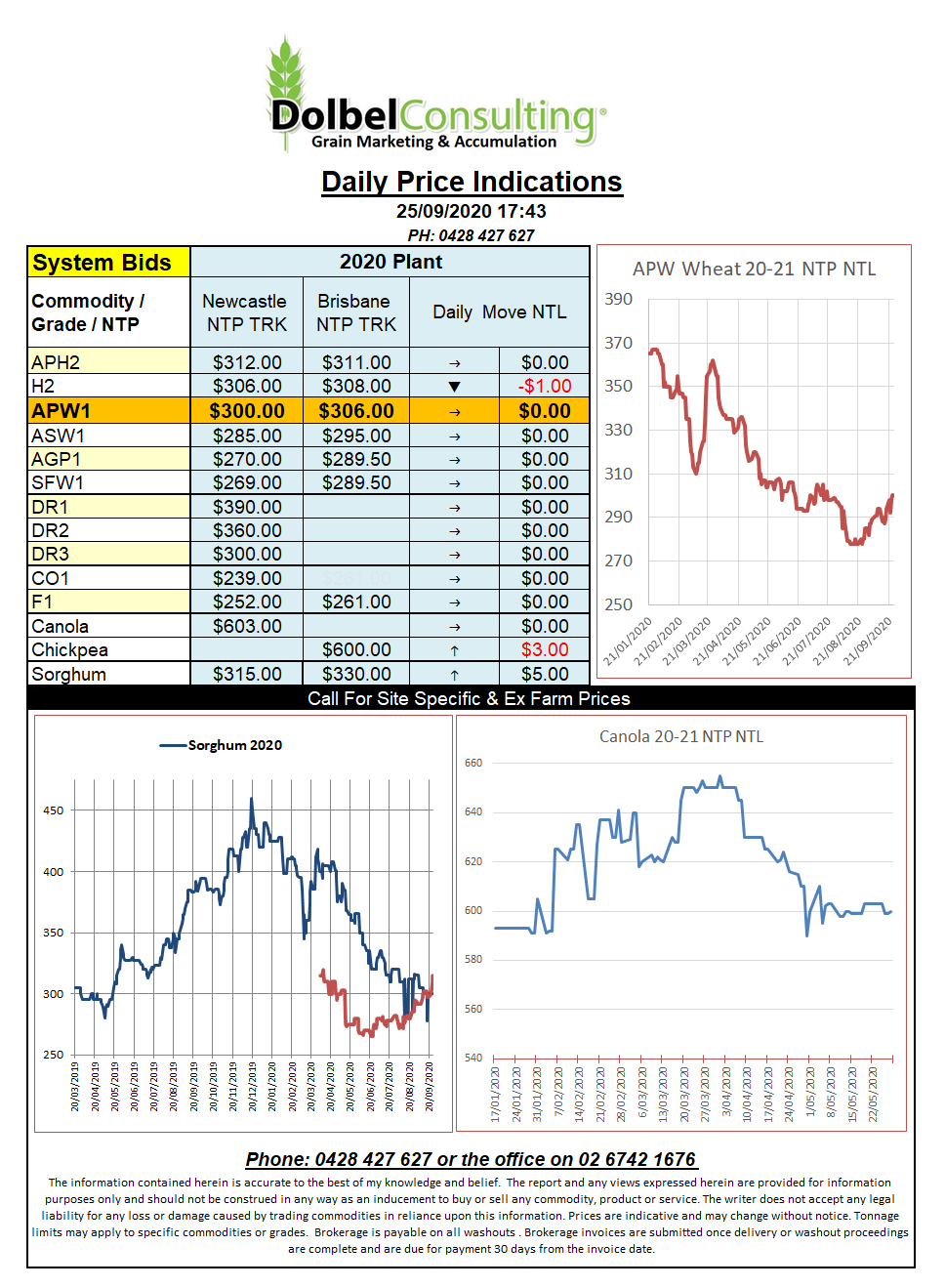

25/9/20 Prices

Double digit losses in Chicago soybean futures weighed on the market last night. The weaker close was attributed to profit taking. The weekly export data out of the states was fundamentally supportive but whose to stand between a fund manager and some end of month profit taking. Weekly US corn sales were noted at 2.138mt (China 566kt), soybeans 3.19mt (China 1.88mt) this is huge, wheat a poor 351kt.

Dry weather is persisting through much of the central US corn belt and western Texas. The driest regions continue to be the Rockies and adjacent grazing country. The increasing dry across the corn belt may play a bigger role in March / April 2021 when autumn sown crops start to demand sub soil moisture. Much of the Dakotas and Nebraska are also looking less than ideal. Not as dry as Argentina but worth keeping an eye on. Argentina is expected to see some rain next week but mainly across the Pampas region of Buenos Aires.

Wheat futures in the states done well to limit any downside and actually closed in the black for some contracts.

The International Grains Council, the EU equivalent to the USDA (if you asked them), had their monthly stab in the dark at global grain production and usage. The main point of interest was a reduction in global corn output. Reduced by 6mt month on month, production is now estimated at 1.16 billion tonnes (a new record). Reductions in the USA were the biggest influence but yield declines in the EU and China were also noted.

The wheat estimate was unchanged at 763mt, up 1mt on last year. Ending stocks were left unchanged at a very heavy 294mt.