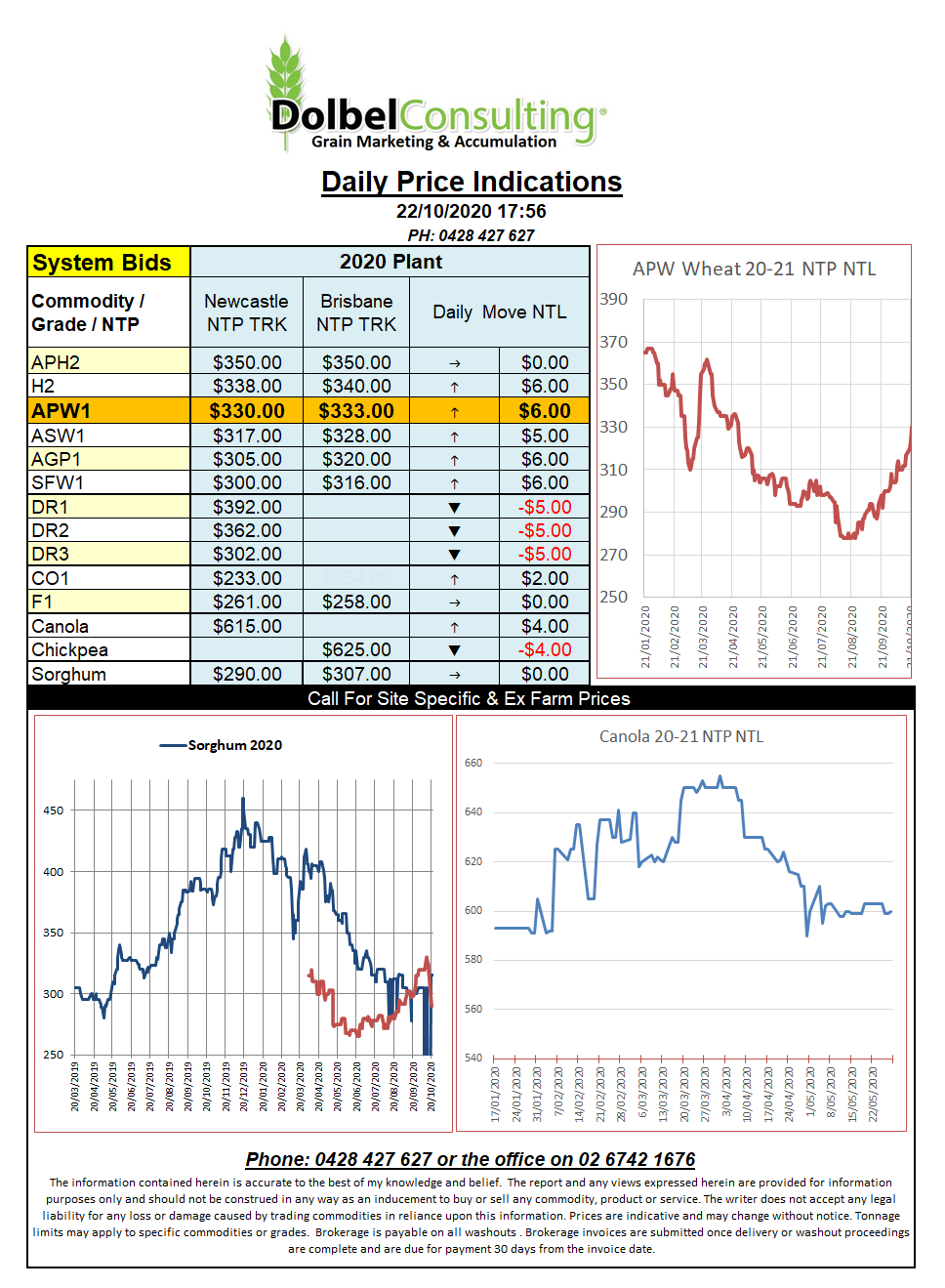

22/10/20 Prices

A combination of weaker low to mid-grade wheat futures at Chicago and a firmer AUD will keep a cap on prices today. Not that the local markets have been too wrapped up in benchmarking against US futures and basis of late. Hell, we can’t even get them to sustain a local basis premium over ASX wheat futures.

Looking at the cash market in SW Saskatchewan we see durum bid there at C$289/t for a December lift. This would convert to something like AUD$412 delivered Newcastle for DR1. Still comparing Saskatchewan values we see spring wheat with 13.5% protein at C$248 per tonne, if destined for somewhere like Japan this would equate to a value at Newcastle comparable to about AUD$335 port. So we did see a premium over N.Hemisphere red wheat yesterday, even if it was only AUD$15, for the first time in ages.

Hard red winter wheat out of the Pacific northwest would move into China for about US$300 FOB. This tends to point to higher grade wheat, like H2, probably being a little under-valued here. And then we have the feed market, probably something we need to keep an eye on for a week or two. Fortunately international demand for feed wheat (SFW1) remains very good.

There were tenders into SE Asia this week for both feed barley and feed wheat but values are not public yet. The Saudi’s booked 540kt of feed barley for Nov / Dec. The punters reckon Australian barley, at US$225.34 CnF. If supplied from Australia it will be sent from WA or SA. This converts to roughly a AUD$250 Newcastle port type of number. Pretty much where we were before yesterday’s weather spike.