26/10/20 Prices

Technically speaking Chicago soft red winter wheat futures for December have been over bought for a week or more now and if one was to use the historical time a contract stays over bought prior to expiry one might come to the conclusion that there is potentially a lot more chance for some downside than upside in the December CME soft red winter wheat contract from here.

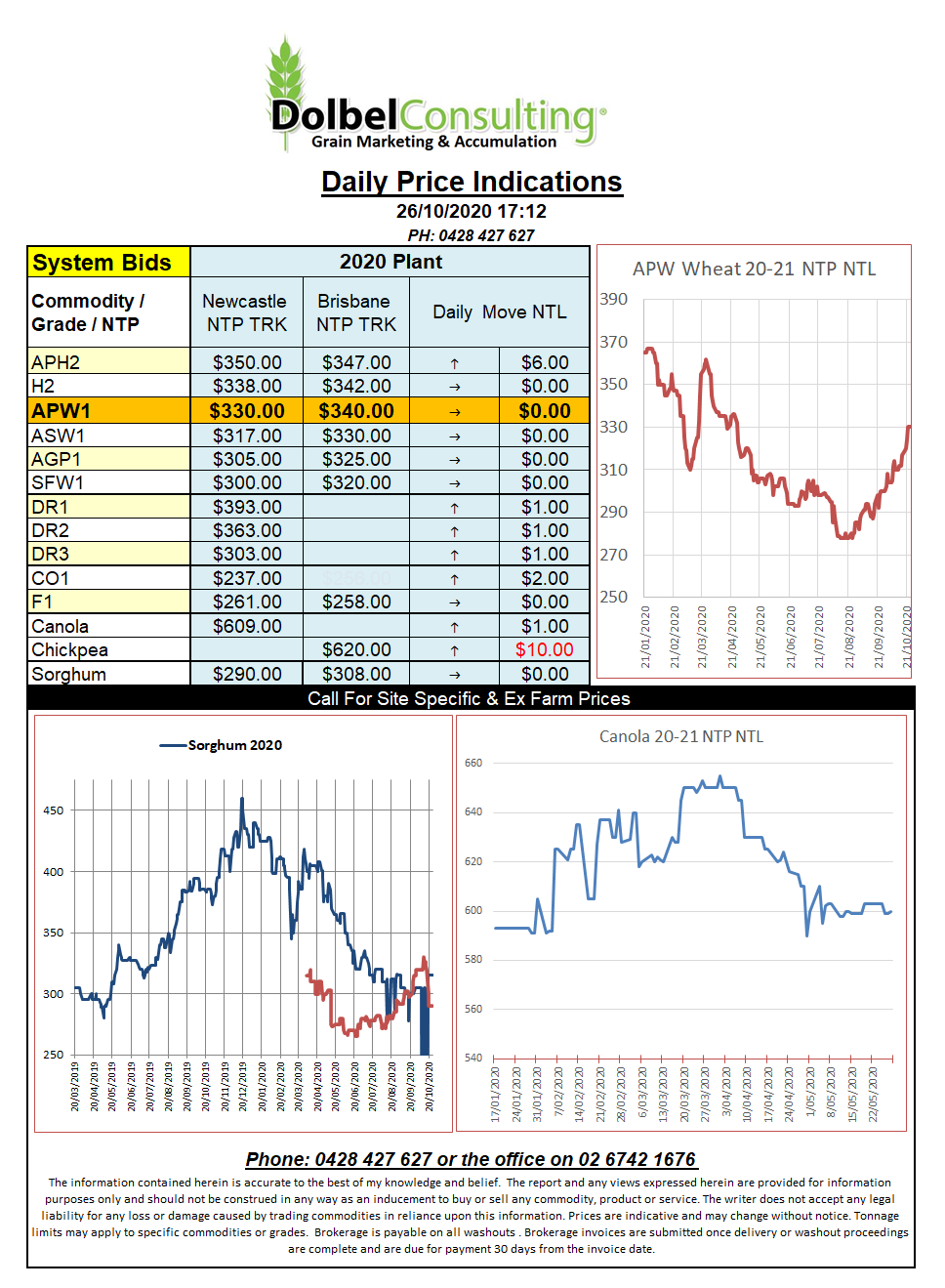

Not that the local guys have been sustaining a basis over Chicago to calculate cash bids anyway. Wheat, like local canola, has seen basis carved up as the cash price moved higher, smoke and mirrors ladies and gentlemen, smoke and mirrors. I guess the futures market has only had a loose correlation to reality for some time now anyway. Chart attached. Basically if August basis had of been sustained through to now current cash bids here could potentially be around AUD$20 higher.

Let’s not dwell on the futures market though, looking at cash bids we see HRW offered out of the Pacific Northwest of the USA bid at US$273 FOB. As a means to compare we will assume this wheat can move to Japan, if this is the case than it would be comparable to a delivered Newcastle port number of roughly $345, roughly AUD$15 higher than current cash bids. It should be mentioned that premiums for US wheat with protein of 13% to 14% over 11.5% wheat is not huge. Which tells us that with the current value of APH2 at the port being AUD$350, neither is our premium.

Cash bids for Canadian durum were flat to firmer, spring wheat firmer by a couple of C dollars and canola out of SW Saskatchewan was C$2.86 firmer for a December pick up. The premium for 1CWAD (durum) with 14% protein over 13% was roughly C$7.35.