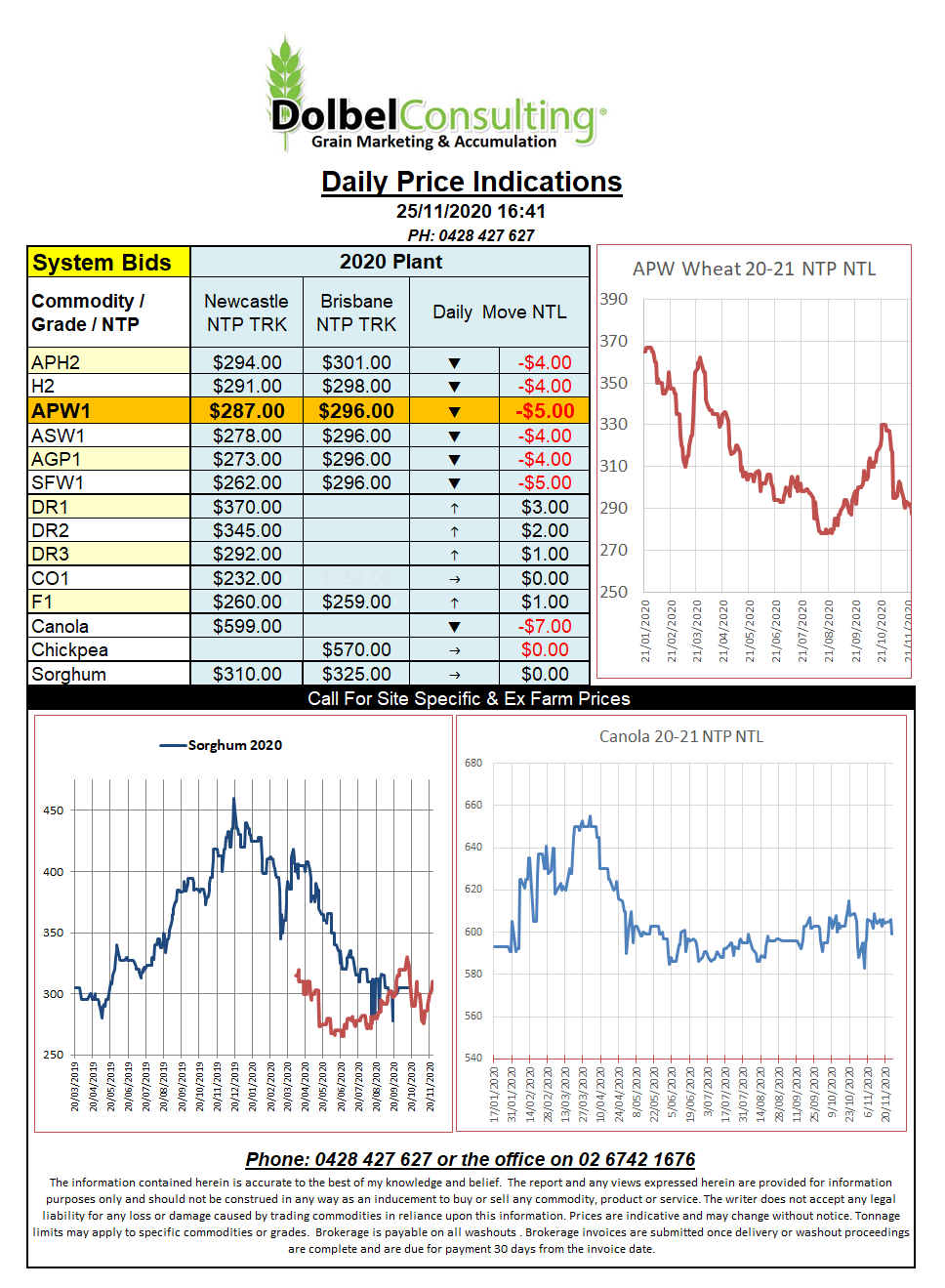

25/11/20 Prices

Futures markets, price indicators or playgrounds, I often wonder. Look at our own ASX. Yesterday there was 29.3kt of Jan21 wheat traded and 29.6kt of March 21 wheat. The price trended lower throughout the day. Looking at the volume and sale times one could come to the conclusion that just 2.3kt, 7.85% of the total January business, was not wheat being rolled into the March slot. Of the total March volume 8.78% was not easily identified as rolled grain. All of both the Jan and March volume may still have been getting rolled.

While on obscured marketing messages from futures markets we can’t exclude the CME exchange at Chicago where SRW futures rallied over AUD$6.00 / tonne last night. We also see, the yet to be traded, Australian Wheat FOB (Platts) APW1 futures contract at Chicago close US$3.00 higher for a Feb slot. Settling at US$263.25 FOB, a number that would equate to an APW1 ex farm price on the LPP of close to AUD$287 per tonne. In reality if a grower could sell APW1 for $270 ex farm LPP yesterday (which was possible) they were doing OK.

Cash wheat prices out of the Pacific North West of the USA, wheat destined for Asian markets, trended sideways to firmer. White wheat for a Feb loading was bid at US$6.37/bu. If using Japan as the destination one can convert this back to an Aussie port number comparable to AUD$295 port, so the $300 port bid for APW1 yesterday wasn’t that bad. Still at the PNW ports we see DNS with 14% protein bid an average price of US$6.95/bu, comparable to AUD$325 Newcastle port. Currency threatens to spoil the show today.