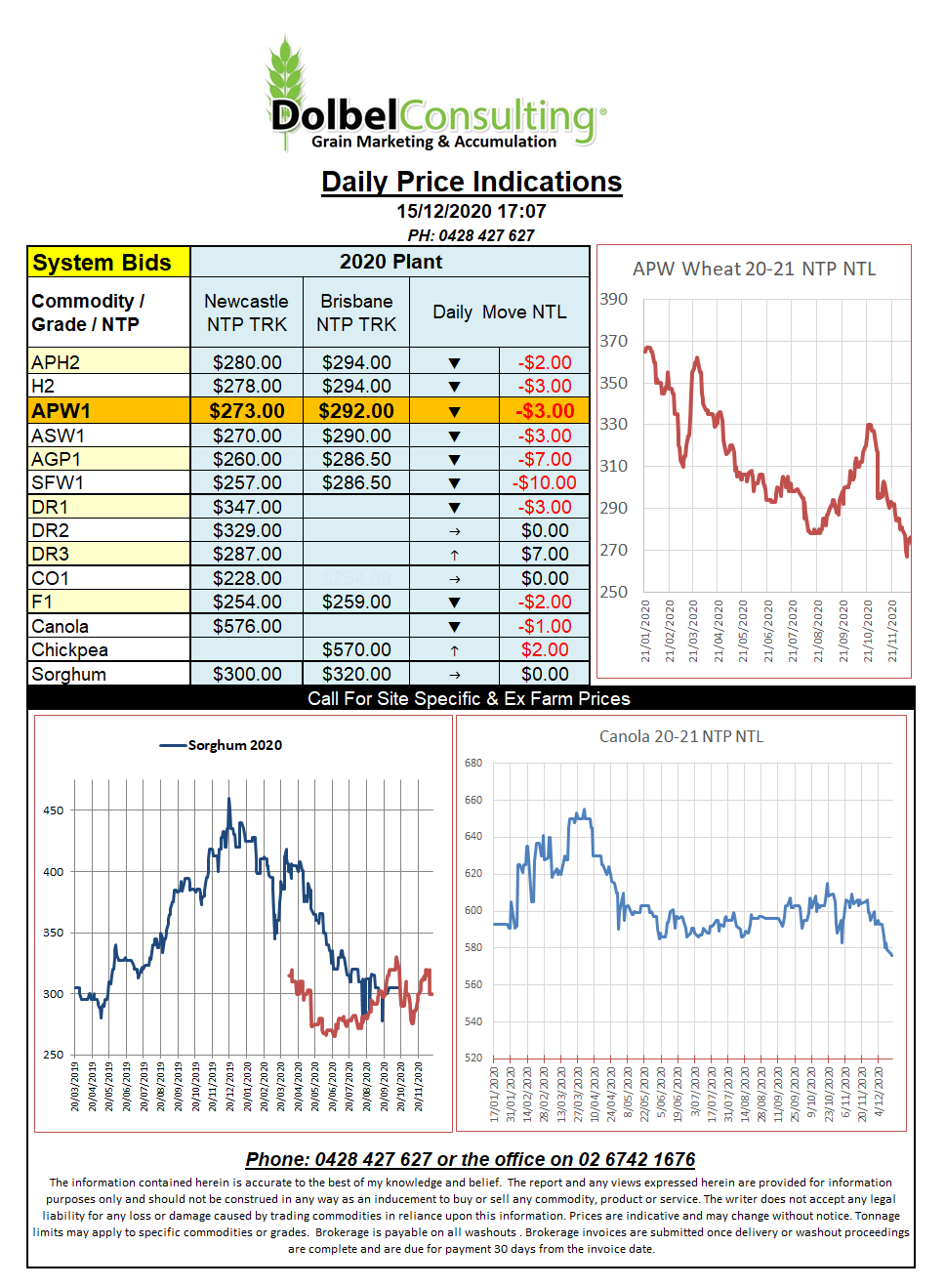

15/12/20 Prices

With the December contract rolling off the board the USDA report appears to be long forgotten. US wheat futures were smashed overnight with SRW, HRW and spring wheat all taking a hit by the close. The Platts APW1 FOB Aussie wheat contract for the Feb slot was up US$0.50 / tonne to US$260 by the close but this contract still remains untraded. Well apart from 1000 contracts in March 21 that were done so long ago I’ve forgotten when. It will be interesting to see if this is a small dip in the chart as wheat marches higher or if there is continued resistance at the March 600c level in January. Paris milling wheat futures also struggled, shedding E$4.25 in the March slot.

Cash bids out of the Pacific North West were generally lower for HRW and spring wheat while white wheat values held on and were mostly unchanged. White wheat bids indicate a comparative value for APW NTP / NTL of close to AUD$295. This would be some $20 better than what we are currently seeing as a cash bid on the track and if anything confirming that Aussie wheat is still very cheap and will, at these values, continue to out place most other suppliers into the Asian markets.

Russian milling wheat is priced at roughly US$255 FOB for a 12.5% protein. Ukraine wheat with 11.5% protein is priced at roughly US$250 FOB. The Ukraine product could move by water to China for something like US$281 CnF. This would equate to an Aussie port equivalent of somewhere around AUD$314. Yesterday H2 was bid at AUD$280 port, that’s leaving a fair trade margin in the equation.

Russian and Ukraine weather remains abnormally dry, many are predicting a big winter kill year in the winter wheat there.