20/1/21 Prices

Chicago soybean futures were back 31c/bu on the nearby contract overnight. Profit taking kicked off early with their overnight session seeing some downside before the trend carried over into the main day session. A quick look at the stochastic chart shows there is still plenty potential downside left in beans from a technical perspective but strong demand from China should continue to underpin this market mid to longer term.

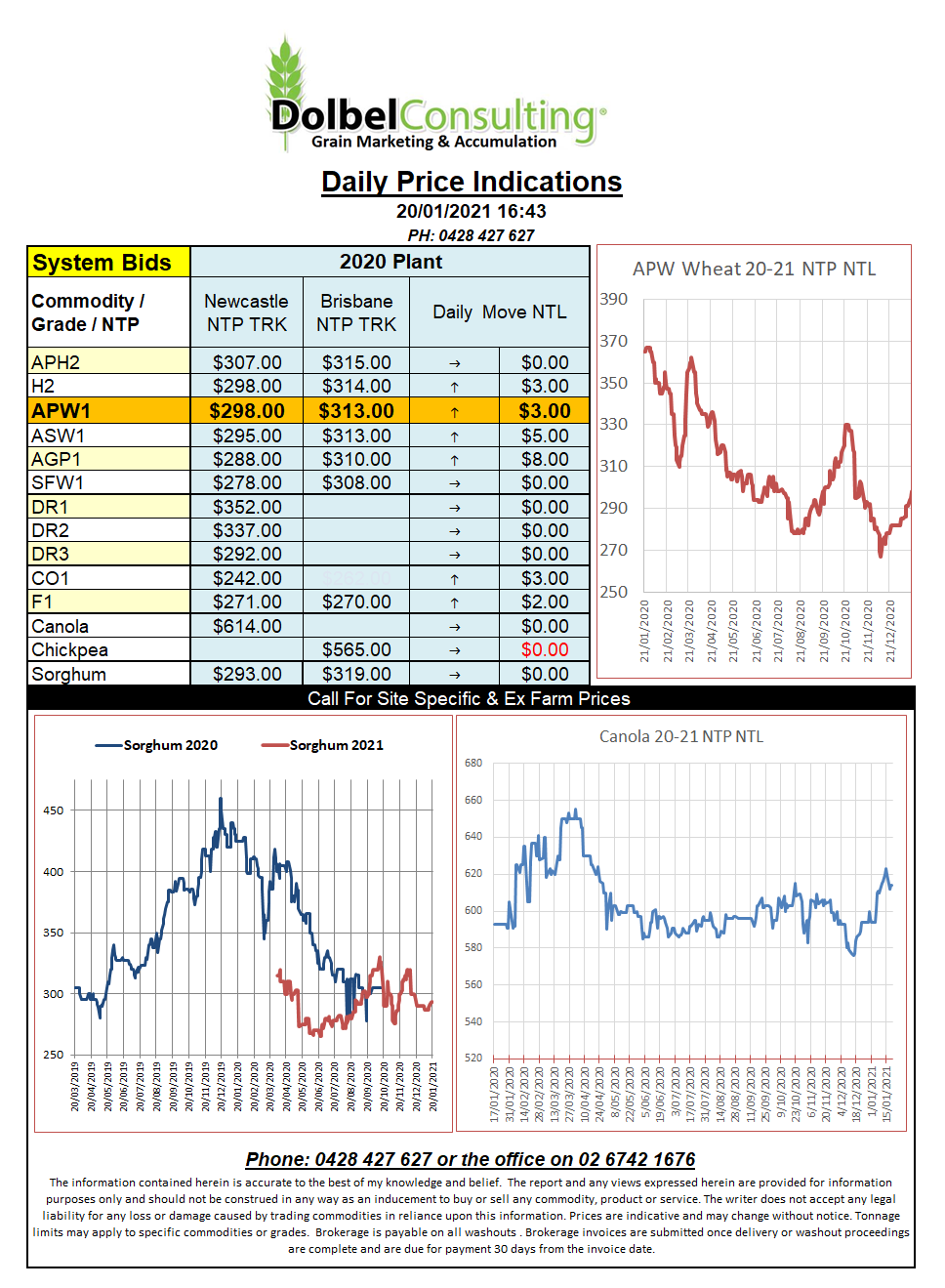

Wheat futures were mixed, soft red winter wheat at Chicago was a little softer while HRWW and DNS wheat were a little firmer. Cash prices for HRWW out of the Pacific North West of the USA were flat to firmer at US$7.87c/bu delivered river. Using Japan as a destination this would be roughly equivalent to about AUD$354 for a H2 type wheat delivered port. Yesterday H2 wheat here moved at $316 into the port. DNS, spring wheat, their higher protein wheat is about AUD$8.00 under HRW values due to internal frieght differentials from growing locations.

White wheat out of the PNW was there at about US$7.11/bu or an Aussie port equivalent of about AUD$317, pretty much on par with Aussie values for wheat moving into NE Asia.

Interesting to note corn values out of the PNW, at US$6.46/bu it does work back to about AUD$316 Newcastle port equivalent. With Dalian corn futures in China closing at Y2869 or AUD$575.58/t you can see the attraction to US corn or sorghum and potentially Aussie sorghum in the short term. In the past the Chinese have paid up to about AUD$50 above corn for Aussie sorghum. It’s a fair bit trickier these days to call this an easy sell though.