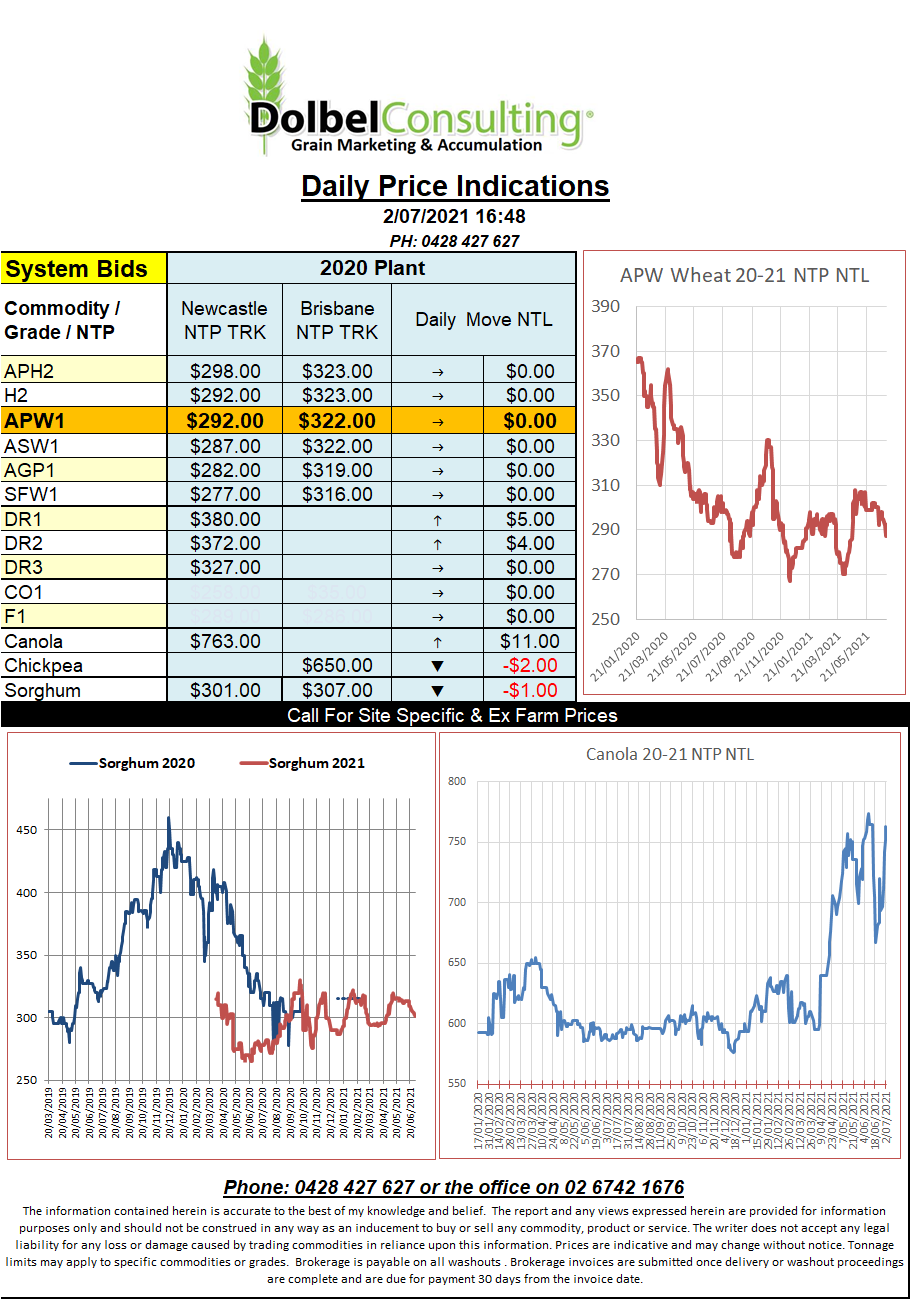

2/7/21 Prices

A night of profit taking as the funds moved money out of grains and back into Wall St.

Wheat was hit the hardest as it was generally a follower of the row crops on Wednesday. Hard and soft wheat futures at Chicago closed lower than spring wheat futures at Minneapolis. If should be mentioned that MGEX spring wheat cash bids were actually 30.25c/bu higher overnight, closing at 979.75c/bu (AUD$482), while futures there drifted lower in line with the wheat contracts at Chicago.

Export bids out of the Pacific North West of the USA saw DNS wheat followed the MGEX futures market lower. A Sept bid at the port averaging 940c/bu. This would be comparable to an APH1 bid of roughly AUD$427 at Newcastle port. New crop APH2 on a multigrade contract was bid at $317 less rail yesterday.

Over the northern US border and into SE Saskatchewan we see 1CWRS 13.5 spring wheat cash bids also followed futures lower with a Dec21 lift averaging an ex farm price of C$333.07 according to PDQ. Using Japan as a destination this cash bid would basically equate to a Newcastle port number close to AUD$420 so very much in line with US prices out of the PNW and still well ahead of Australian values.

Since the start of May new crop APH basis over MGEX has slipped over 80c/bu, that’s almost AUD$40/t, the start of a US drought premium.

Durum values out of SE Sask were relatively unchanged at C$328.72/t for a Dec21 lift and indicating fair value for new crop at the port here would be about AUD$420, depending on unloading port location. Old crop has recently been bid as high as AUD$400 at the port, this does tend to back up this comparison. In SE Sask there is little difference between old and new crop durum bids.