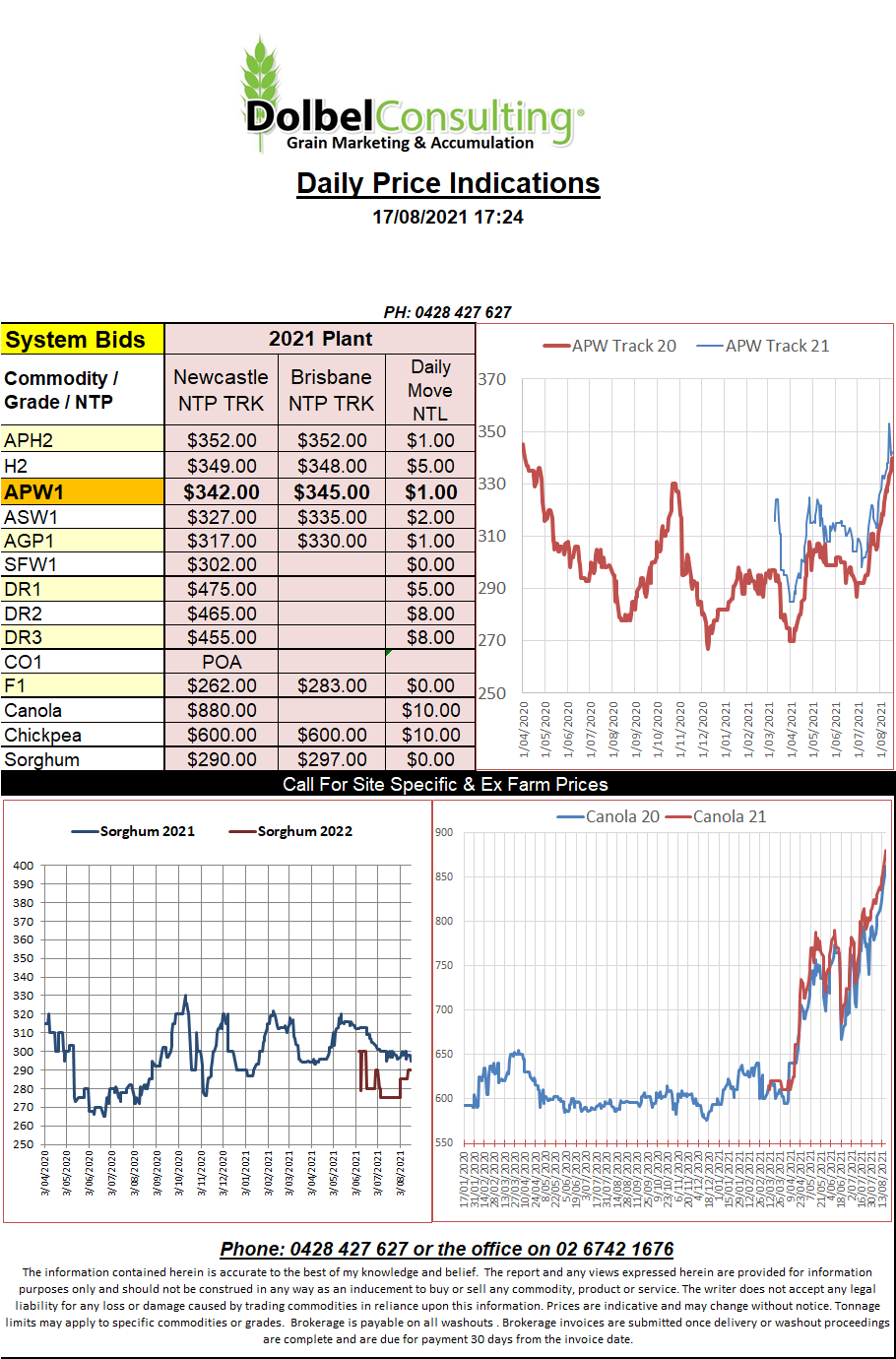

17/8/21 Prices

US grain futures took half a breather overnight, bar soybeans which continued to move higher. The big mover continues to be canola / rapeseed. ICE futures for Canadian canola pushed through C$900 to close the session C$18.10 higher on the nearby at C$912.40. Paris rapeseed futures were also sharply higher with the Feb22 contract putting on E6.00/t to close at E565.

Sunflower seed FOB Black Sea from Ukraine was valued at US$648 per tonne for prompt delivery and less US$35 for a December lift. Ukraine sunseed values are still well below the May high set at over US$800/tonne.

Feed barley out of Argentina is offered into China at US$341 per tonne C&F. Values at this level do tend to indicate there would be a better prices on offer into the Australian ports if we had access. Looking at barley values around the world we see Aussie feed barley would move into China at roughly US$265 FOB China (if able), US barley out of the Pacific North West would be worth roughly US$261, Russian barley out of the Black Sea would be worth about US$322 FOB China.

The only real question these comparisons really bring to my mind is why are we competing with US barley. Last night’s crop progress report showed US barley rated at just 23% G/E. Washington, in the PNW, rated at 0% G/E and 66% Poor / Very Poor.

River levels in Argentina are causing issues. EU barley won’t work, it’s already US$60 per tonne more expensive the Black Sea barley and SFW1 wheat isn’t an option price wise. Aussie barley is even US$20 cheaper into Saudi Arabia than Russian barley.