8/12/25 Prices

International milling wheat values continue to slip away as supply becomes larger. The Platts Milling Wheat Marker has fallen to it’s lowest level since mid September on the back of increased volume, and lower FOB values from the Black Sea. The marker is determined by the lowest offers of both Ukraine and Russian milling wheat.

The lower values for Russian wheat has seen an increase in export sales. Buyers so far happy to take advantage of low international values. In November Russia exported 5.5mt of wheat, 200kt more than Nov 2024. Turkey, Iran, Egypt, Bangladesh and Saudi Arabia all major buyers. Demand is expected to remain strong for December. Russian Dec exports are projected to be at least 200kt better than Dec 2024, currently estimated at 4.3mt.

Domestic values in Russia have presented some accumulation problems for exporters at present values. Producers not entirely happy with current values, resulting in the trade struggling to make a significant margin in export business, thus reducing port volume a little……… my heart bleeds.

Competition from Argentina may further reduce milling wheat margins. Argie offers to Asia were stated as being as low as US$262 CFR. Some saying that the quality of Argentine wheat versus Russian wheat means that Argie wheat needs to be at least US$10.00 cheaper than Russian wheat to buy Asian business. Last night’s decline in Argentine milling wheat FOB values basically cements Argie wheat as a viable option into the less discerning Asian markets.

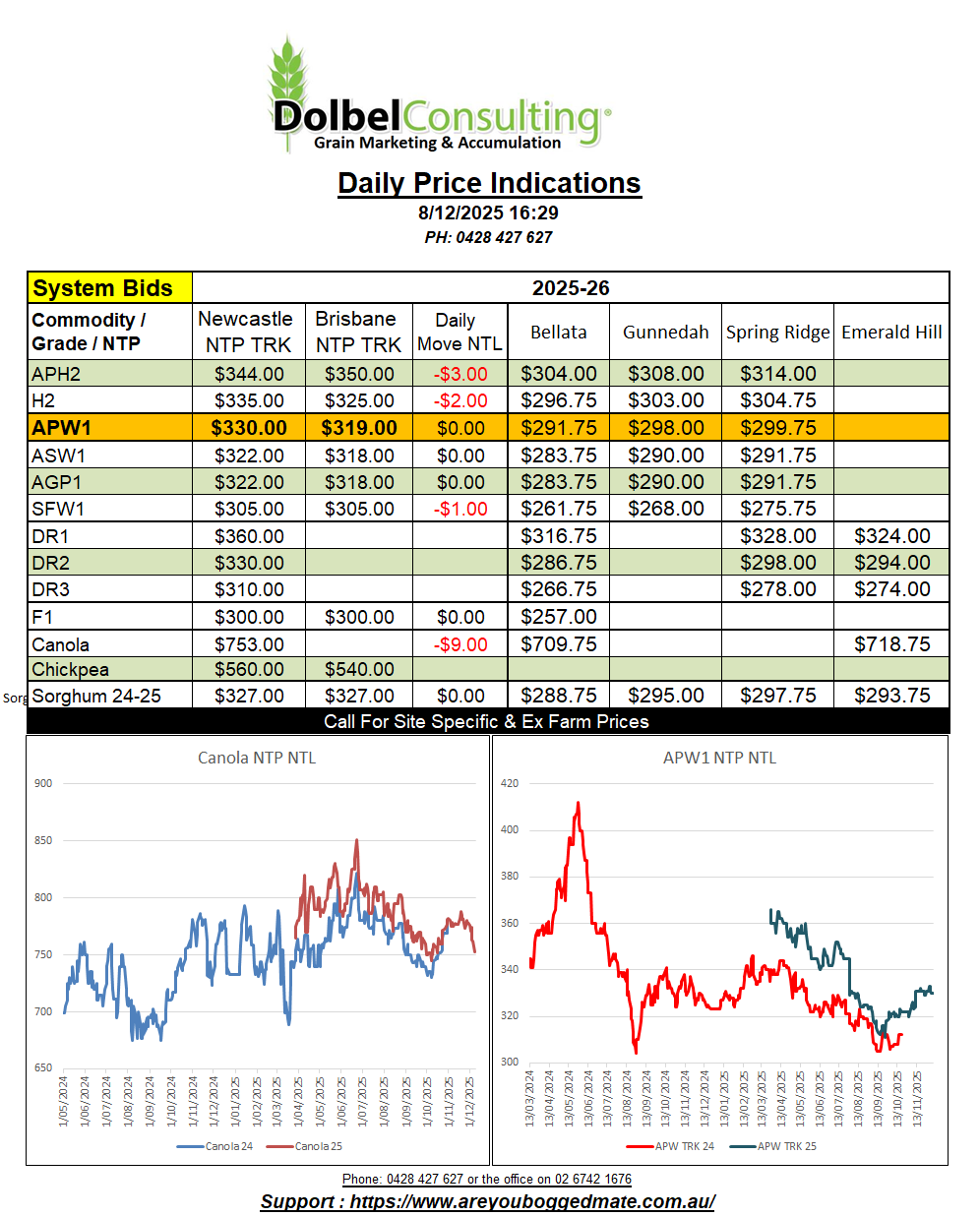

On the back of an envelope a CFR US$262 value into Asia would equate to an XF LPP value of something close to AUD$300 to AUD$305. The current H2 bid of AUD$360 port Newcastle equates to about AUD$320 XF LPP, possibly suggesting a white wheat premium of AUD$15 to AUD$20 is being achieved.

US club white wheat was valued at US$275 C&F Asian buyer last night, roughly US$2.00 to US$3.00 higher than Aussie H2 to the same destination.