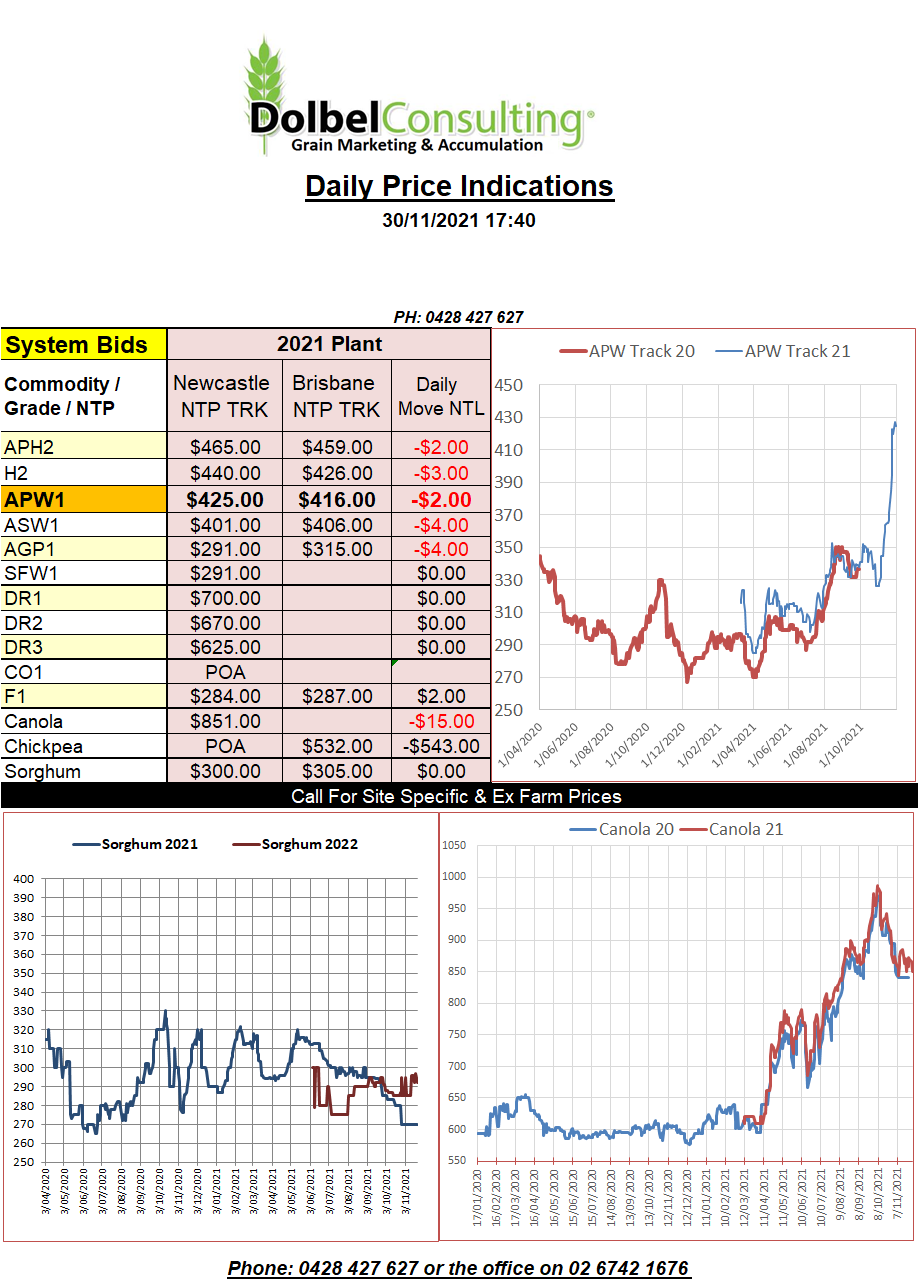

30/11/21 Prices

Grains appear to have been caught up in the general market sell off in overnight trade. The financial markets were caught up in the narrative that the new variant of covid could interfere with the global recovery from covid19. So many “if’s” in world markets at the moment that price discovery and forecasting remains difficult. I’m starting to run out of chicken to blood and iguana bones.

The ABARES report also put pressure on world wheat prices.

ABARES data hit the market last night, better late than never, not really, this report is now basically useless given the weather of the last fortnight. In the report ABARES predicts the Aussie wheat crop at 34.4mt, yeah good luck with that. There’s more of a chance of me buying a new Mercedes with grain brokerage from this year’s winter crop than that figure being seen in 2021 (both odds are very, very low).

So ABARES pegged NSW wheat at 12.2mt, just yesterday I heard trade estimates as low as 7mt, which I thought might be optimistic.

Why this report was even released without some mention of the major flooding across the eastern states is beyond me.

In overnight business we see Egypt picked up 600kt of milling wheat. Romania 240kt, Russia 240kt and 120kt from Ukraine for January shipment. Russian wheat was the cheapest and almost the most expensive on offer. Prices ranged from US$351.37 FOB to a high of US$361.95 for French wheat. Black Sea frieght remains relatively high at around US$26 +/-. Using a mid-point of about US$355 FOB BS as an indicator we can determine roughly what this value would equate to XF LPP, which is about AUD$400 XF equivalent here.