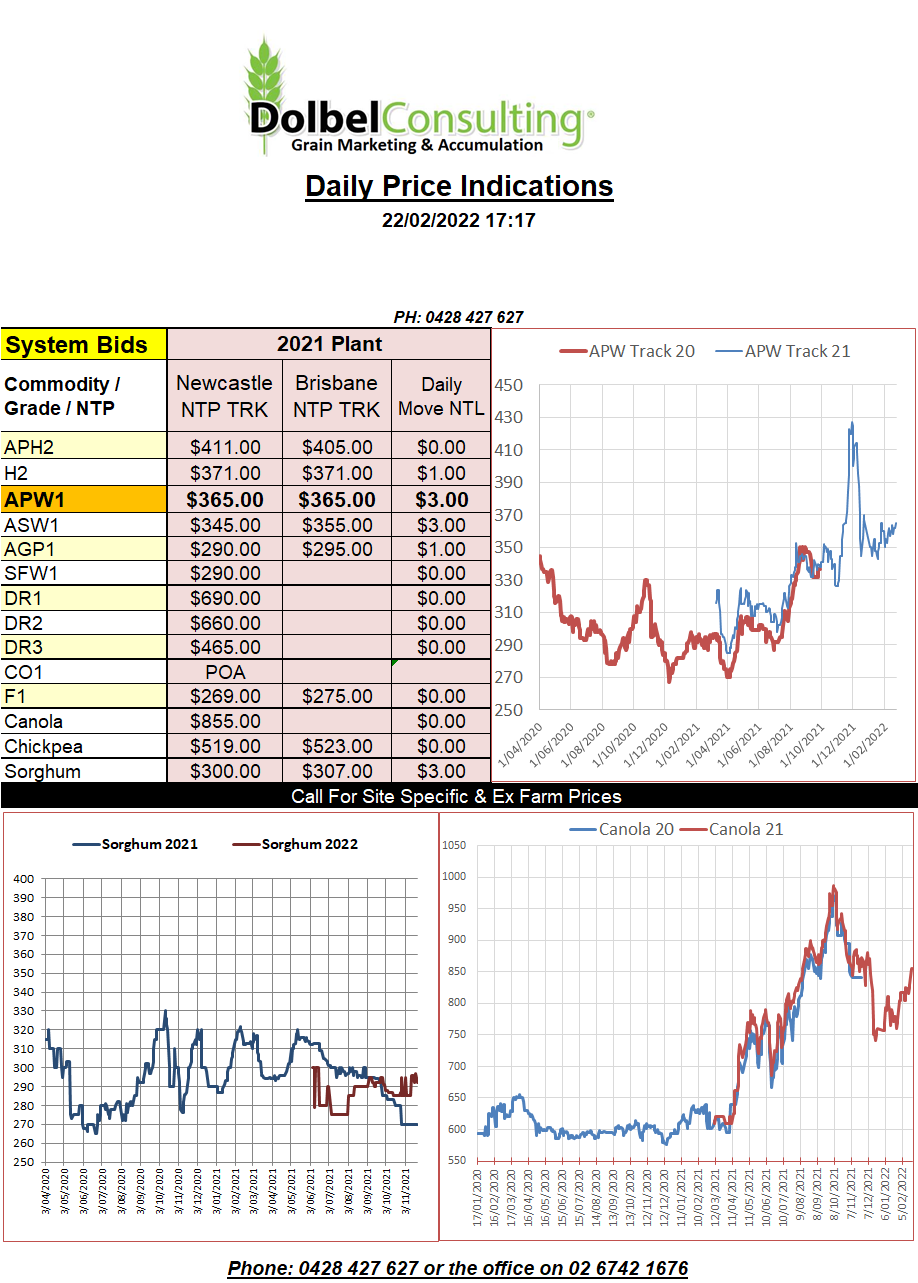

21/2/22 Prices

Chicago hard red winter wheat futures were the clear winner in last night’s US futures session. Closing 12.25c/bu (AUD$6.26) higher on the nearby and 11c/bu (AUD$5.62) higher in the Dec 23 slot. 1CWRS13.5 Canadian wheat spread March / Dec is C$49.00.

The IGC wheat stocks chart for the major exporters is probably the only chart you need to see to understand why international wheat prices have persisted at such high levels for so long. With China holding almost half of all carry (wheat that will not make it onto the export market), the stock level of all the major exporters is very important. Currently we see this value at a nine year low after four years of major issues in a row. Two years of drought in Australia started the ball rolling, drought in Canada a major factor last year.

The stocks to use ratio in these 8 major exporters is now just 15%, falling from a high of almost 21% in 2017-18. Increasing stocks in Australia and Russia over the last two years, the only real change that stopped this from becoming a major supply problem in 2022-23.

Back at Chicago we see the down grade in S.American soybean production rolling through to a higher close in soybeans. This in turn pushed both Winnipeg canola and Paris rapeseed higher. Looking at Canadian values we see cash bids for the old crop ex farm SE Saskatchewan were up about C$10 for nearby delivery. Locally we did see a slight improvement in basis to both Paris and Winnipeg but we are still looking at exceptionally poor basis compared to traditional basis, even for new crop.

The Ukraine / Russia hype remains support to the narrative but has not resulted in grain movement restrictions from the Black Sea as yet.