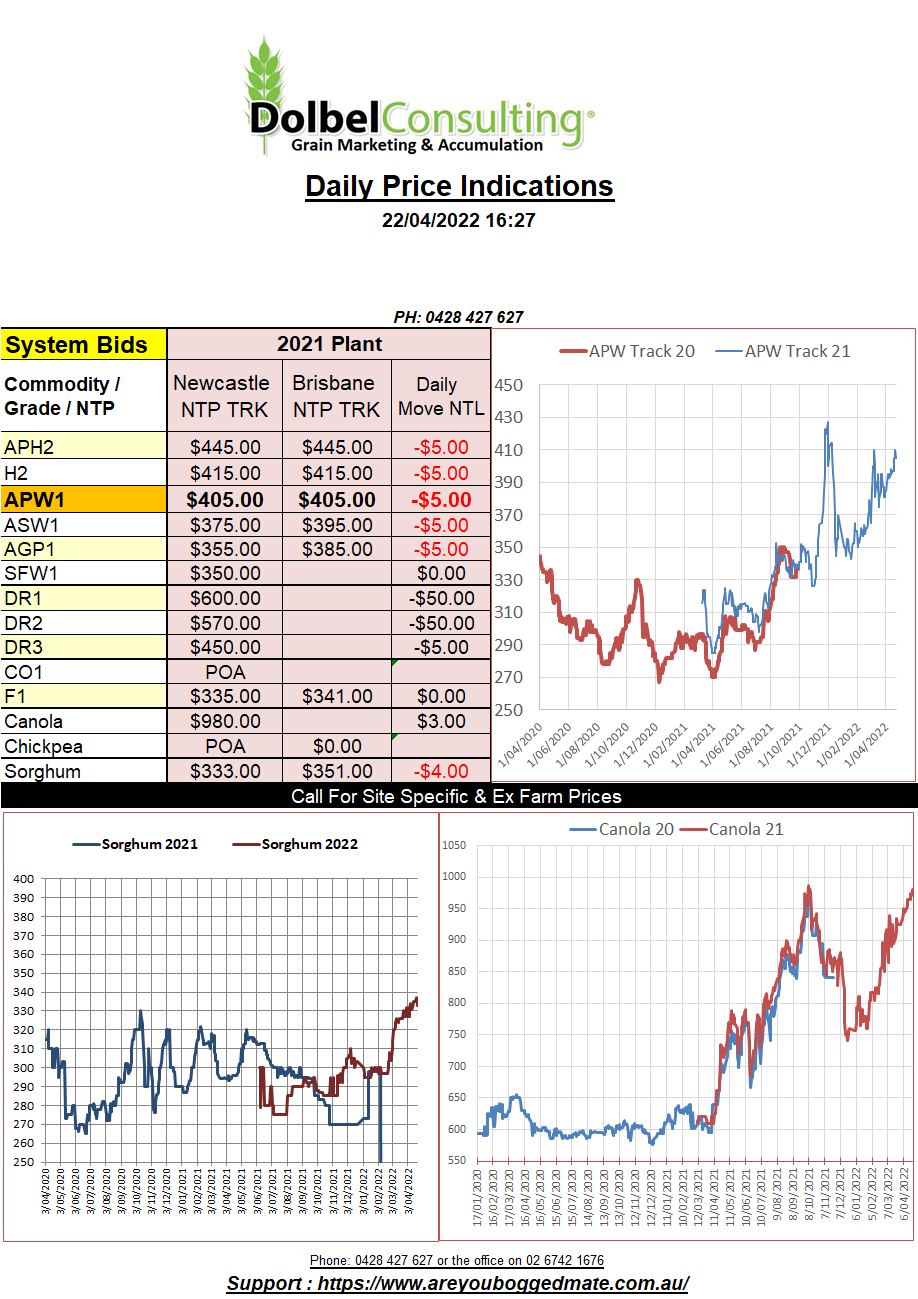

22/4/22 Prices

The US futures market saw some profit taking dominate wheat futures in overnight trade. One needs to remember that longer term, futures prices spend less than 5% of their existence, if any time at all, in the top 30% of historical prices.

Those long wheat futures at these levels will be nervous.

The current rain forecast in the US and Canada could be adding to that nervousness but the map is a little mixed. The US spring wheat belt looks likely to see around 50mm over the weekend. This rain could also push north into the SE corner of Saskatchewan. Western Kansas and much of Nebraska look likely to miss it again though.

Fundamentally poor export volume from the US in their weekly report wasn’t helpful. Wheat sales out of the States hit a marketing year low and corn sales were also disappointing. High prices fix high prices, just like low prices fix low prices……. in time.

The International Grains Council had their monthly stab in the dark at the global grain S&Ds. Wheat ending stocks were pegged at 277mt, a 5mt reduction from the previous year. Year on year global wheat production is expected to be back just 1mt to 780mt. Oddly enough the IGC did not show individual data for Russia or Ukraine. Private forecasting firm, Sovecon, predicted Russian wheat production could be as high as 87.4mt in 2022, resulting in exports of 41mt during 2022-23. The increase in exports year on year is significant, 33.9mt vs 41mt, a 7.1mt increase. Potentially counters any reduction in Ukraine wheat production. Ukraine’s ability to sow, harvest and export the volume of wheat they could prior to the Russian invasion and demolition of important export ports like Mariupol remains questionable.