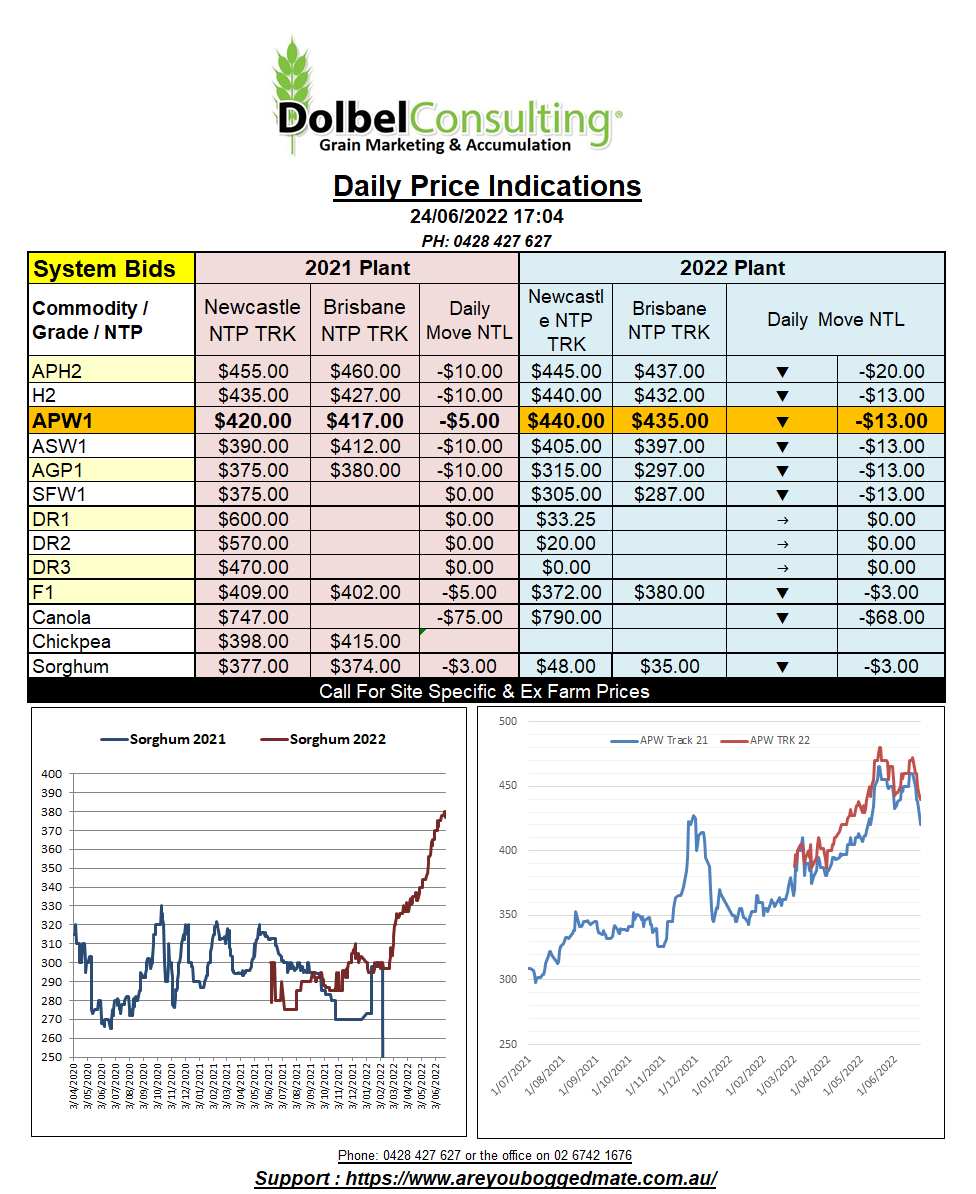

24/6/22 Prices

It’s taken a while but sooner or later the US wheat market had to come to terms that the punters got it wrong, and the prevention of Ukraine wheat exports wasn’t going to create a world-wide disaster. I’ve been on the other side of that narrative for a while now. I hope everyone enjoyed it while it lasted.

The realisation that the world is not on fire, that US wheat exports haven’t jumped through the roof. Prices didn’t rally for any other reason than a Canadian / N.USA drought last year. Some suggest US wheat prices are still some AUD$80+ higher than where they should be given the current world supply and demand situation. For example spring wheat out of the US PNW is over 200c/bu (over AUD$106) above where prices were this time last year. These are just a few of the reasons we are now seeing the managed money rushing for the door.

Overnight grain futures in the US were crushed yet again. The canola and rapeseed market left bloodied on the floor yet again. ICE canola futures at Winnipeg were the hardest hit. The January 23 contract shedding over AUD$75, a massive fall. Paris rapeseed slipped over AUD$53 for the Feb23 slot. These are big, big falls. Outside market influence, decreasing Chinese demand, export competition from Brazil, better weather in some major producers, these are all fundamental factors that have been evident for a little while now. The US farmer must be feeling pretty ripped off, this crash occurring smack bang in the middle of wheat harvest and only now after the summer crops have been sown, all with record high input costs.

The fall wasn’t restricted to the US markets though, Paris milling wheat futures fell over AUD$16 for the December contract. Even London feed wheat values were softer, setting a contract low overnight.

Technically Chicago wheat is neutral, the stochastic turning on last night’s session, whether this helps or not is anyone’s guess.

Another large grain storage facility in SE Ukraine, Rubizhne, Luhansk region has been destroyed.