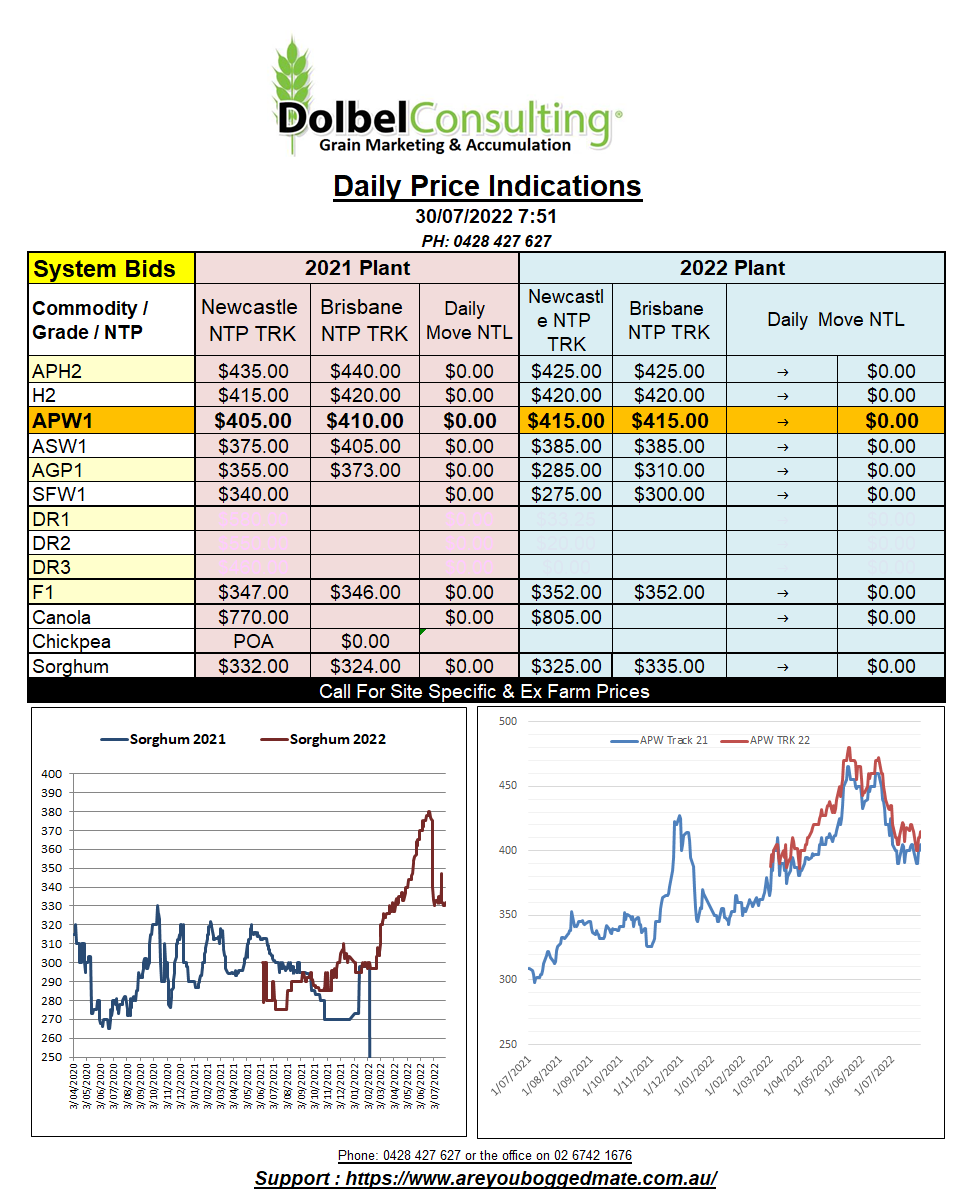

29/7/22 Prices

It’s all about soybeans, canola, and rapeseed this morning. There were some impressive gains at Winnipeg, the Jan23 contract pushing C$39.00 per tonne higher. Paris rapeseed futures were also firmer by the close, the Feb23 slot up E11.00 or about AUD$16.04 per tonne. Not as impressive as the ICE contract but a move in the right direction. Chicago soybeans continue to push higher, the Jan23 slot up another 31c/bu by the close, roughly AUD$16.30 per tonne.

The return of heatwave conditions to the US had the row crop punters on the defensive. Corn futures also closing with double digit gains at Chicago. Some basis in the US was lower, cash buyers not convinced next week’s heat is worth the extra futures gained.

The weaker basis for US cash prices up country was also a feature on the soybean market. The physical market for beans mostly not convinced that the futures market at Chicago is reflecting actual fundamentals correctly….. again.

Fundamental support for wheat was on the back off, go on, take a guess…… “thoughts that Ukraine exports may not happen as quickly as previously expected”. This is the part where I insert a picture of Homer Simpson going DERRR.

US wheat export sales week on week were back 29%. This week’s rally in futures not helping to increase sales volume.

Wall St was happy to back the Fed rate rise, thus the weaker AUD this morning. Falling energy prices may also help household cash flow in the US.

Argentina has sown around 6.1mha of wheat this year. Weather has improved across the Pampas and is potentially a little wet in places believe it or not. Cordoba is still a bit dry though, receiving just 50% or less of average July rainfall. Buenos Aires produces about 40% of Argie wheat, Cordoba 20%.