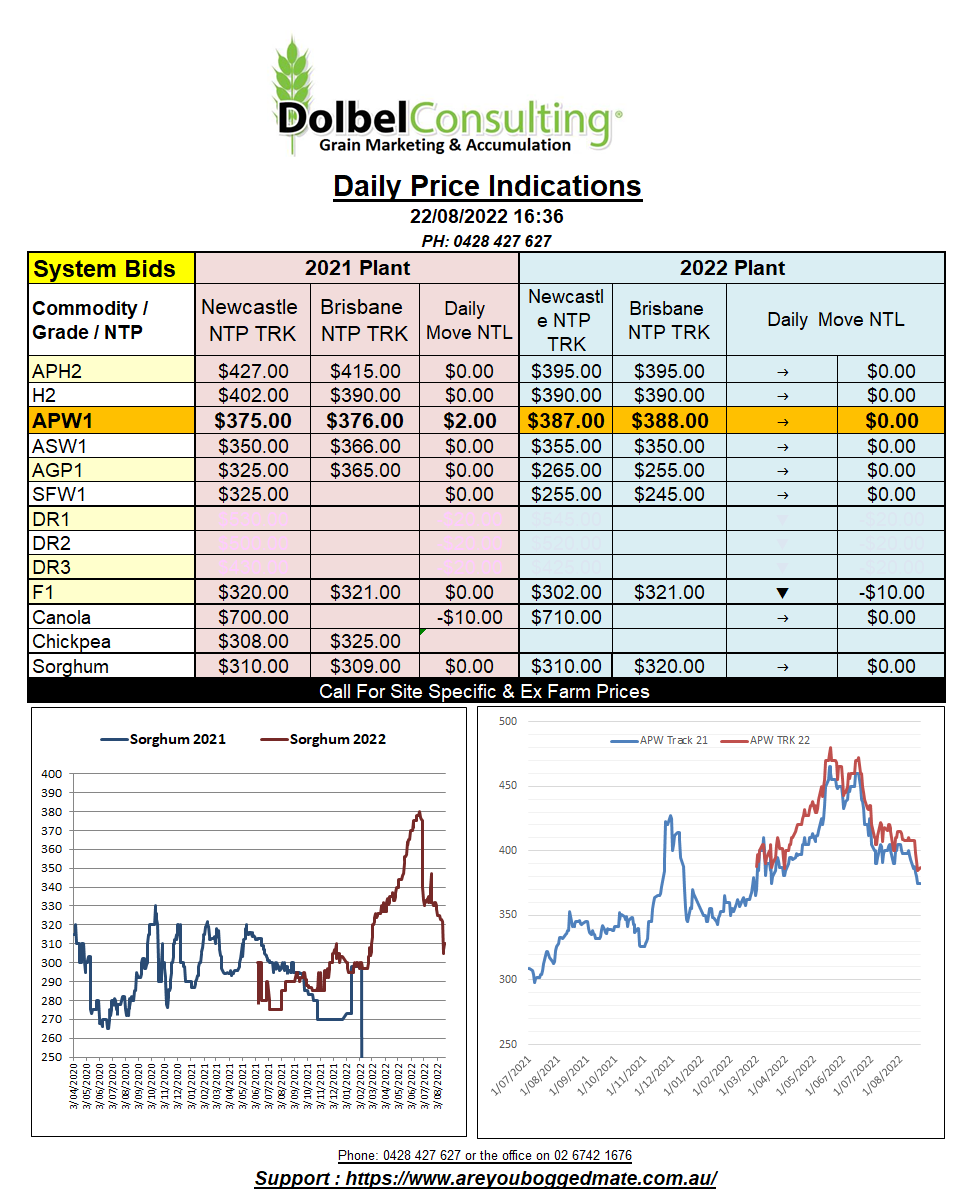

22/8/22 Prices

Russia reduced its wheat export tax for the following week by US$3.93 to US$80.75 per tonne FOB. Traders and farmers have been canvassing the government to further reduce the export tax on wheat. With a record crop likely this year the only thing supporting an export tax is grade. There were reports mid-week that up to 50% of current deliveries were only making feed wheat grade. Makes one wonder if the Russians wouldn’t be better off placing the export tax on milling wheat and removing it off feed wheat, makes sense, good luck policing it though.

Although US yields for HRWW and spring wheat are generally a little lower thanks to drought in the west this year, the quality is very good. With a continuation of the La Nina for another year this may bode well for US farmers if the Aussie crop is again downgraded at harvest. Wise farmers in the US are expected to carry a little more wheat forward this year after a sharp drop in prices during the harvest period disenchanted many.

At Chicago wheat finally bounced, closing AUD$11.63 higher overnight. Up until Thursday Chicago Dec 22 SRWW futures had closed 73.5c a bushel (AUD$39.30/t) lower than Fridays close. A sharp decline on the back of potentially higher exports out of the Black Sea. Dec22 SRWW futures at Chicago averaged 776c/bu during the first half of February this year, prior to the invasion of Ukraine. So, to be at this value given sharp increases to some major exporters production estimates it isn’t all that bad. Bargain hunters may become more active. Year on year wheat carry over from the major exporters is expected to be back 2.4mt. Major importers carry over wheat stocks are expected to increase by 2.61mt, to 180.47mt. So, we are not going to starve. Just keep an eye on 2022-23 winter wheat area in China and the USA. China announced a drought warning for the Yangtze yesterday.