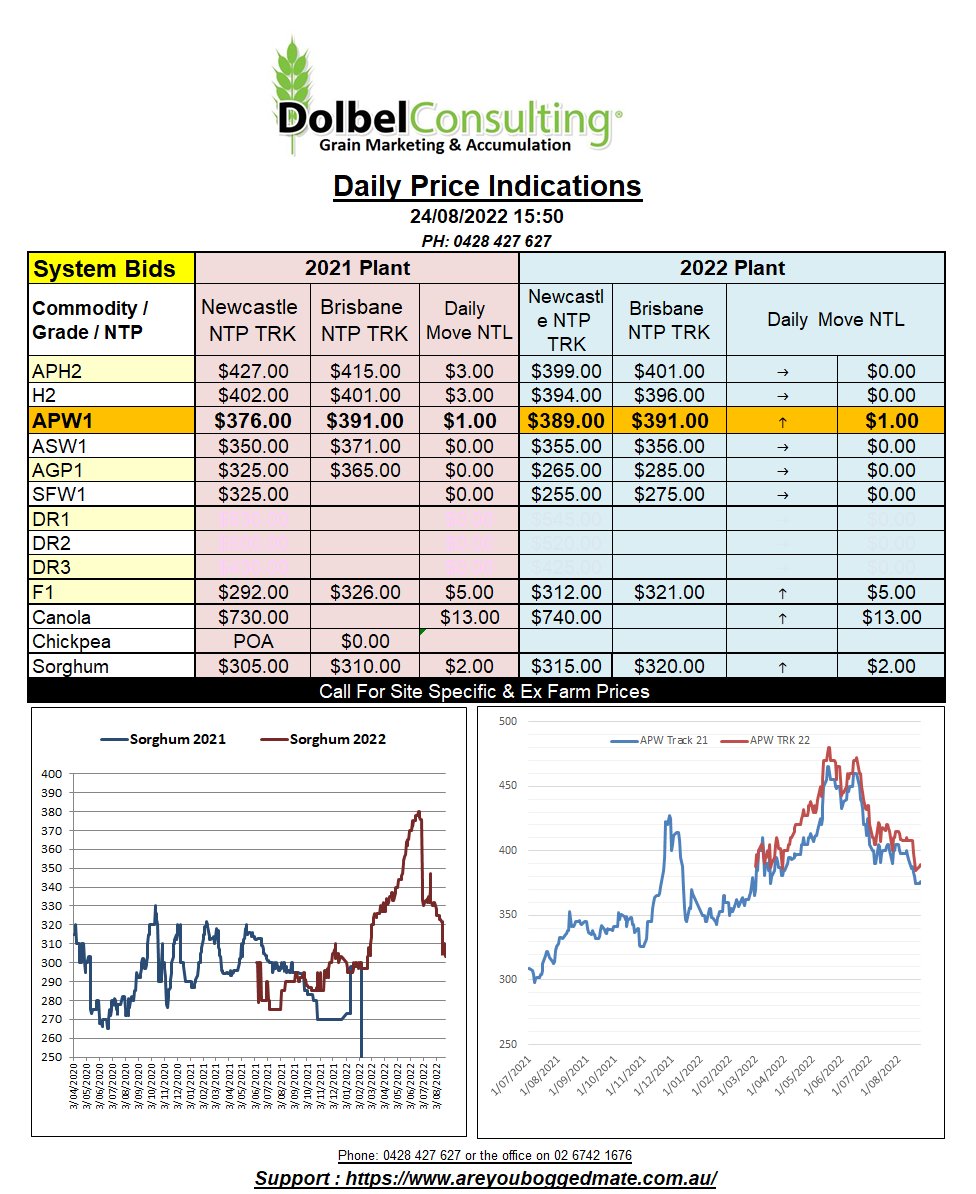

24/8/22 Prices

US wheat futures found spill over support from the corn and soybean pits which found their support from lower G/E ratings on Tuesdays weekly crop progress report. Fundamentally wheat has little reason to rally from a global perspective. Increased competition from the Black Sea and confirmation Germany will see a 3.8% increase over last year’s wheat crop, even with the dry weather, were just a couple of the stories working against wheat.

Russia confirmed the sale of 240kt of milling wheat to Egypt. This was not a public tender, so prices were not made public, but the trade assumed the value was around US$368C&F, around 8% below their last purchase price in July.

Russia will need to see more what sales on the book if they are to pick up the pace and meet USDA targets. Currently just 5.9mt has been exported in the current marketing year (starts July), around 27% less than this time last year.

Rainfall continues to delay some harvest and field work across eastern Ukraine and south-central Russia.

Feed barley prices into S.Arabia were generally firmer with French and Russian offers rallying between AUD$10 and AUD$15 per tonne. With dry weather dominating the Northern Hemisphere harvest, apart from parts of Russia and Ukraine, the quality of the wheat crop is generally very good. This is good news as global barley production is estimated at 146.3mt, +1.2mt on last year. Consumption of barley is estimated at 147.061mt resulting in a slight draw down on world stocks. Opening world barley stock for this year was estimated at 17.557mt, closing stocks are expected to be around 16.853mt. Australian production is estimated at 5mt, back 1.5mt from 20-21, farmers choosing to sow wheat or canola instead.