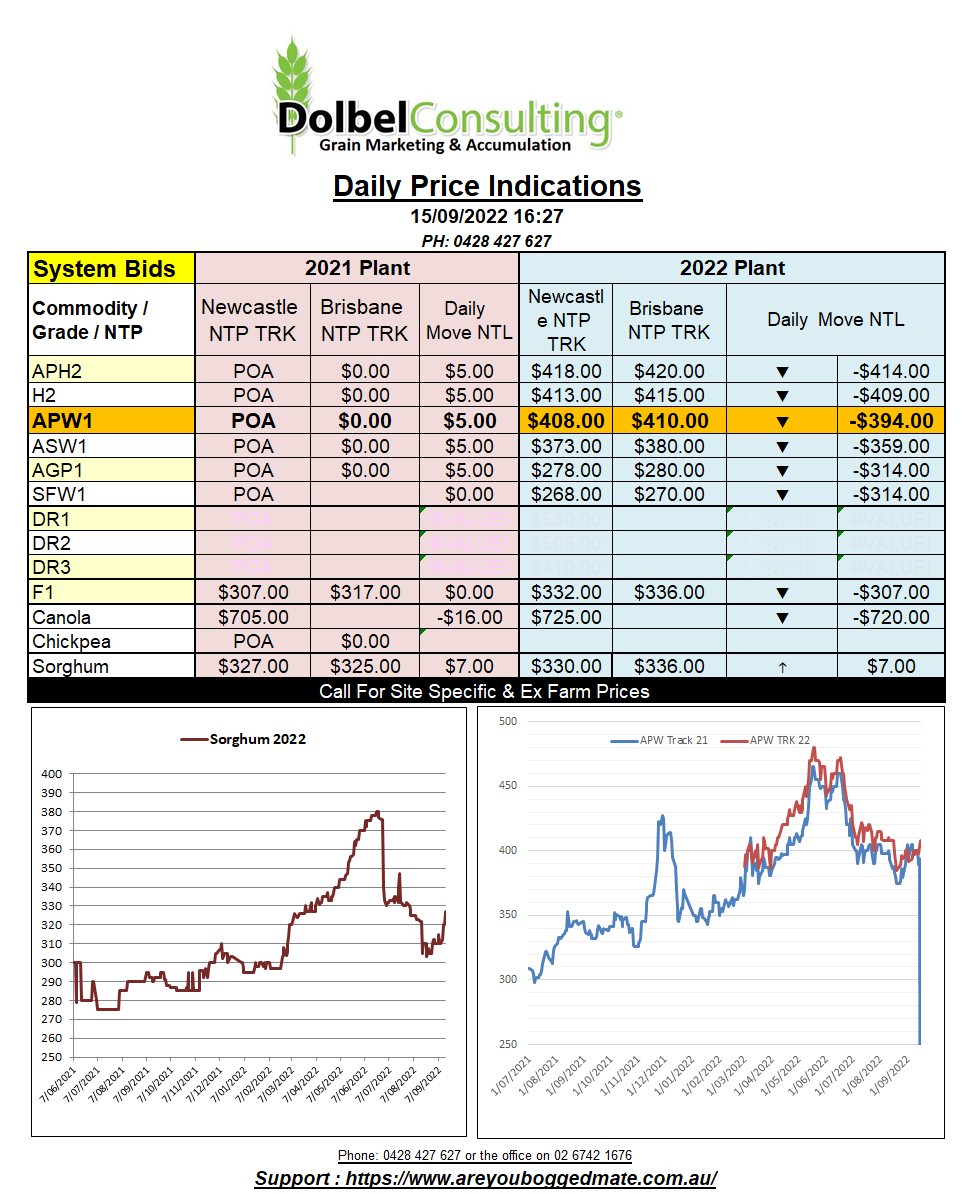

15/9/22 Prices

US corn and soybean futures closed in the red overnight. The later influencing a lower close in both ICE canola at Winnipeg and Paris rapeseed. In Aussie dollar terms the difference in day-to-day prices for canola futures represents a decline in Paris of about AUD$18.12 for the Paris Feb contract and AUD$4.17 at Winnipeg in the Jan 2023 slot.

Cash prices for canola across SE Saskatchewan were also lower. Grain for a December lift was bid on average ex farm at C$765.12, about a C$11.16 carry to the spot cash price. Durum bids in SE Sask were higher, as were spring wheat bids. December durum rallied about C$6.82 on average, bid at roughly C$400.07 ex farm compared to a spring wheat number of C$395.03. 1CWAD13 Durum now just C$5.04 over 1CWRS13.5 spring wheat. The spread between 1CWAD13 and 2CWAD11 remains relatively tight in SE Sask at -C$4.75.

Interesting to see ICE canola futures fall after the release of the StatsCanada number. Month on month Canadian production slipped 400kt to 19.1mt. All wheat production in Canada now stands at 34.7mt, a little above the trade estimate leading up to the release of the data.

Feed barley values out of Russia, Ukraine, France, and Argentina were all a little lower. Not by much but at a C&F level into somewhere like S.Arabia the move represents about AUD$2 to AUD$3. The conversion to an equivalent price in AUD XF LPP for French or Russian feed barley into S.Arabia still indicates that the trade has more than enough buffer factored into local cash bids across Australia to absorb more than a $3 move. With local barley production on the east coast of Australia being significantly lower again this year we should see domestic interest at least sustain the current spread to SFW1.