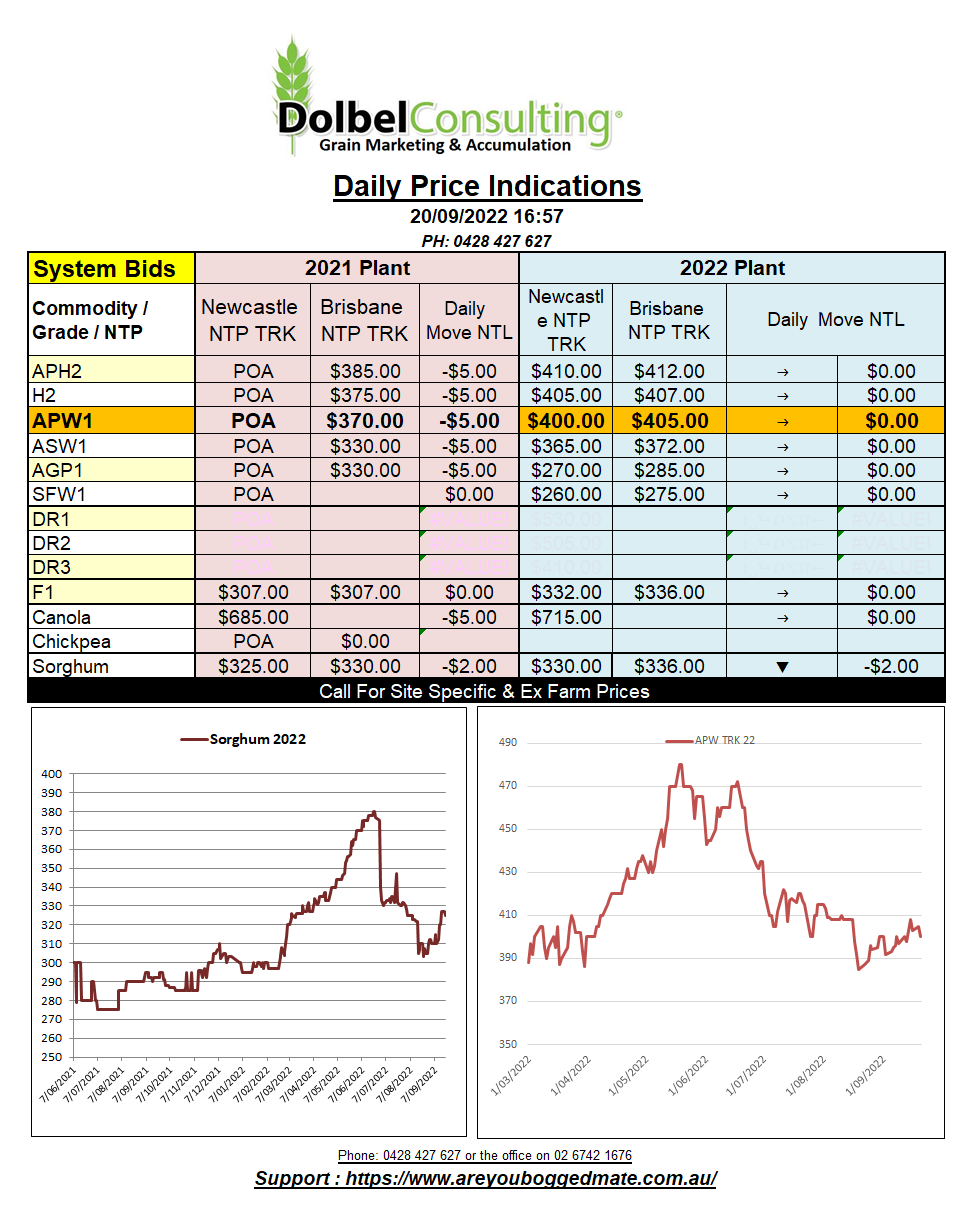

20/9/22 Prices

Weakness in US futures was initially fuelled by speculation that the Black Sea corridor is now not at risk. Putin must like having Black Sea wheat values on a string, one negative statement sending prices higher, only to fall just as quick on a positive statement. Russia has a very large wheat crop of various quality to sell this year, being able to manipulate the price would be very handy.

With the Black Sea sentiment becoming less of a concern, US wheat futures fell away, triggering technical selling on the way down. The algorithm traders now well in control of the direction of US grain futures. We’ve known it wasn’t really the physical market in control of intraday trade for years, so this shouldn’t come as too much of a shock to producers.

Saudi Arabia picked up 556kt of 12.5% milling wheat over the weekend. The delivery period is between Nov / Feb and the price averaged out at about US$371.61. On the back of an envelope this would equate to a H2 price off the LPP of something close to AUD$420 XF. With APW bid at $440 port, or roughly AUD$390 XF LPP. This may indicate a potential increase in current premium grade spreads is feasible here. Throw La Nina into the mix and I’m surprised we haven’t seen an increase in H2 / APH spreads on the east coast already.

Russian feed wheat is priced at about US$263.50 for a Jan / Feb slot FOB Black Sea. Using the back of the same envelope to see how this compares to Australian bids for new crop ASW we come up with a number closer to AUD$400 XF than $300 XF. This also indicates that current multi grade spreads to ASW / SFW1 are not reflecting current international values. Potentially large stocks of low grade ASW out of WA appears to be the issue.