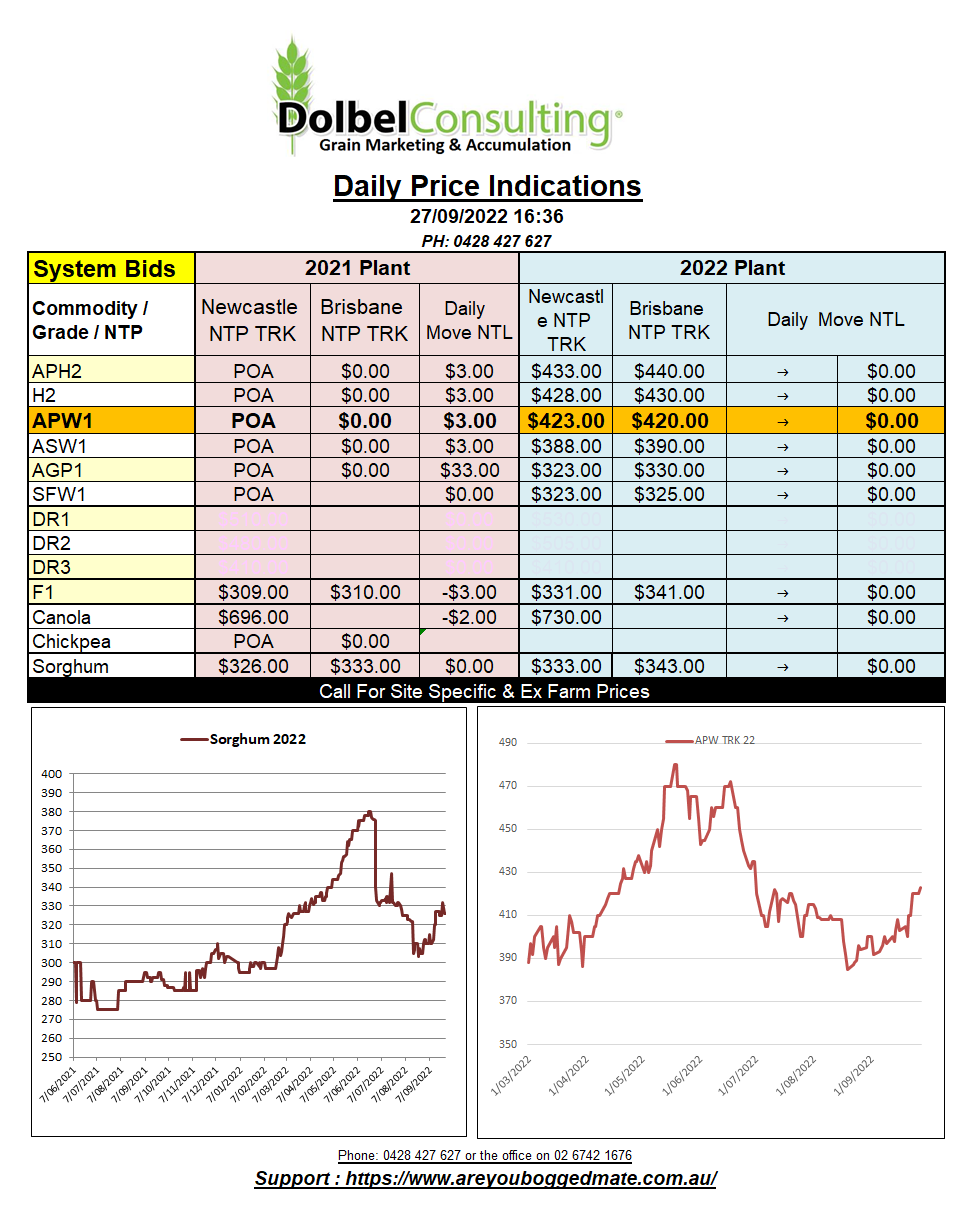

27/9/22 Prices

Spill over selling from the share market hurt US grain futures overnight. One might have expected to see the US market rally a little with the prediction of a Hurricane crossing the coast of Florida and pushing inland, but the markets chose to concentrate on the bigger picture. That is the continuing demise of the prospect of any short to mid-term global financial growth.

With most reserve banks appearing happy to use inflation to reduce debt, we may soon see what was initially supply driven inflation, crush demand for many non-essential items. Looking at the past for direction we quickly see that grains were often a casualty in large market corrections. This is resulting in some analyst forecasting lower returns into Q2-3 of 2023 for most grains given average production. Probably not what Russia wants to hear, a huge wheat crop, potentially 100mt, and slow exports, may see Russian wheat become more accessible to the world market as prices decline.

Southern hemisphere producers may find basis remains weak during Q4 2022 as marketers attempt to buy / sell into global and domestic markets that some analysts are predicting are more likely to slip sharply rather than improve from the highs we’ve seen over the last 9 months.

In December 2020 the prospect of 850c/bu wheat futures at Chicago seemed fanciful. World wheat production was estimated at 773.66mt and yet here we are today with a world wheat production estimate of 783.92mt and 858c/bu wheat at Chicago. Ending stocks have fallen from 316.5mt to 268.57mt during that time, helping this look more plausible, but at the same time major exporters stocks have actually increased by 1.84mt and that is with the USDA calling the Russian crop 91mt, some 9mt under most private estimates now considered accurate. If we see demand slip back to 2020 volume and the USDA start to reflect larger production estimates for Brazil, Australia, and Russia, we may well see ending stock begin to climb quickly.