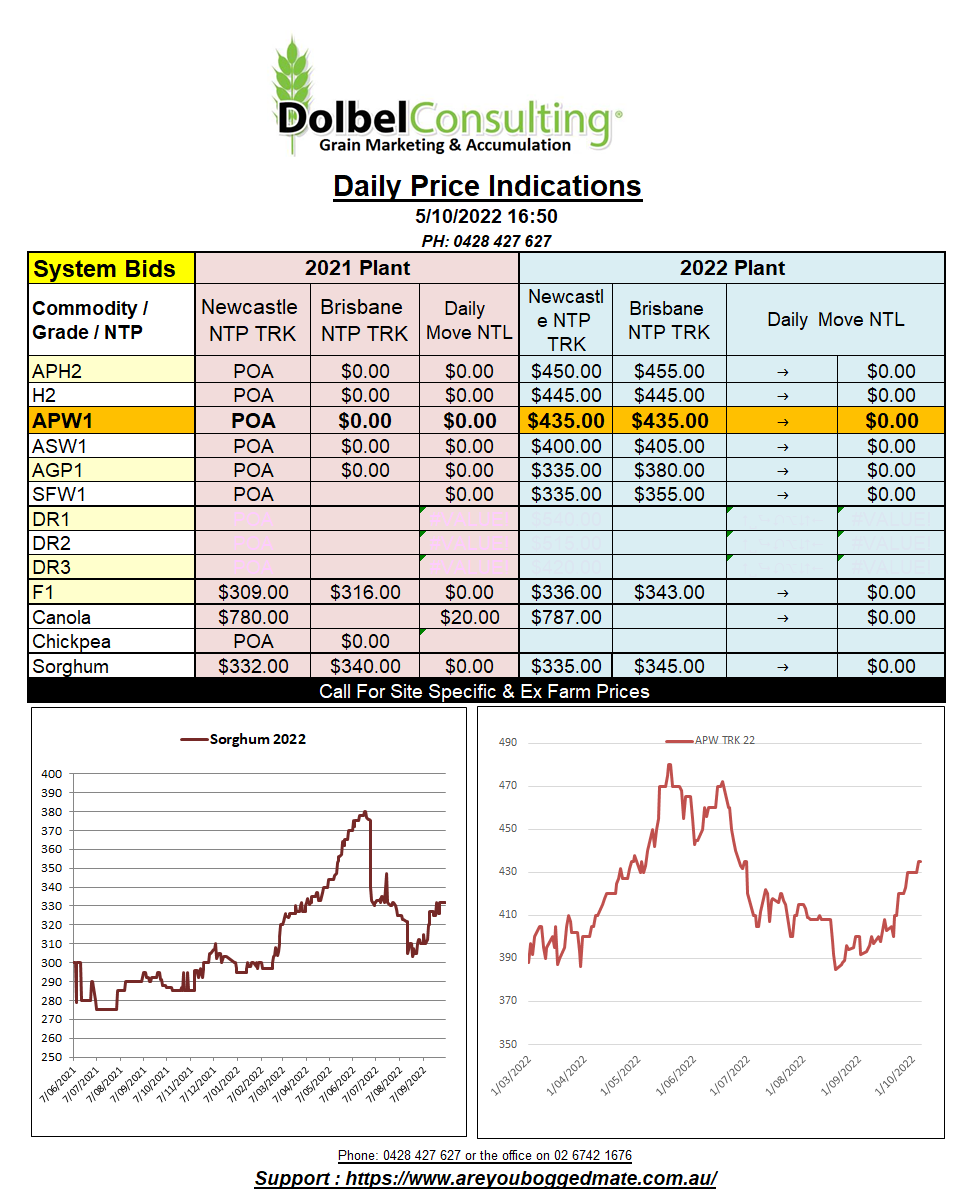

05/10/22 Prices

Algeria picked up 300kt of wheat on Friday, the majority being Russian. Approximately 180kt of the tender is Russian wheat from the Black Sea. Other supply destinations included Bulgaria, France and Ukraine with 30kt each. Algeria is also in the market for 50kt of durum wheat, this tender closing on the 6th. Tunisia is also expected to confirm a tender for durum wheat over the next couple of days.

In Aussie dollar terms both Canadian and French durum values were higher overnight. On the back of an envelope French and Canadian prices are converting to much higher ex farm LPP equivalent values than we are seeing currently bid. There is still a significant gap in converted value between the French and the Canadian product. The lesser of the two indicating that local values could be closer to AUD$560 ex farm.

If we can confirm the value of either of the above two durum tenders it will help a lot with price discovery in the short term. With new crop DR1 at just $540 NTP NTL less GTA French and Canadian values do tend to indicate there is more potential for upside than downside in new crop durum.

The delivered Newcastle market isn’t trying too hard to compete with the track this early in the season either.

There are reports that Russia has now harvested 102mt of wheat, if correct, this will be “their” biggest wheat crop by a country mile. It may also explain why inspections for Ukraine wheat exports through the “grain corridor” are so slow.

At Chicago “technical Tuesday” lived up to its name. In the end wheat futures were mostly flat to lower. Cash prices out of the PNW followed their futures grade equivalent market. White wheat out of the PNW was unchanged.

Paris milling wheat futures followed the lead from Chicago, slipping E1.25 nearby and E2.00 for the March slot. Argie weather is still a major issue.