12/10/22 Prices

The sharp surge in US wheat futures in the previous session triggered a little profit taking overnight, pushing futures lower. Technical positioning prior to the release of this week’s monthly USDA World Ag Supply and Demand Estimates was also evident.

Fundamental weakness for wheat was found from talk that Russia may be about to remove export quotas that had been put in place to ensure ample wheat stocks prior to the commencement of war with Ukraine. Russia has harvested a bumper wheat crop this year, domestic stocks are now plentiful there, resulting in some traders assuming that export volume will increase greatly in the short to mid-term.

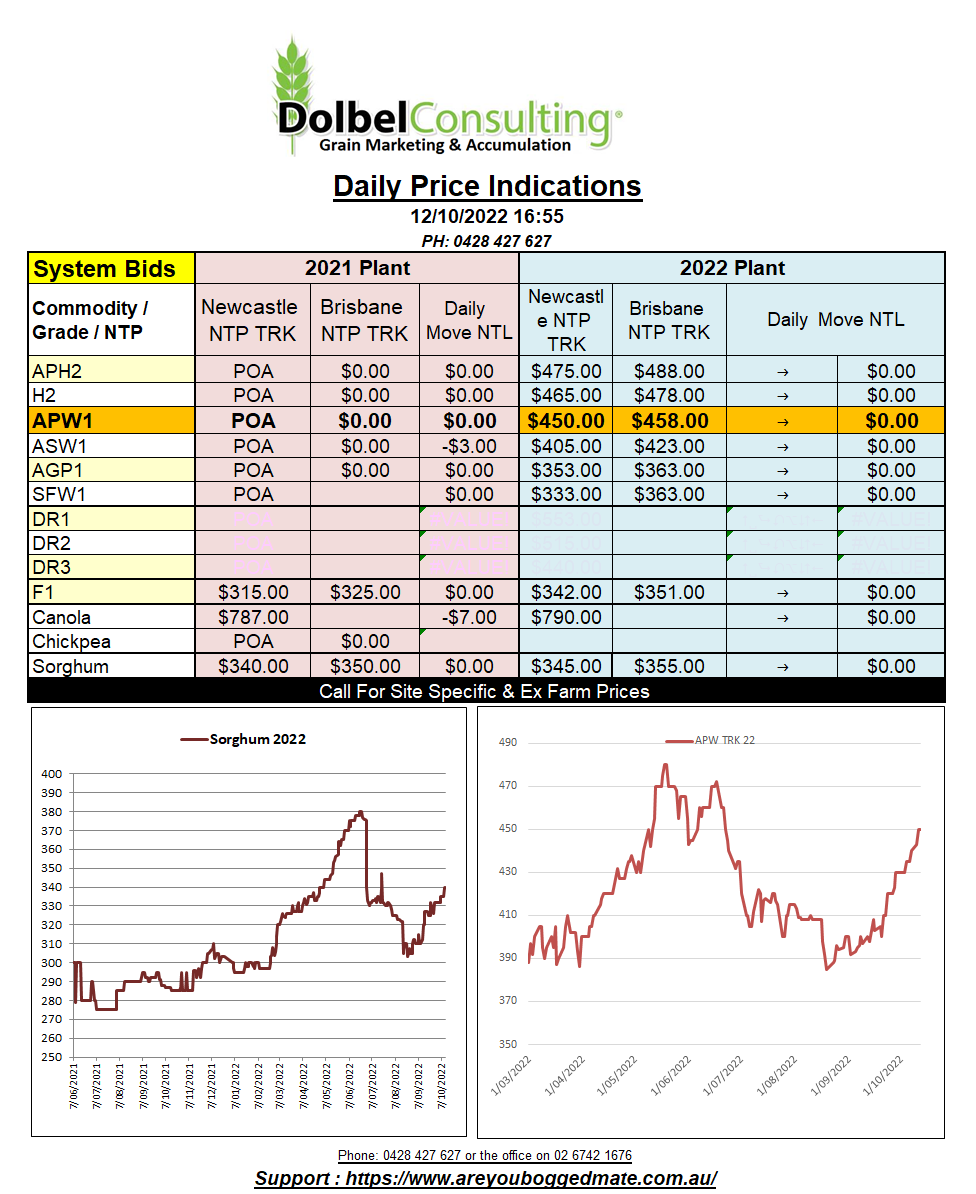

Comparing US, Australian and Russian wheat into the Asian market we see Aussie wheat is still very cheap. C&F China ASW1 wheat out of WA comes in around US$285, US soft wheat out of the PNW around US$410 and Russian wheat around US$350.

US wheat, and corn for that matter, remains the most expensive grain in the world. The strength in the US dollar is not helping them either.

Australian basis remains very low in an attempt to clear as much stock as possible prior to another big harvest in the west. Recent adjustments higher now have the WA crop closer to 12.2mt. The is against the trend lower for east Australian wheat, where wet weather continues to see flood water, disease and lodging becoming a major problem in low lying fields from the QLD border to Victoria.

Private production estimates for NSW, Australia’s second largest wheat producing state, are now back 26% on last year’s production.

Turkey picked up feed barley at tender, the lowest number was about US$325 CFR. Turkey is expected to pick up about 495kt this week.