17/11/22 Prices

The ending of daylight savings time in the US and Canada has seen the delay in the availability of some market data in the morning while I prepare the morning comments. If there are major adjustments to be made to price comparisons or some news influences physical price analysis after the release of the morning comments, I’ll make mention of it in the afternoon comments.

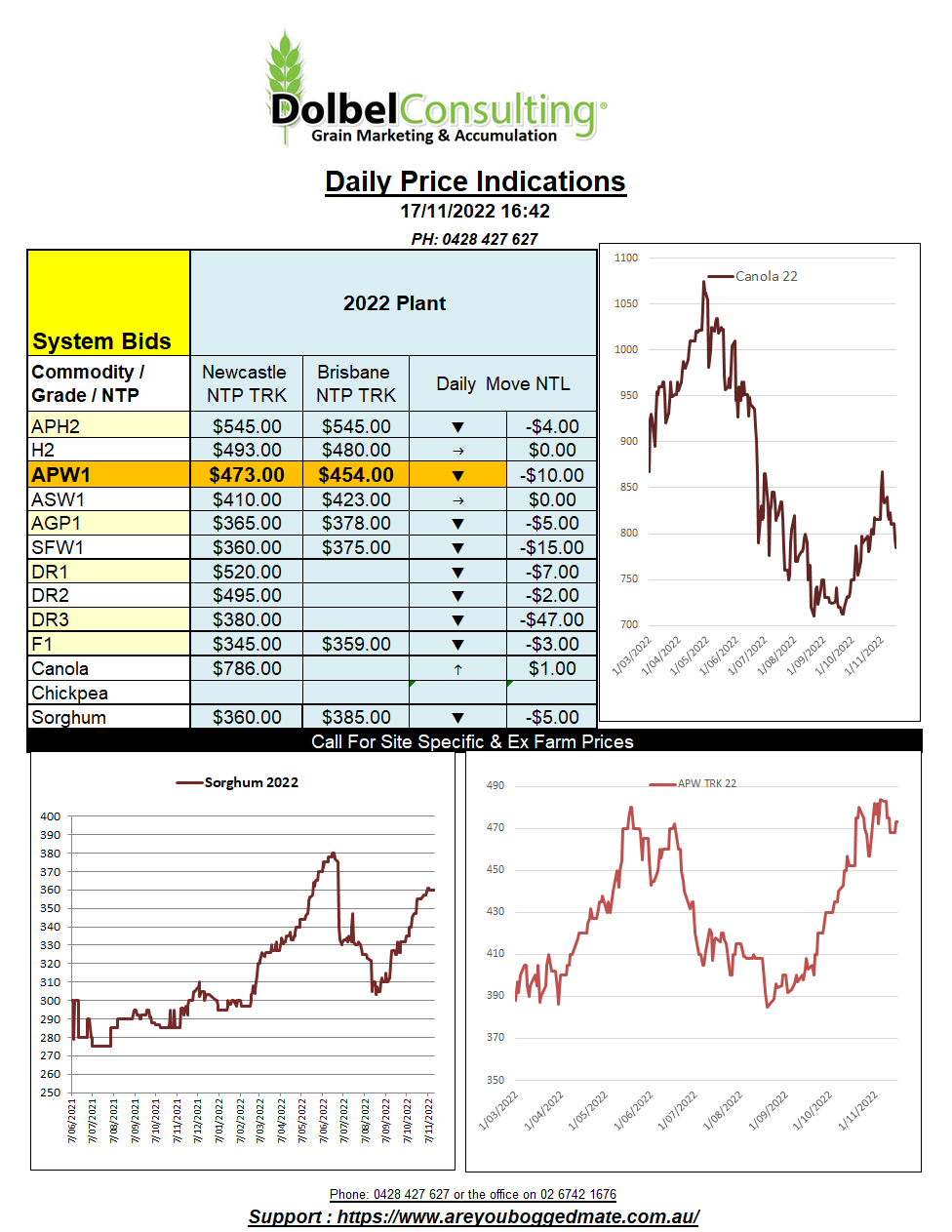

US soybean futures came under pressure overnight. Technical selling was triggered by rainfall in Brazil, and profit taking in soy oil. The weakness in the soybean pit did not spill over into the Paris rapeseed market, which actually managed to close higher on the nearby contract. Winnipeg canola did find some pressure though and shed C$12.20 on the nearby futures contract.

With the AUD a fraction lower and the local market generally more reflective of the EU rapeseed market of late it will be interesting to see if the trade here continues to track EU movement versus US soybeans and ICE canola. The Australian trade are persisting with the $10 discount for those unwilling to comply to ISCC audit procedure for Australian grown canola. Bureaucratic profiteering if I’ve ever seen it.

Basis to Paris rapeseed has blown out by almost another -$30 per tonne this week. An incredible amount given the damage we are seeing to canola on the eastern seaboard, I guess it shows how small the domestic market really is. Markets are often much slower to react to upward fundamental pressure than downward pressure though.

Paris wheat futures were higher in the December slot, closing at US$332.52 per tonne. Chicago was back a little closing at US$300.34, that’s a nice premium Paris has over Chicago. The shorts in Chicago wheat are holding tight. Some analysts are predicting a short, sharp correction in Chicago.