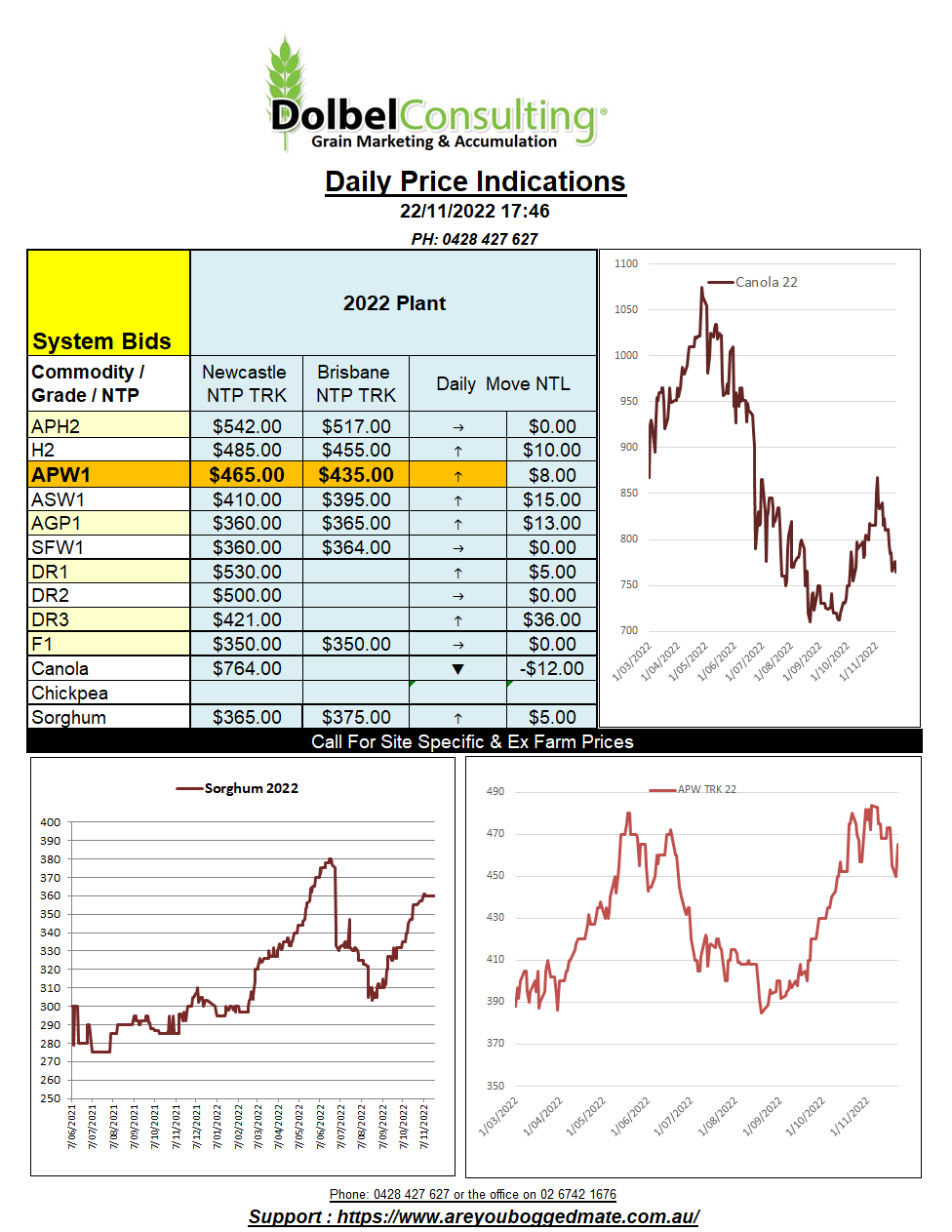

22/11/22 Prices

Not the way you like to see US futures start the week. Wheat and corn pushed a little lower. Corn, unlike wheat, had become vulnerable to a technical sell off after becoming massively overbought in recent weeks.

The selling in corn spilt over into the wheat market which was attempting to move higher on the back of both technical indicators and deteriorating world production estimates. Soft red winter wheat December futures at Chicago are oversold and should find some level of support from both this technical aspect of the market and the reductions in quantity and quality from Australia and Argentina.

Soybeans at Chicago found support closing slightly higher. Unfortunately, this support did not roll across to either Winnipeg canola futures or Paris rapeseed. Paris slipped roughly AUD$11.24 on the nearby contract.

The only thing working in our favour last night was the weaker AUD. The softer Aussie dollar should be able to turn a weaker close in US wheat futures into a positive start to wheat here today. The SRWW futures move was worth about -AUD$2.23 / tonne, the AUD drop worth roughly +AUD$4.94 per tonne. The fall in the AUD may not be able to counter the decline in canola or rapeseed futures though.

Increasing COVID cases in China and their persistence with their zero COVID policy continues to hurt Chinese demand sentiment.

The northern hemisphere is nearing the completion of winter wheat sowing. European weather has been average, France and S.Germany are generally seeing good conditions while NW Germany and Poland are becoming dry. Ukraine is average. Russia is dry in the south and wet in the central districts. India is dry. China has remained dry in the south but the winter wheat regions in the north are seeing average to above average rain in the far north.