24/11/22 Prices

US wheat, corn and soybean futures closed firmer across the board, as did the AUD. The Aussie dollar put on 1.34% against the greenback in overnight trade and is steady at 67.29, near the session high, as I write. That’s an increase of over 3c for this month.

Paris rapeseed futures were sold down hard, shedding almost AUD$30 on the nearby contract. Winnipeg was also lower, breaking away from any influence the soybean market had over it and falling AUD$6.67 on the nearby contract.

The move lower at Paris is important as the support level of E600 has been broken significantly, triggering further technical selling. All months now closing under the E600 mark. EU grains were generally lower across the board. Milling wheat also taking a hiding on the nearby contract shedding E6.25 per tonne after showing good resilience against weaker closes at Chicago all week and sustaining a significant spread to US values.

What are some bullish factors this week. Shrinking EU wheat stocks, Argentine drought still an issue in the north. Some parts of Brazil drying out as soybean sowing cranks up. Still very dry in Poland. Chinese covid closures are probably the most bearish issues, the Ukraine / Russian war isn’t getting a lot of attention after the missile hit the nuclear power plant earlier this week.

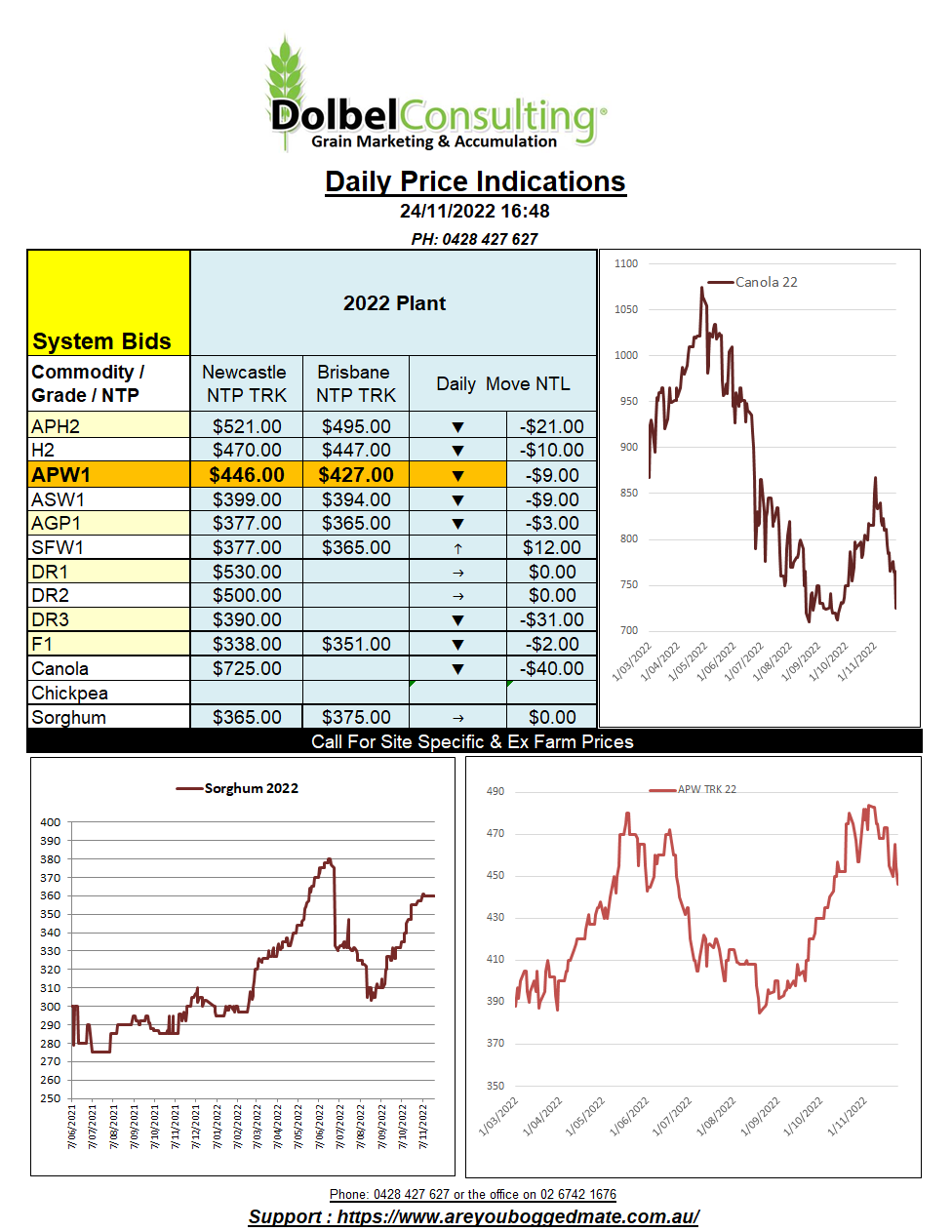

Thailand picked up Australian feed wheat at US$345. This roughly converts to a price of over AUD$400 ex farm which continues to support current ASW / AGP / SFW1 pricing levels in the short term.

Turkey are in for 455kt of wheat, tender results on the 29th.