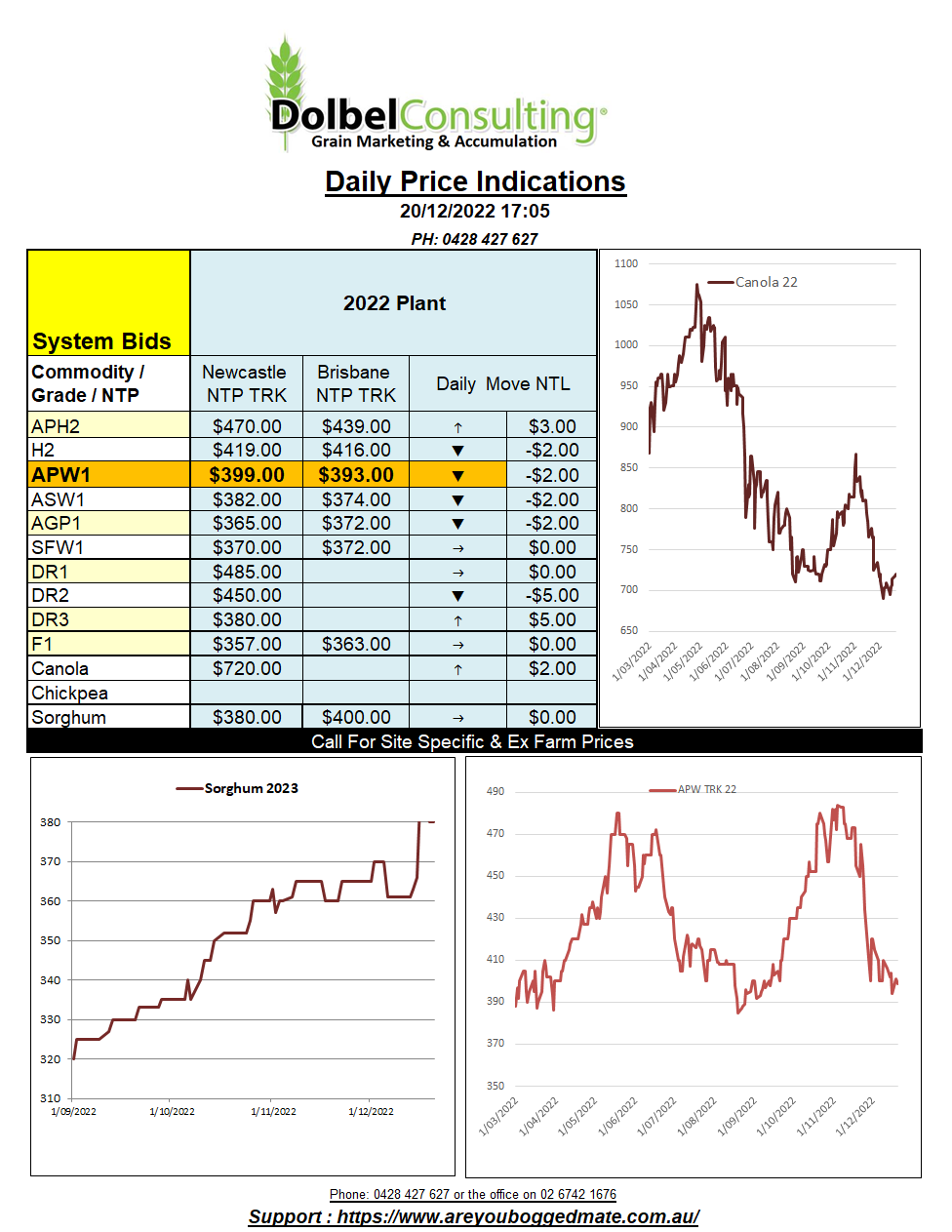

20/12/22 Prices

International grain markets continue to worry about the potential of a global recession and the impact a recession will have on demand. This is tending to force those on the fence to be more bearish than bullish. Fund and tech shorts continue to be the most favourable position at present.

From a fundamental perspective for wheat there is not a lot of reason to be bearish. If demand remains constant, the focus should return to world production and opening stocks as we move out of the Northern Hemisphere winter in March / April.

Lower production in Argentina, the poor start to the US HRWW crop, dry weather in India, why is Russia increasing export taxes on wheat when they have so much to sell, good export pace out of the EU and the grade profile of a big Australian crop will all play a major roll.

The grade profile of the Australian crop will be interesting and may counter the poor US HRWW to some degree. Lower HRWW exports out of the PNW should help H2 trade at better values into the Asian markets. Something to consider when determining what to store into 2023.

US wheat futures followed the path of least resistance, lower. The HRWW contract at Chicago holding on well after a poor performance in the last session. HRWW and Spring Wheat values out of the PNW were a touch lower. With the AUD generally flat to a smidge firmer, the move in the US may put a little pressure on local wheat prices. It should be noted that basis to Chicago March23 SRWW is again at a negative, -22c/bu FOB, so the trade should have the ability to absorb a buck or two move in US futures locally.

Paris rapeseed was lower, shedding E3.25 on the Feb 23 slot, this is roughly converted to AUD$5.15, with Winnipeg also lower local bids may slip.