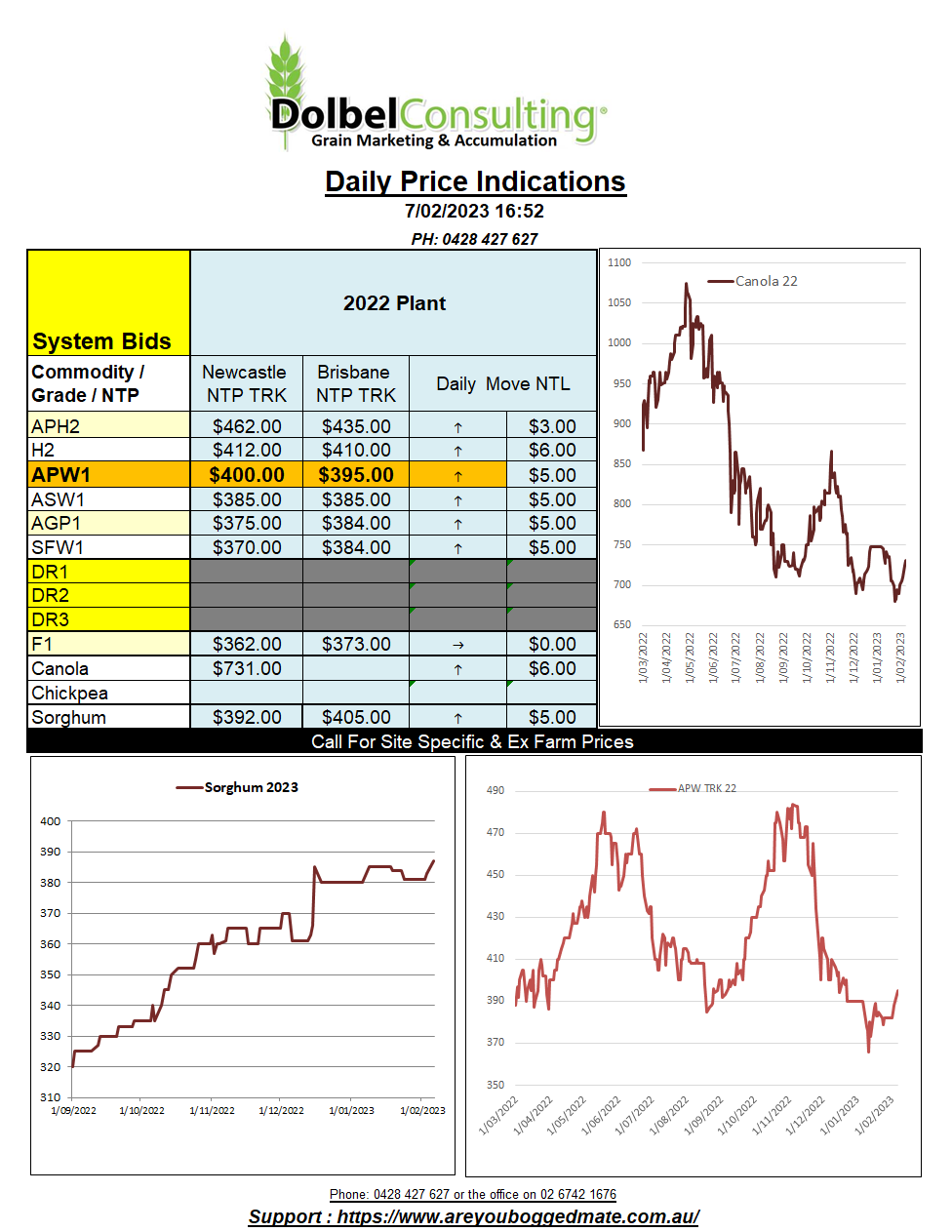

7/2/23 Prices

The USDA WASDE, World Ag Supply & Demand Estimate report, is out on the 8th of Feb US time. So, we should see the details on Thursday morning here. The punters are backing an increase in Australian wheat production, something which has generally been factored into the equation since ABARES came out with some record numbers a month ago. Other changes may come in the form of lower Argentine wheat production, possibly smaller opening / ending stocks for China and India. In the scheme of thing the AUD is likely to have a bigger impact on the local market than the USDA report does in February, but you can never be 100% sure.

US soybean futures closed lower, unable to recover from an early sell off bought about by tension over the shooting down of a Chinese “weather” balloon over US soil. There are rising concerns that China may cancel existing orders for US soybeans. This in no way has anything to do with a record Brazilian soybean crop that could be cheaper than where existing US purchase contract were struck. The weakness in Chicago soybean futures did not spill over into the Paris rapeseed contract or the Winnipeg canola contract. Both futures markets managing to close in the green. The rally in Paris rapeseed works out to a plausible upside here of roughly AUD$6.00 to AUD$7.00 today when taking the slight increase in the value of the AUD against the Euro into consideration. Generally, the AUD was weaker against most of our trading partners other than the Yen and the Euro.

Wheat futures found support from good US export sales & some more tenders from Algeria. The increase in the value of the USD did put some pressure on US export values. HRW out of the PNW, in Aussie dollars terms at least, improved about AUD$5.00 per tonne, so no real weakness into Asia today.