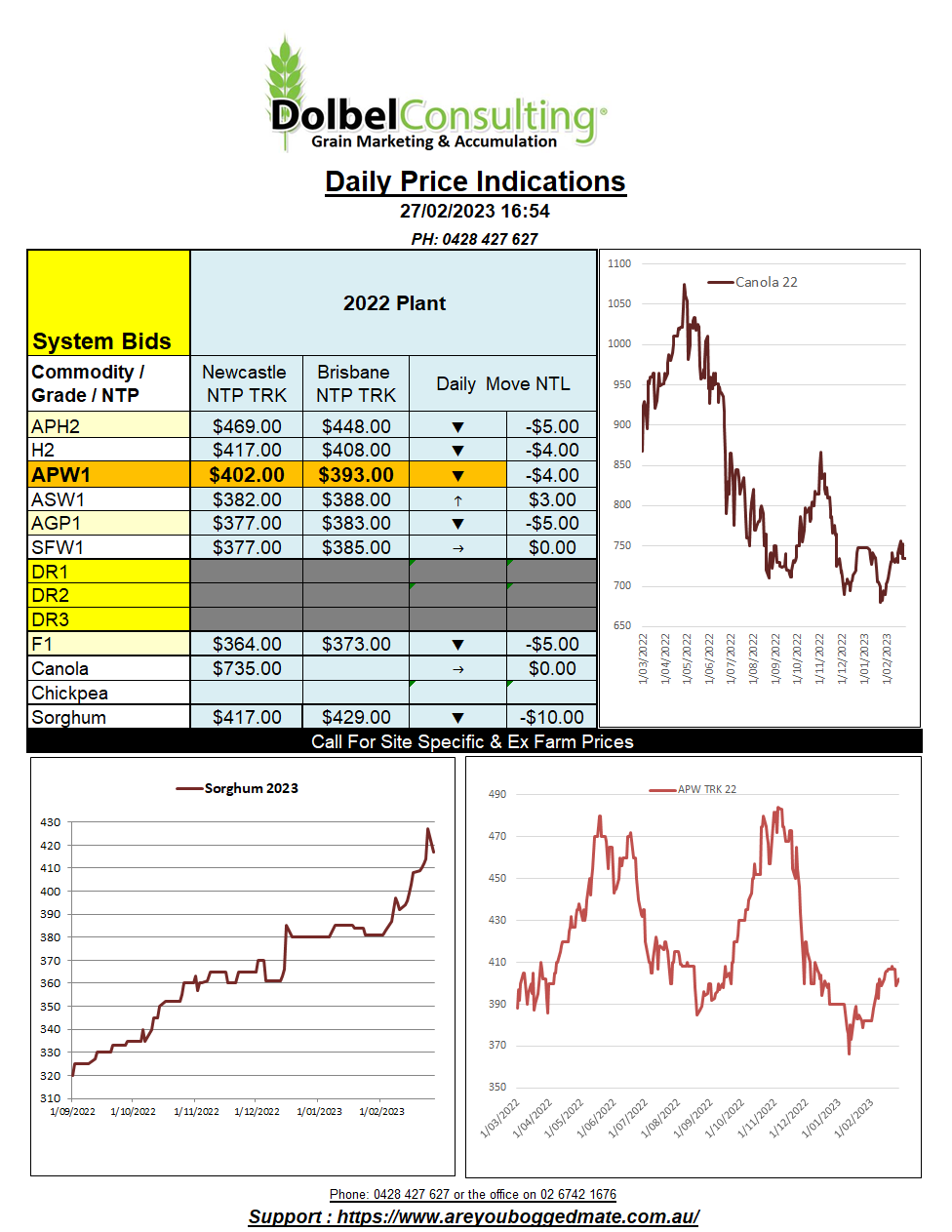

27/2/23 Prices

Egypt picked up 240kt of Russian wheat this week for shipment during the first half of April. The price was said to have been US$317.50 C&F. On the back of an envelope this is equivalent to somewhere around AUD$350 XF LPP, Australian milling wheat was never in the mix for this tender. Australia did however pick up 250kt of milling wheat into Iraq, Viterra supplying the lion’s share of the sale.

Turkey was also in the market, tendering for the supply of 790kt of milling wheat. This too is likely to be either Russian or Ukraine origin.

The EU Commission reduced their wheat production estimate 400kt to 126mt. Lower than desired soil moisture the reason. The EU winter wheat crop condition rating was unchanged at 95% good / excellent. According to World Ag Weather, over the last 30 days France has seen less than 25mm of rain. Much of the northern wheat districts have seen less, some none. This puts most of France into the 20% – 40% of normal rainfall over the last month scenario, not ideal. The dry weather extends east into Italy and as far east as Turkey.

Russia, Ukraine, and Kazakhstan appear to be having an average season now. Much of the Russian winter wheat regions are showing 14-day precipitation increasing to 20mm – 30mm. In the USA rainfall has been mostly east of the Mississippi, leaving large swathes of the HRW belt persisting with cold, dry conditions.

The stronger USD had a major impact on US futures overnight. Wheat futures at Chicago and MGEX saw losses. Fundamentally the outlook remains more positive than the move in futures might indicate. Not overly bullish but worth watching. US weekly wheat sales were up on last week, but don’t stand in front of a fund manager with a fist full of sell orders. Technically one might expect to see support for May HRW creep into this market next week.