21/3/23 Prices

The Grain Corridor deal is doing a good job of keeping everyone a little confused if nothing else. Russia is saying that because they objected to the extension for 120 days and suggested that the deal be extended for just 60 days that the deal is indeed up for renewal in 60 days.

The other parties were saying that there were no formal objections to a 120-day extension thus the deal was extended for 120 days. Meanwhile Reuters were reporting that the deal had been extended for 60 to 120 days.

Overnight it appears to have been confirmed by all parties that the deal was indeed only extended by 60 days. The end of May is shaping up to be a very interesting period for the world with several events now focusing on this time.

Is this a time paradox, great Scott Marty, or just a very ugly time for grain and financial markets in the making. Either way I’d like a DeLorean with a flux capacitor for a few days.

The risk on sentiment is spilling over from financial markets and into retail and grains. Believe me it’s spilling over into retail, I’m not a fan of cross entity marketing but if anyone wants a new sofa or mattress, I’m all ears.

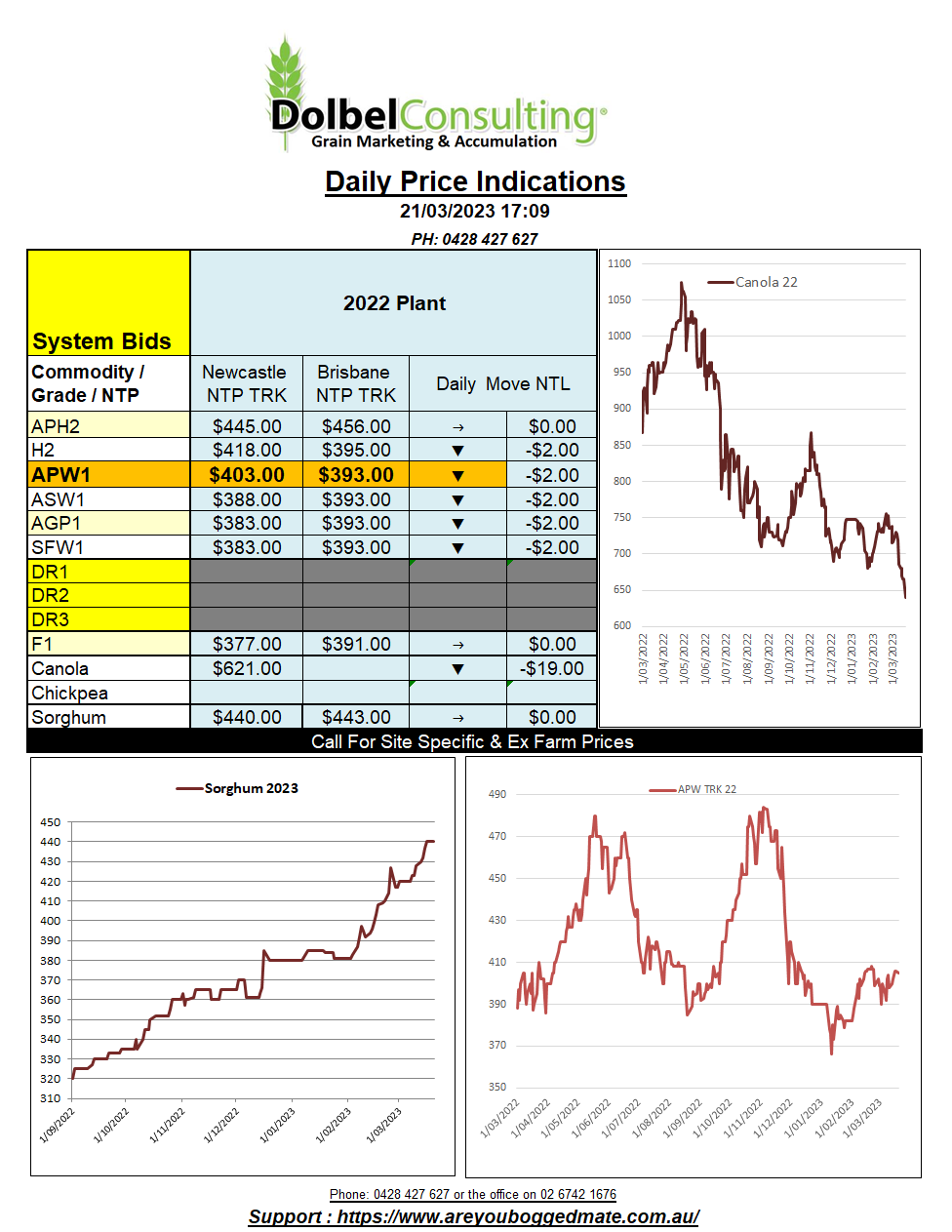

Looking at global grain values this morning. Cash values around the world are all lower bar 1CWAD13 out of SE Sask. Oilseeds are being hit hard. Although nearby Chicago soybeans did see some upside, outer months were softer. Paris rapeseed futures were hit hard, shedding E13.50 on the nearby. Taking the AUD / Euro into account this could see as much as AUD$19.53 off local prices today if local basis sustained.

Much of France and Germany have seen fortnightly rainfall of around 25 – 50mm, alleviating short term moisture stress for now.