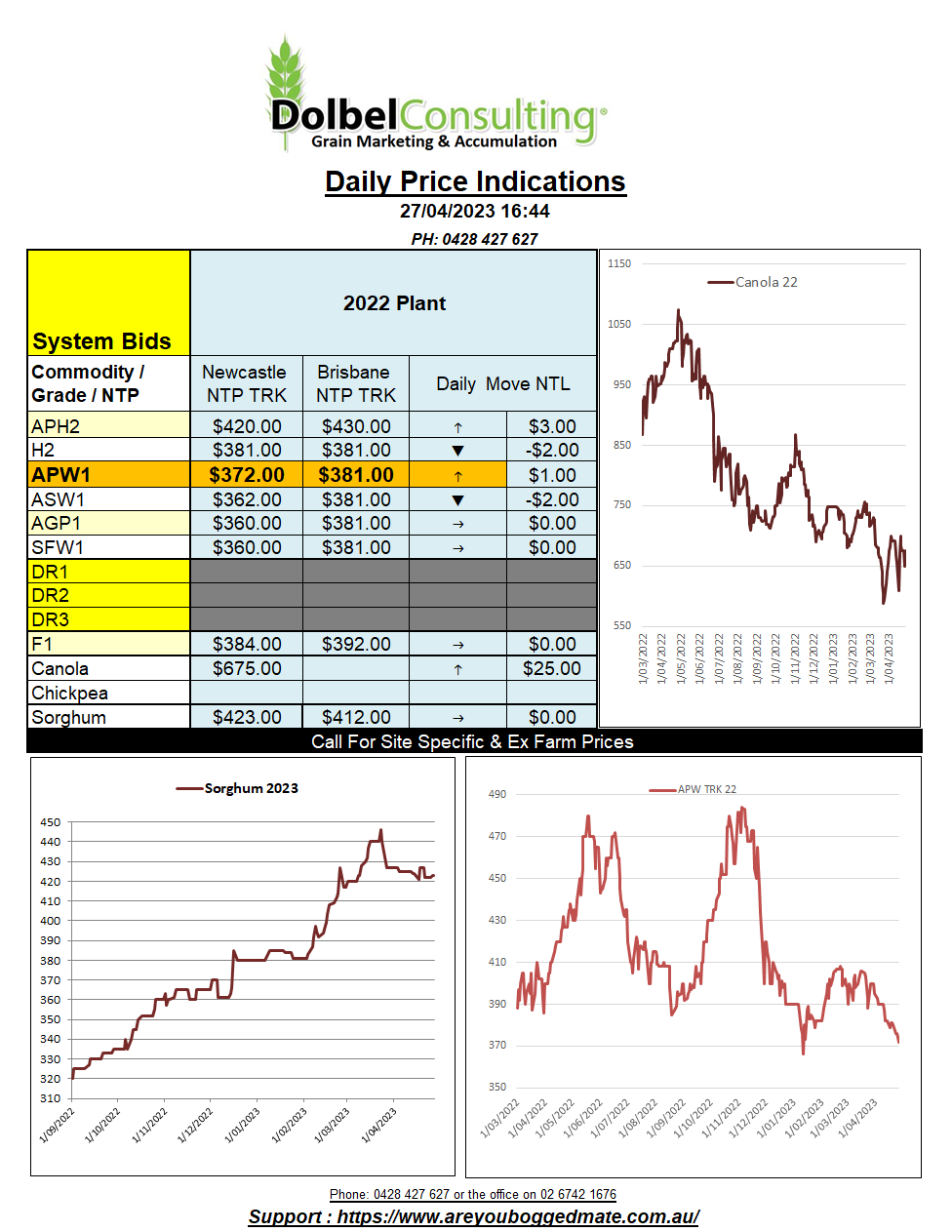

27/4/23 Prices

Local APW wheat basis to US wheat futures, (the difference between our cash price and the underlying futures contract for wheat at Chicago), continued to improve yesterday. Locally basis to the ASX was poor as local futures and local cash price slide lower in unison.

The increase in basis to US wheat futures appears to be the reaction of the US futures market falling away quickly as weather conditions improve across the hard red winter wheat belt. The punters “happy” to assume that the rain may put the brakes on a very, very poor hard red winter wheat crop deteriorating further. Local prices here generally benchmark off international cash values, taking less notice of US futures these days, leaving the HRWW punters in the US to play a US centric game.

To date there’s been little impact to US wheat futures in regards to delays in spring wheat planting there. Producers in Minnesota would have usually finished sowing wheat by the time they are expected to actually start sowing this year. The delay is not even rating a mention in anything other than farmer groups as yet.

The StatsCanada data was out on the 26th. All wheat acres were estimated at 26,967,900, a year-on-year increase of 1.58mac, +6.22%. The big increase in is spring wheat area, up 7.5% on last year to 19.39mac. Durum area is also expected to be higher, increasing by just 56kac to 6.062mac. The spread between new crop spring wheat and durum wheat price out of SE Saskatchewan continues to improve, 1CWAD13 durum now +C$33.04 to 1CWRS13.5 spring wheat for a September lift.

The area under canola is also expected to increase by just 201kac, up to 21.597mac. That’s not a small crop and will cap canola prices if realised. It’s not the largest area we’ve seen under canola in Canada in the last 5 years but given a good season it could become burdensome. Chickpea area +11.29%.