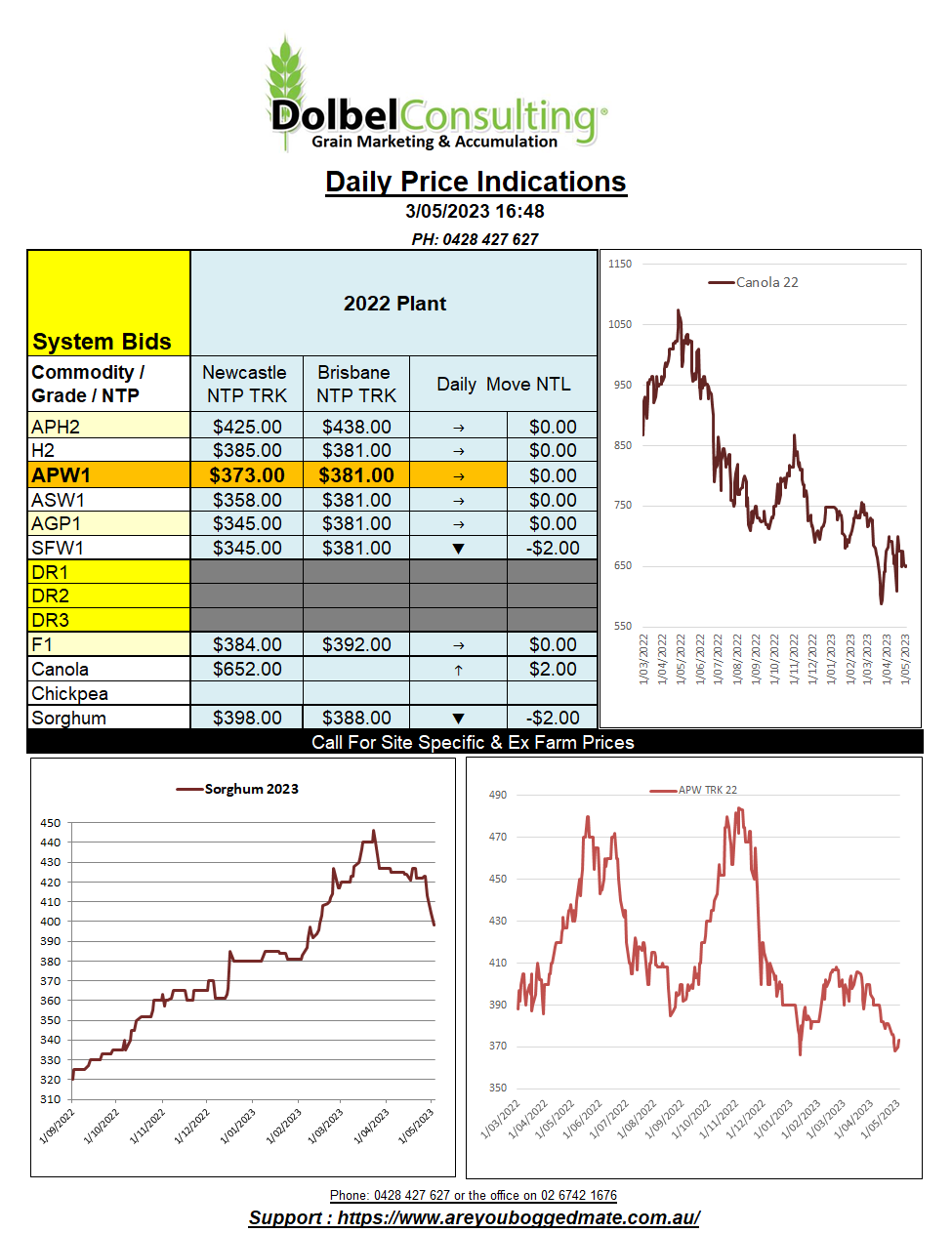

3/5/23 Prices

Yesterday’s Egyptian wheat tender was interesting. It helped to discover price, but it also helped to discover what was not acceptable.

Russian wheat was said to have been the cheapest at US$260 FOB.

Ukraine wheat was offered at US$255.50 but had the proviso against the offer that it was only valid while the Black Sea Grain Corridor deal was operational. This term was deemed unacceptable, and the offer was disqualified.

Offer values ranged from a low of US$260, which there were many, to as high as US$280 FOB. The final volume booked, and values is yet to be made public.

The limited access to banking platforms, sanctions and distractions with Ukraine seem to be having little to no impact on Russian grain exports. Last week shipping 691kt of wheat for export, resulting in a year-on-year increase in exports of “Russian” wheat of 37%. Considering Russia had roughly a 30% increase in wheat production last year the increase in exports is a welcome sign, signalling that 2024 opening stocks may not be too burdensome.

The devastating drought in Spain is starting to get more airplay as the punters join the dots. More so the case in barley than wheat, although some hard wheat may benefit from increased imports. The southern half of Spain remains very dry, the north not a lot better but did see some light rain over the last fortnight. A week ago, there was talk of crops dyeing in the field, this can only be getting worse now temperatures are into the 30’sC.

Rainfall across France and Germany has been a little light over the last week, but crop ratings in Europe remain generally good apart from Spain.

Central Russia is having a cracking season, good rain will also help Ukraine yields, although sown area to wheat there has been greatly reduced.