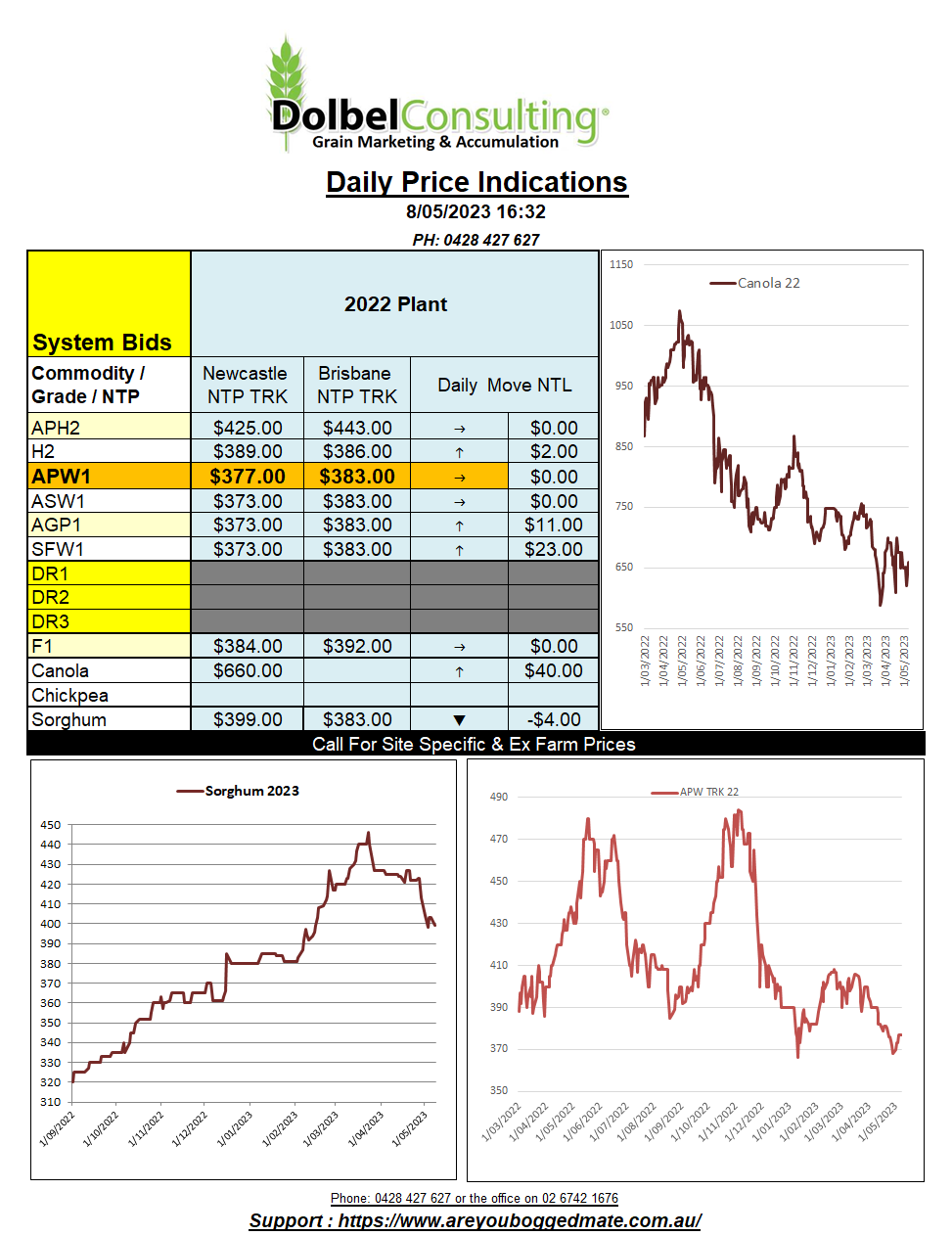

8/5/23 Prices

US wheat futures pushed sharply higher again overnight. Hard red wheat and spring wheat led the way, dragging both soft red winter wheat and to a degree corn futures at Chicago higher. HRWW was the leader, production issues in Kansas and delays in the spring wheat crop the catalyst for the rally.

The continuing problems between Russia and Ukraine also fed the rally. The chance of a Black Sea access deal going ahead for Ukraine exports looks poor. Russia continues to say they will walk away from an extension of the current deal if their concessions are not met prior to the expiry of the existing deal on May 18th. The threats are being taken seriously by shipping companies and insurance agencies, which are now rejecting work from that area until the deal is confirmed. Some grain buyers are also deciding against acquisitions from Ukraine via the Black Sea as supply cannot be guaranteed. Insurance companies have a 7 day renew threshold, which at 1% could become costly if delays are experienced.

Turnaround time for a boat picking up Ukraine grain is roughly nine days. That’s a lot of exposure in a region where things can change in the blink of an eye. Boat orders have fell 27% from March (489) to April (355) and are expected to fall even further in May, which currently stands at just 94 orders. The chance of getting stuck at a Ukraine port is very real, just ask one of the 50 or so boats already stuck there.

Tunisia picked up 100kt of durum and 75kt of barley this week. The lowest price on the durum was said to be US$385.49 / tonne C&F. The barley was said to have been purchased at US$254 C&F. These are best trade estimates at present.

French soft wheat condition slipped 1% week on week; 93% G/E is still better than last year’s 89%. France and Germany could see 20-50mm next week